Key Stats for Datadog Stock

- 52-Week Range: $91 to $202

- Current Price: $147

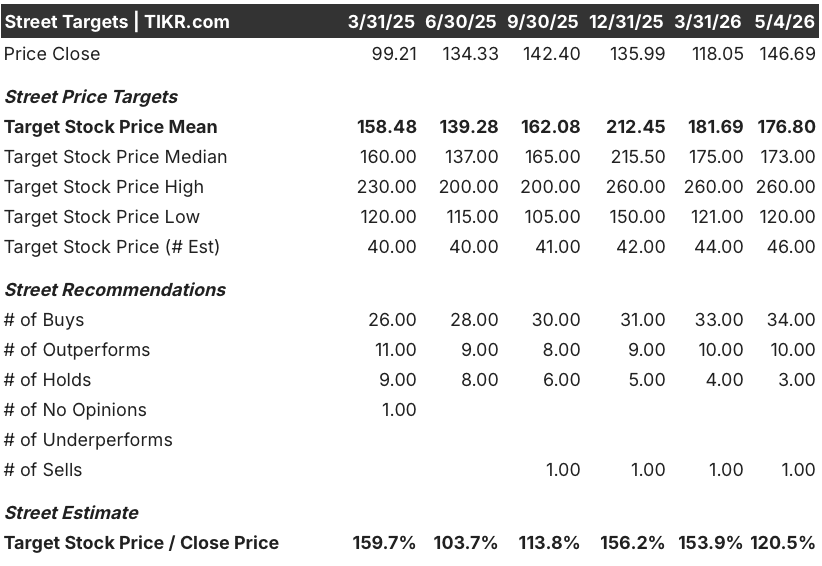

- Street Mean Target: $177

- Street High Target: $260

- Analyst consensus: 34 Buys / 10 Outperforms / 3 Holds / 0 Underperforms / 1 Sell.

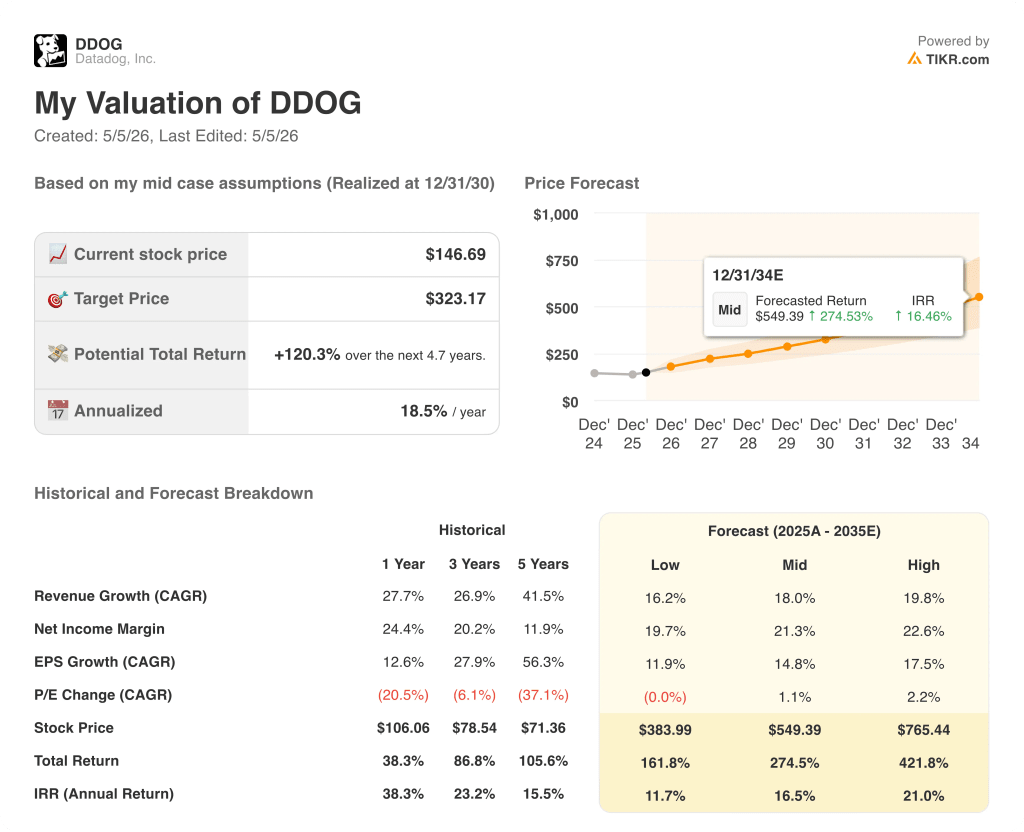

- TIKR Model Target (Dec. 2030): $323

What Happened?

Datadog (DDOG), the cloud-native observability and security platform used by 32,700 companies to monitor their software infrastructure, is trading at $146.69 after Datadog stock surged alongside software peers as investor sentiment toward the sector reversed sharply from its March lows.

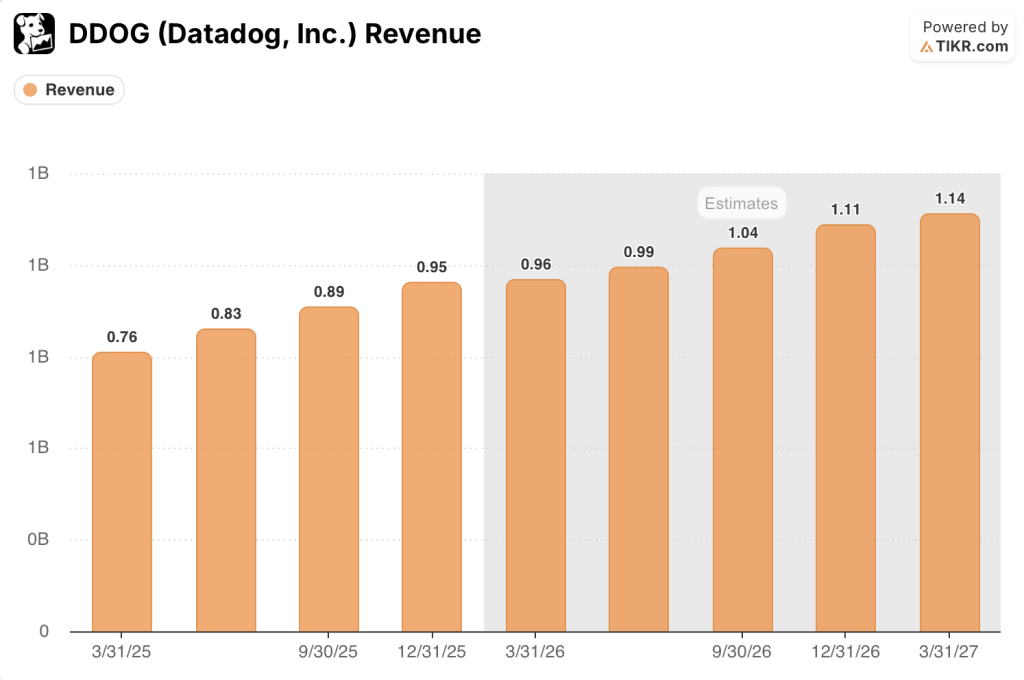

The catalyst was a record Q4 2025 earnings report filed February 10, with revenue hitting $953 million, up 29% year-over-year and above the high end of guidance, alongside record bookings of $1.63 billion, up 37% year-over-year.

The number that reframes the setup is the reacceleration of the non-AI-native core business, where revenue growth climbed to 23% in Q4 from 20% in Q3, proving the platform story extends well beyond a handful of AI hyperscalers.

Olivier Pomel, Co-Founder and CEO, stated on the Q4 2025 earnings call that “our go-to-market teams executed to a record $1.63 billion in bookings, up 37% year-over-year,” and noted the quarter included 18 deals over $10 million in total contract value, two of which exceeded $100 million.

With 48% of the Fortune 500 now on the platform but median ARR per Fortune 500 customer still under $500,000, Datadog’s multi-year expansion runway is grounded in consolidation economics: 14 of the top 20 AI-native companies are already customers, APM growth reaccelerated to the mid-30% range, and the company’s Bits AI SRE Agent, its autonomous incident-response tool, reached general availability in December with over 2,000 customers running investigations within the first month.

Wall Street’s Take on DDOG Stock

Q4’s acceleration is not a one-quarter event — it is the output of a platform consolidation cycle that has been quietly compressing Datadog’s competitive field for three years, and the forward revenue trajectory now reflects that structural advantage at scale.

Datadog stock’s consensus revenue estimates show around $960 million for Q1 2026E, growing roughly 26% year-over-year, followed by around $990 million in Q2 and around $1.04 billion in Q3, implying the Street expects full-year 2026 revenue near $4.1 billion — estimates set before Q4’s bookings print signaled the core business had re-entered genuine acceleration.

The 44 analysts covering DDOG carry a mean price target of $177, implying roughly 20% upside from the current price, with the bull end of the range reaching $260 — a spread that reflects divergent assumptions about whether AI-native customer growth can offset concentration risk from the company’s largest single customer.

The upside debate hinges on that customer: management explicitly guided for the non-largest-customer business to grow at least 20% in 2026, leaving the largest customer’s trajectory an intentional unknown, and the $260 target bulls are betting the broader platform re-rating outweighs that ambiguity.

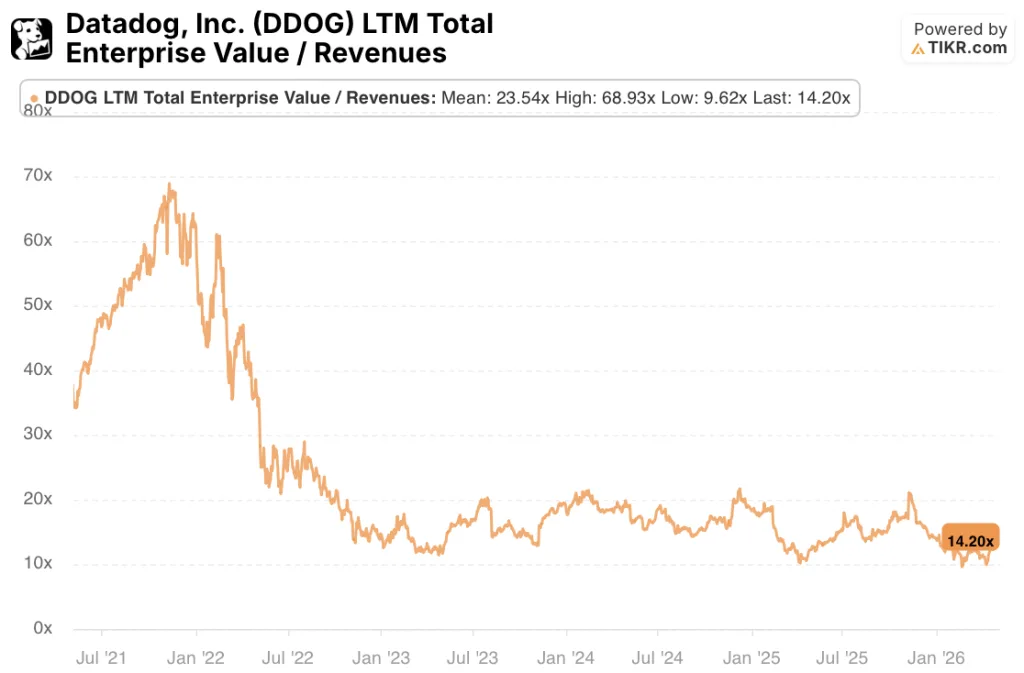

Priced at roughly 14x forward revenue against a business that grew 29% in Q4, Datadog stock appears undervalued relative to its own historical EV/Revenue range, particularly as consensus estimates reflect a deceleration that the record bookings print and core reacceleration data do not yet support.

The Bits AI SRE Agent is not yet reflected in Street estimates as a standalone revenue driver — it is priced as optionality, not as a compounding product line, despite a $500 per 20 investigations price already live on the Datadog website and over 100,000 customer investigations run since GA launch.

If the largest AI-native customer pulls back meaningfully on spending, consensus revenue estimates for the second half of 2026 could undershoot by a margin large enough to compress the multiple before the rest of the platform catches up.

Q1 2026 earnings on May 7 are the next clearing event: the number to watch is whether non-AI-native core revenue growth holds at or above 23%, confirming the reacceleration is structural rather than a pull-forward.

What Does the Valuation Model Say?

TIKR’s mid-case model assigns Datadog a price target of $323, anchored to an 18% revenue CAGR through 2030, a net income margin of around 21%, and EPS growth compounding at roughly 15% annually — assumptions that look conservative against a business that just printed 29% revenue growth and $1.63 billion in bookings in a single quarter.

An 18% forward revenue CAGR in a market Gartner projects will exceed $1 trillion in cloud spend by 2027, with Datadog currently at only 7% logo penetration of its estimated 500,000-customer target market, makes Datadog stock undervalued at $147, where the current multiple prices in a deceleration the bookings and core reacceleration data have not delivered.

The debate centers on whether AI is a compounding flywheel or a near-term concentration risk for Datadog’s growth trajectory over the next three years.

What Has to Go Right

- The non-AI-native core sustains 20%-plus growth: Q4 showed 23% YoY, up from 20% in Q3, driven by APM reacceleration into the mid-30% range and Fortune 500 tool consolidation deals now routinely exceeding $10 million in TCV

- Bits AI SRE Agent converts from trial-stage optionality to a recurring ARR driver: 2,000 customers ran over 100,000 investigations in Q4 alone, with transparent per-investigation pricing already enabling direct revenue attribution

- The 650-customer AI-native cohort continues expanding: 19 already spend over $1 million annually with Datadog, and management cited active inbound interest from additional hyperscaler-level AI labs beyond the two already signed at 8-figure annualized commitments

- Security crosses from 2% of existing customer spend toward the 20-38% range already visible at the company’s most mature accounts, powered by a newly deployed specialist security sales force and Cloud SIEM product maturity following 18x ARR growth over five years

What Could Go Wrong

- Largest AI customer concentration is an unquantified risk: management’s guidance explicitly carves out this customer and applies “very conservative” assumptions, signaling the contribution could range from flat to significantly negative in 2026

- EPS Normalized growth is already decelerating to around 10% in Q1 2026E from 20% in Q4 2025, meaning any revenue miss converts to margin pressure faster than the stock’s premium multiple can absorb

- The observability category faces an accelerating open-source plus frontier-model challenge as customers explore whether general-purpose AI agents can substitute for dedicated monitoring platforms, a risk Datadog’s CEO addressed on the Q4 call without fully dismissing

- Net revenue retention of around 120% is stable but not expanding, and any normalization below 115% would signal platform expansion is reaching saturation in the existing base before new logos replace the growth

Should You Invest in Datadog, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Datadog, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Datadog, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze DDOG stock on TIKR for Free →