Key Stats for Occidental Petroleum Stock

- Current Price: $60.58

- Target Price (Mid): ~$58

- Street Target: ~$64

- Potential Total Return (Mid): ~(4%)

- Annualized IRR: ~(1%) / year

- Earnings Reaction (Q4 2025): +9.38% (February 18, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Energy stocks are recalibrating. Occidental Petroleum (OXY) climbed as much as 58% year-to-date in 2026, then gave back ground fast. When Iran and the U.S. reached a ceasefire framework in mid-April and the Strait of Hormuz reopened to commercial shipping, crude oil fell sharply, and OXY dropped 5.42% on April 17 alone.

The stock now sits at $60.58, roughly 10% below its 52-week high of $67.45. Bulls say the structural improvements to the business are intact. Bears point to a TIKR model fair value of around $58, which implies OXY is already trading above what the fundamentals support. With Q1 results arriving May 5, the earnings call will go a long way toward settling that debate.

The Rally, the Reversal, and What Remains

Three catalysts drove the 2026 surge. Occidental completed the $9.7 billion sale of OxyChem to Berkshire Hathaway on January 2, using the proceeds to cut principal debt by $5.8 billion to a stated target of $15 billion. U.S.-Israel airstrikes on Iran then triggered a partial blockade of the Strait of Hormuz, which handles roughly a quarter of the world’s maritime oil trade, sending WTI crude toward $100 per barrel. And Oxy delivered five consecutive quarters of EBITDA beats ranging from 6.4% to 11.7% above consensus according to TIKR’s Beats & Misses data, showing the cost improvements were real.

The ceasefire removed the commodity overlay. That is the right frame for the pullback: not a deterioration in the business, but a temporary supply-disruption premium that was always going to unwind. What remains is a leaner company with a materially better balance sheet than it had a year ago. The question is whether $60.58 still prices in oil conditions that no longer exist.

What the Q4 Call Said That Investors Should Not Miss

Most coverage of OXY in 2026 has focused on the oil price and the OxyChem sale. The Q4 transcript contains something more durable. CEO Vicki Hollub, President and Chief Executive Officer, told analysts that the global oil industry’s reserve replacement ratio is now “less than 25%,” meaning the industry as a whole is replacing fewer than one barrel in four of what it produces each year. She argued that oil supply and demand will “get much closer to being in balance” by 2027, driven by structural reservoir depletion across the industry.

Oxy is among the few large producers actually replacing what it produces. The 2025 organic reserves replacement ratio came in at 107%, the all-in ratio at 98%, both at a finding and development cost below the depreciation rate. The total resource base now stands at 16.5 billion BOE (barrels of oil equivalent, covering oil, gas, and natural gas liquids), with 84% breaking even below $50 per barrel.

The operational progress reinforces that picture. COO Richard Jackson told analysts Oxy has achieved “approximately $2 billion in annual oil and gas cost savings across capital and operating expense categories” since 2023, with a further $500 million targeted for 2026: $300 million from capital and $200 million from operating and transportation costs.

New well costs fell 15% in 2025. Full-year 2025 production hit a record 1.434 million BOE/day while spending $300 million less in oil and gas capital than planned. These gains come from concrete changes: more wells per pad, longer laterals, and wider use of simul-frac technology (a completion method fracturing multiple wells simultaneously), which scaled from 10% to nearly 40% of Oxy’s U.S. portfolio.

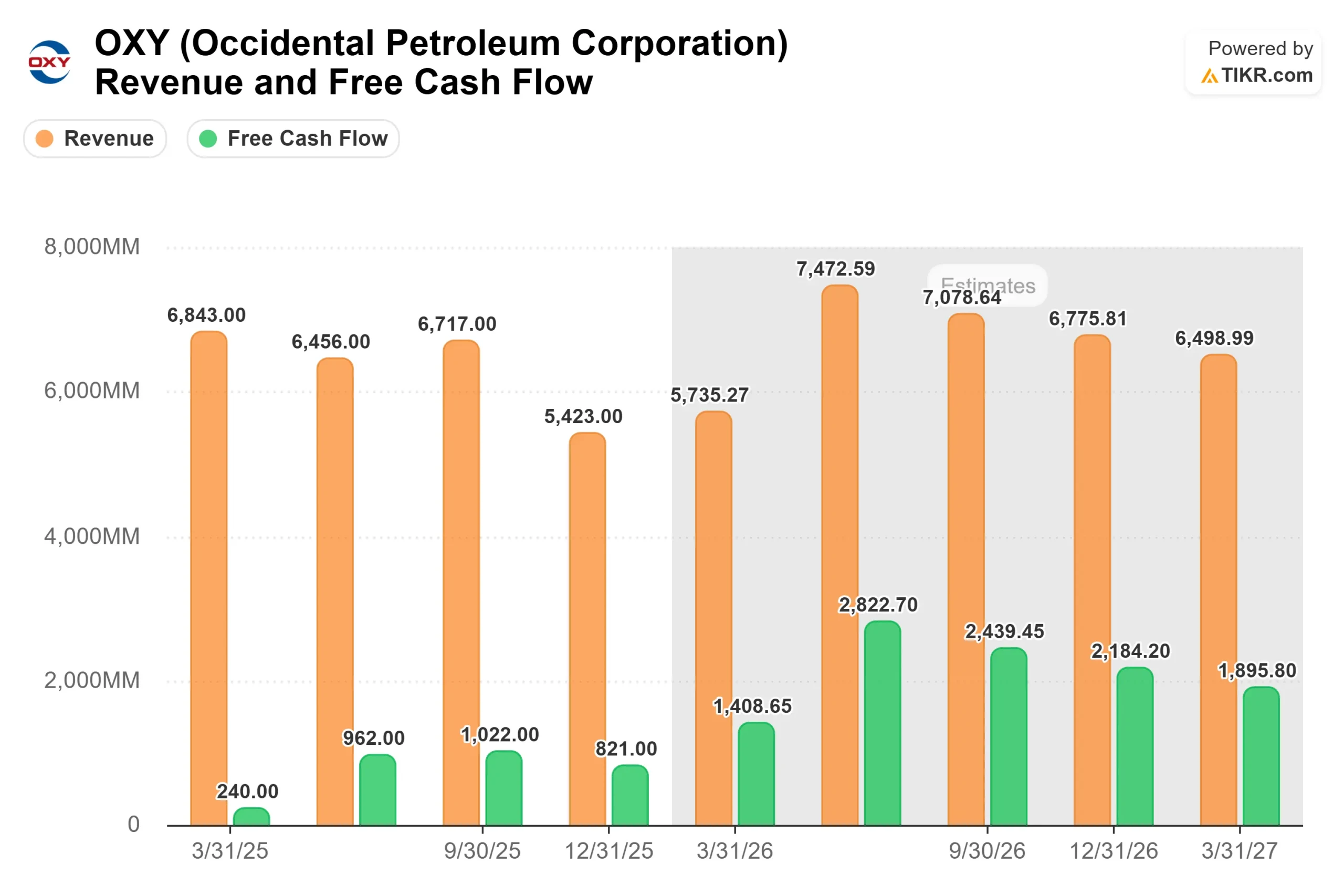

On the balance sheet, CFO Sunil Mathew guided free cash flow improvement of more than $1.2 billion in 2026, driven by the $500 million in oil and gas savings, $400 million in midstream improvements, and approximately $365 million in annual interest savings. TIKR consensus estimates put 2026 free cash flow at around $7 billion, more than double the $3.045 billion reported in 2025. Near-term debt maturities are minimal: approximately $450 million due over the next four years, down from $5.5 billion for the same period at Q3 2025 end.

See historical and forward estimates for Occidental Petroleum stock (It’s free!) >>>

Is Occidental Petroleum Undervalued Today?

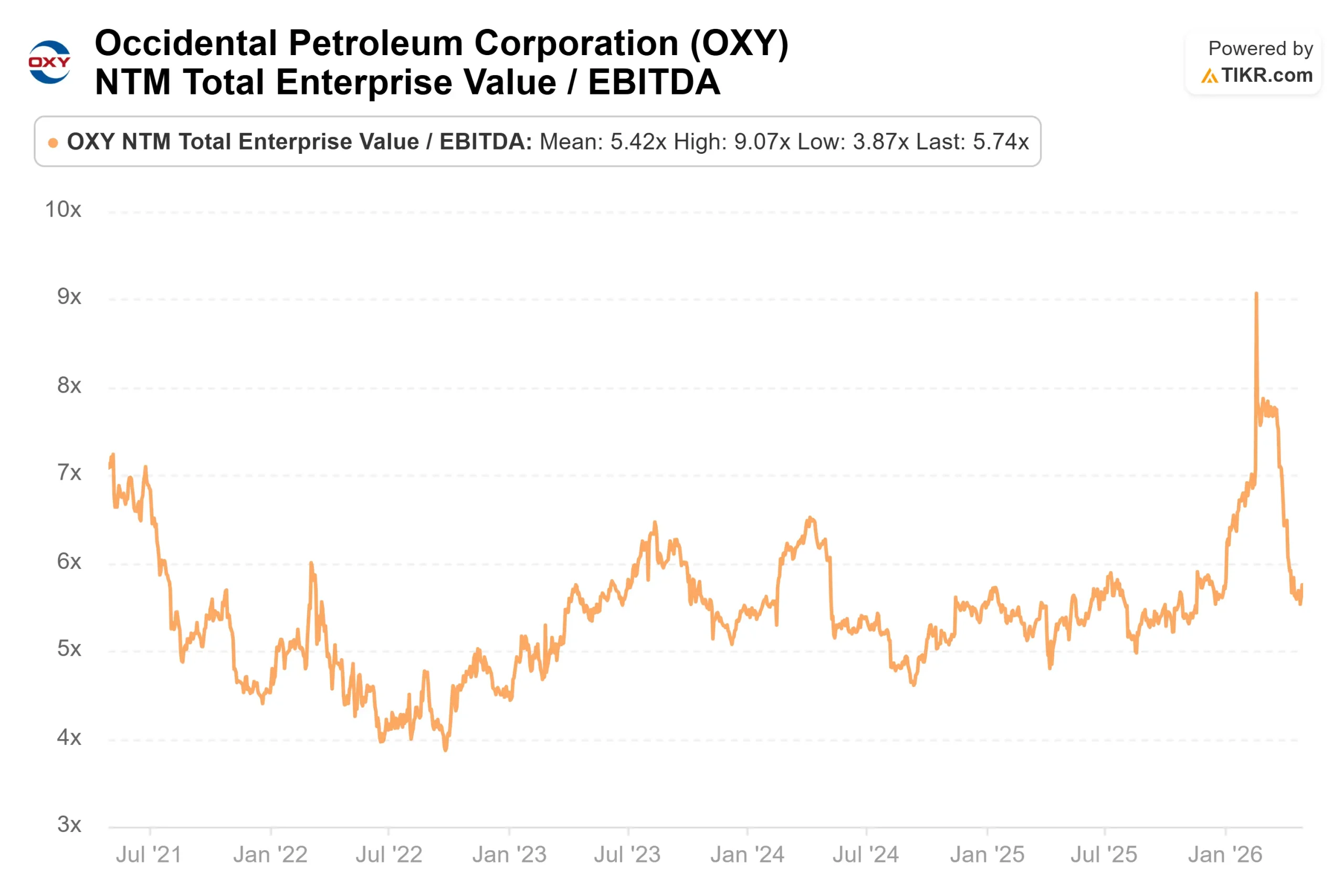

At $60.58, OXY trades at 5.74x NTM EV/EBITDA (enterprise value relative to forward EBITDA, a standard measure of operational value). That sits above the 52-company peer median of 4.89x on TIKR’s Competitors page. ExxonMobil trades at 7.73x and Canadian Natural Resources at 6.69x. OXY’s premium to the peer median narrowed sharply since December 2025, when it traded at 6.70x, suggesting the market has already stripped out most of the geopolitical oil premium.

The Street is modestly more constructive than the TIKR model. The mean analyst price target is ~$64 based on 6 Buys, 1 Outperform, 15 Holds, 1 Underperform, and 2 Sells across 25 analysts per TIKR’s Street Targets data as of April 30, 2026. The heavy Hold count signals Wall Street acknowledges the structural progress but sees limited upside at current prices.

See how Occidental Petroleum performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $60.58

- Target Price (Mid): ~$58

- Potential Total Return (Mid): ~(4%)

- Annualized IRR: ~(1%) / year

See analysts’ growth forecasts and price targets for Occidental Petroleum stock (It’s free!) >>>

The TIKR mid-case model puts fair value at around $58, below today’s $60.58, which is why total return comes in at around negative 4% from the current entry price. The two revenue CAGR drivers are modest Permian production growth of around 1% annually and a gradual recovery in revenue toward around $27 billion in 2026 from $22.1 billion in 2025. The margin driver is the cost-reduction program, with net income margins expected to expand from 12.5% in the trailing twelve months to around 16% in the mid case. TIKR consensus estimates show revenue declining again in 2027 by around 8% as crude normalizes, which is the bear case in one sentence: this is a commodity story, and the commodity tailwind may already be fading.

The high case, which targets around $72, requires sustained elevated oil prices and production above 1.5 million BOE/day. The low case of around $51 models a deeper crude reversion and multiple compressions. If Hollub’s supply thesis proves correct and the industry’s reserve replacement crisis tightens the oil market structurally by 2027, the high case becomes more achievable. If the ceasefire holds and OPEC+ adds supply, the low case comes into view.

Conclusion

Watch one number on the May 5 earnings release: realized oil price per barrel. Oxy’s pre-earnings 8-K filing confirmed that the average worldwide realized oil price in Q1 2026 was $69.91 per barrel, well above Q4 2025’s $58.99 per barrel. If that improvement flowed through to EBITDA at or above the consensus adjusted EPS estimate of $0.70 per share from S&P Global, the free cash flow recovery is on track, and the cost-savings story holds. OXY is a structurally improved company trading modestly above the TIKR model’s fair value estimate, with a five-day earnings catalyst that will tell investors whether the April pullback was an entry point or a warning.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Occidental Petroleum?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Occidental Petroleum, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Occidental Petroleum alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Occidental Petroleum on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!