Key Takeaways:

- Moody’s Corporation provides credit ratings through Moody’s Investors Service and analytical software through Moody’s Analytics, and its Q1 FY2026 adjusted EPS rose 13% year-over-year to $4.33 while revenue climbed 8% to $2.1 billion.

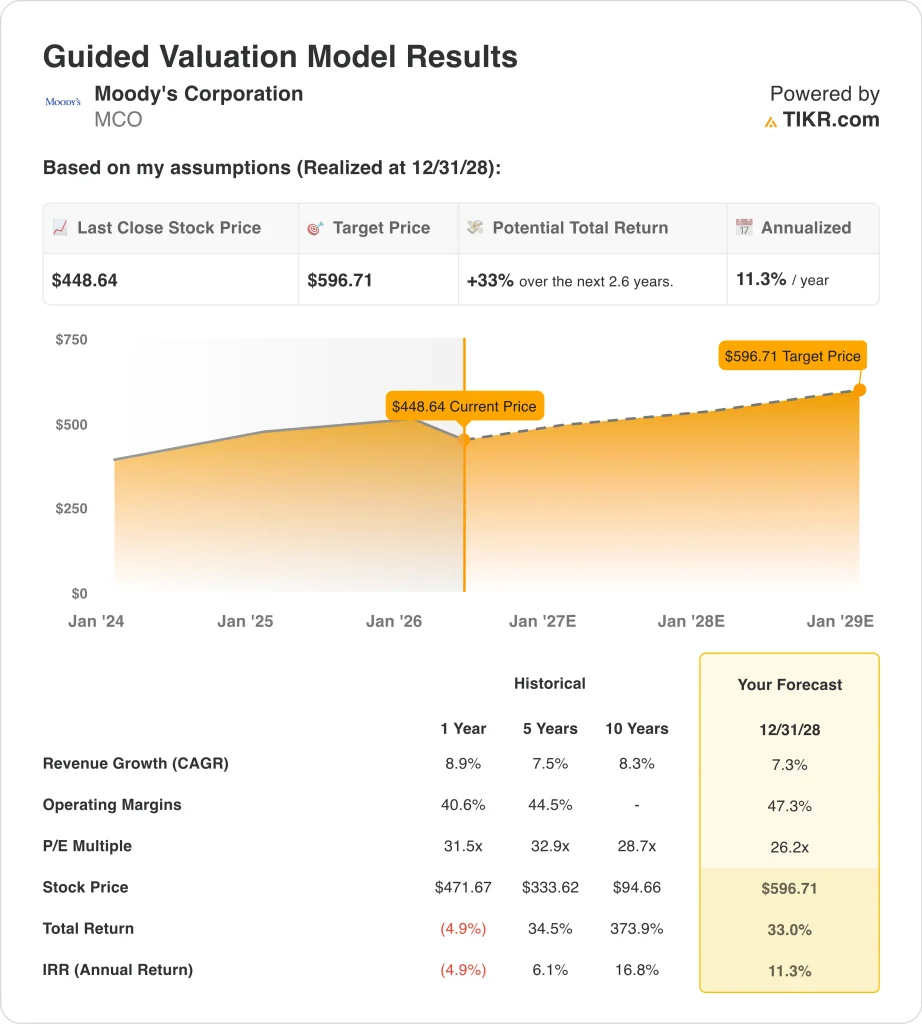

- MCO stock could reasonably reach $597 per share by late 2028, based on our valuation assumptions.

- This implies a total return of 33% from today’s price of $449, with an annualized return of 11.3% over the next 2.6 years.

What Happened?

Moody’s Corporation (MCO) delivered a strong start to fiscal 2026. The company’s Q1 adjusted EPS rose 13% year-over-year to $4.33, and revenue climbed 8% to $2.1 billion, according to Reuters. Moody’s also reaffirmed its full-year revenue guidance after the quarter. So investors got a clear signal that the business remains on track.

Strategic developments are just as important as the earnings beat. Moody’s expanded its Microsoft partnership in April 2026, embedding its credit intelligence directly into Microsoft 365 Copilot. Copilot is Microsoft’s AI-powered productivity assistant used by millions of enterprise workers. And Moody’s separately partnered with Anthropic to bring agentic risk workflows into the Claude AI platform, according to Reuters.

Moody’s also named Christina Kosmowski as the new CEO of Moody’s Analytics, its software and data division. It established a new regional headquarters in Riyadh, Saudi Arabia. So the company is building both its AI capabilities and its global commercial footprint. MCO also declared a $1.03 quarterly cash dividend, extending its consistent capital return track record.

The company’s LTM EBIT margin stands at 44.9%, and its LTM gross margin is 74.4%. But MCO has pulled back around 18% from its 52-week high of $547 to trade near $449. And the Street target price of $535 implies significant upside from current levels.

Here’s why Moody’s stock could deliver attractive double-digit returns through 2028 as AI integration strengthens both its ratings and analytics businesses.

What the Model Says for MCO Stock

We analyzed the upside potential for Moody’s stock based on its strong analytics growth, expanding AI-powered risk intelligence offerings, and recurring subscription revenue from the Moody’s Analytics segment.

Based on estimates of 7.3% annual revenue growth, 47.3% operating margins, and a normalized P/E multiple of 26.2x, the model projects Moody’s stock could rise from $449 to $597 per share.

That would be a 33% total return, or an 11.3% annualized return over the next 2.6 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for MCO stock:

1. Revenue Growth: 7.3%

Moody’s Q1 FY2026 revenue grew 8% year-over-year, driven by strong analytics results. The company’s forward two-year revenue CAGR is projected at around 7.1%. And its three-year historical revenue CAGR of 12.2% reflects structural tailwinds from global credit market activity.

Moody’s Analytics benefits from expanding subscription revenue, and Moody’s Investors Service (MIS) is tied to global debt issuance volumes. Both segments are positioning well for AI-powered data integration with enterprise platforms like Microsoft 365 Copilot.

Based on analysts’ consensus estimates, we used a 7.3% revenue growth forecast for MCO. This reflects sustained analytics subscription momentum, continued debt market activity, and emerging revenue from AI risk intelligence tools embedded in enterprise workflows.

2. Operating Margins: 47.3%

Moody’s LTM EBIT margin of 44.9% reflects the company’s highly scalable business model. Its ratings business generates exceptional margins because the cost of producing additional credit assessments is minimal relative to the fee earned. And the analytics segment benefits from software-like recurring revenue streams.

The company’s three-year EBITDA CAGR of 19.2% reflects both revenue growth and disciplined cost management. And AI integration could drive further operating leverage by improving research production efficiency.

Based on analysts’ consensus estimates, we used a 47.3% operating margin assumption for MCO. This reflects continued operating leverage from subscription growth and AI-driven efficiency gains across research and ratings operations.

3. Exit P/E Multiple: 26.2x

MCO currently trades at an NTM P/E of 26.2x, reflecting its high-quality earnings profile and regulatory moat as one of the three dominant global credit rating agencies. Its LTM P/E is 32.2x, and the Street target of $535 confirms analyst confidence in near-term fundamentals.

Based on analysts’ consensus estimates, we used a 26.2x exit P/E multiple for MCO. This assumes modest multiple compression from current levels as growth moderates, while still reflecting Moody’s durable competitive advantages and pricing power.

MCO’s 1.0% dividend yield and quarterly cash dividend of $1.03 per share add a modest income component to total returns. And CEO Robert Fauber continues to execute with consistent strategic discipline.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

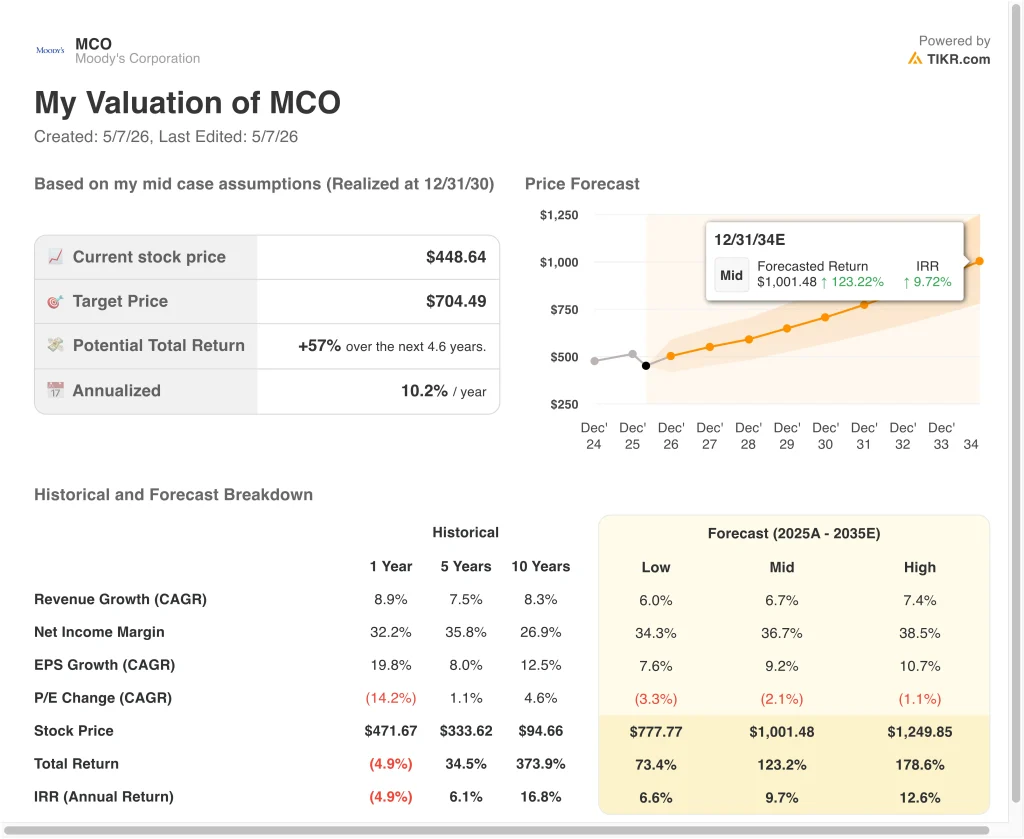

Different scenarios for MCO stock through 2030 show varied outcomes based on analytics growth, debt market conditions, and AI product monetization (these are estimates, not guaranteed returns):

- Low Case: Debt issuance slows, and AI product adoption disappoints → 6.6% annual returns

- Mid Case: Analytics subscriptions grow steadily, and AI tools gain traction → 9.7% annual returns

- High Case: AI-powered risk intelligence unlocks faster growth and margin expansion → 12.6% annual returns

Going forward, Moody’s setup is solid but not exceptional at current prices. The 11.3% annualized return from the guided model is above the 10% threshold that typically signals an attractive long-term investment. But investors should monitor debt issuance trends and the pace of Moody’s AI product monetization as the key indicators of whether the higher-end return scenarios become achievable.

See what analysts think about MCO stock right now (Free with TIKR) >>>

Should You Invest in Moody’s Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up MCO, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track MCO alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Moody’s stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!