Key Takeaways:

- Elastic provides a search and analytics platform used by organizations worldwide for search, observability (system health monitoring), and security, with Q3 FY2026 revenue growing 18% year-over-year and sales-led subscription revenue up 21% to $376 million.

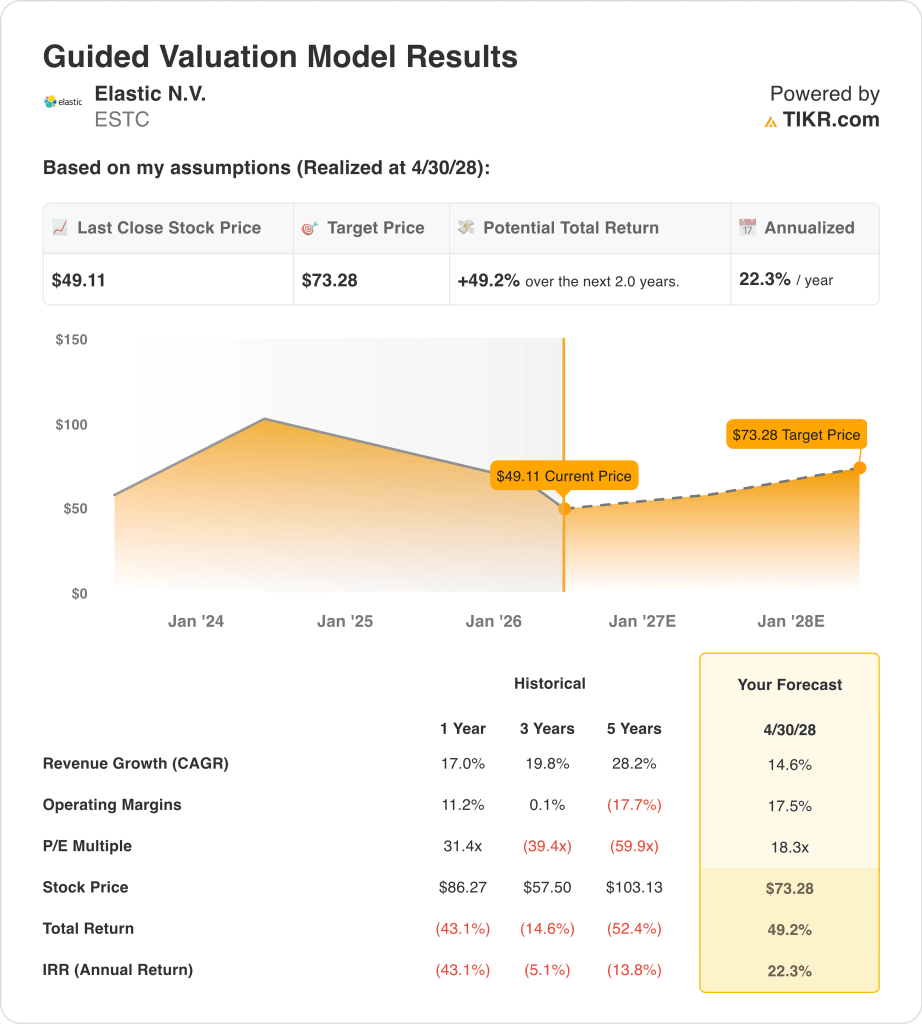

- ESTC stock could reasonably reach $73 per share by mid-2028, based on our valuation assumptions.

- This implies a total return of around 49% from today’s price of $49, with an annualized return of 22.3% over the next 2.0 years.

What Happened?

Elastic (ESTC) is one of the most beaten-down software stocks of 2026. The stock has fallen around 49% from its 52-week high of $96 to trade near $49. Yet the business continues to grow at a strong pace. And Q3 FY2026 results showed 18% revenue growth year-over-year, beating analyst expectations, according to Reuters.

The operational results are actually quite encouraging. Elastic’s Q3 adjusted EPS came in at $0.73, well above the estimate of $0.65. And sales-led subscription revenue grew 21% year-over-year to $376 million. The company also secured FedRAMP High authorization on AWS GovCloud, opening the door to more federal government contracts.

Elastic is also deepening its AI integrations. The company expanded its collaboration with NVIDIA on GPU-accelerated vector indexing in Elasticsearch, its core search database. And it added Jina Embeddings v3 to Google’s Gemini Enterprise Model Garden, strengthening its AI-native search capabilities. So Elastic is well-positioned in the fast-growing enterprise AI search market.

The company’s LTM gross margin is 76.1%, but its LTM EBIT margin is slightly negative at around 1.6%. Elastic is investing aggressively in growth and approaching a key inflection point toward profitability. And it announced a $500 million share repurchase program in October 2025, signaling management confidence in the business.

Here’s why Elastic stock could offer some of the most compelling return potential in software despite its steep recent decline.

What the Model Says for Elastic Stock

We analyzed the upside potential for Elastic stock based on its improving profitability trajectory, strong subscription revenue growth, and expanding AI-native platform capabilities across search, observability, and security.

Based on estimates of 14.6% annual revenue growth, 17.5% operating margins, and a normalized P/E multiple of 18.3x, the model projects Elastic stock could rise from $49 to $73 per share.

That would be a 49% total return, or a 22.3% annualized return over the next 2.0 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for ESTC stock:

1. Revenue Growth: 14.6%

Elastic’s Q3 FY2026 revenue grew 18% year-over-year, and sales-led subscription revenue grew 21% to $376 million. The company’s forward two-year revenue CAGR is projected at around 15.2%. And its three-year historical revenue CAGR of 19.8% shows strong underlying momentum.

Elastic recently eliminated per-endpoint pricing for its Elastic Security XDR product (a unified threat detection and response tool), potentially broadening adoption among cost-conscious enterprise buyers. And FedRAMP High authorization on AWS GovCloud opens a large new government revenue channel.

Based on analysts’ consensus estimates, we used a 14.6% revenue growth forecast for ESTC. This reflects continued cloud transition tailwinds, strong government contract momentum, and growing AI-driven enterprise search demand.

2. Operating Margins: 17.5%

Elastic’s LTM EBIT margin is slightly negative at around 1.6%, as the company invests aggressively in product and go-to-market capabilities. But its LTM gross margin of 76.1% provides a strong foundation for margin expansion. And the company’s forward two-year EBITDA CAGR is projected at around 20.9%.

New GPU-accelerated capabilities and deeper integrations with cloud providers like AWS and Google Cloud support this expansion trajectory. And operating leverage should improve meaningfully as the revenue base grows.

Based on analysts’ consensus estimates, we used a 17.5% operating margin assumption for ESTC. This reflects Elastic’s path to profitability as revenue scale improves and investment spending normalizes relative to revenue.

3. Exit P/E Multiple: 18.3x

ESTC currently trades at an NTM P/E of 18.3x, which is low relative to high-growth software peers. Its significant pullback from $96 to $49 has compressed the multiple substantially. And the analyst consensus target of $79 implies around 61% upside from current levels.

Based on analysts’ consensus estimates, we used an 18.3x exit P/E multiple for ESTC. This reflects a conservative assumption for a company growing at a mid-to-high teens revenue growth rate. But it also accounts for the near-term profitability ramp still underway.

Elastic announced a $500 million share repurchase program in October 2025, signaling management confidence in the business. And the stock’s deep pullback means the company can retire a larger percentage of its shares at depressed prices. So capital allocation is beginning to add another dimension to the ESTC investment case.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for ESTC stock through 2030 show varied outcomes based on revenue growth, margin expansion, and platform adoption (these are estimates, not guaranteed returns):

- Low Case: Revenue growth slows, and profitability improvements disappoint → 6.0% annual returns

- Mid Case: Strong subscription growth and improving margins drive a recovery → 9.7% annual returns

- High Case: AI-driven demand and platform expansion unlock faster growth → 13.1% annual returns

Going forward, Elastic’s setup is compelling but requires consistent execution. The guided model’s 22.3% annualized return over 2.0 years is well above the 15% threshold that typically signals an undervalued or high-growth opportunity.

But investors should track revenue growth consistency and the pace of margin improvement closely, as these two drivers will determine whether ESTC can sustain its recovery from current lows.

See what analysts think about ESTC stock right now (Free with TIKR) >>>

Should You Invest in Elastic?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ESTC, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track ESTC alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Elastic stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!