Key Stats

- Current Price: €286 (May 6, 2026 close, up ~2%)

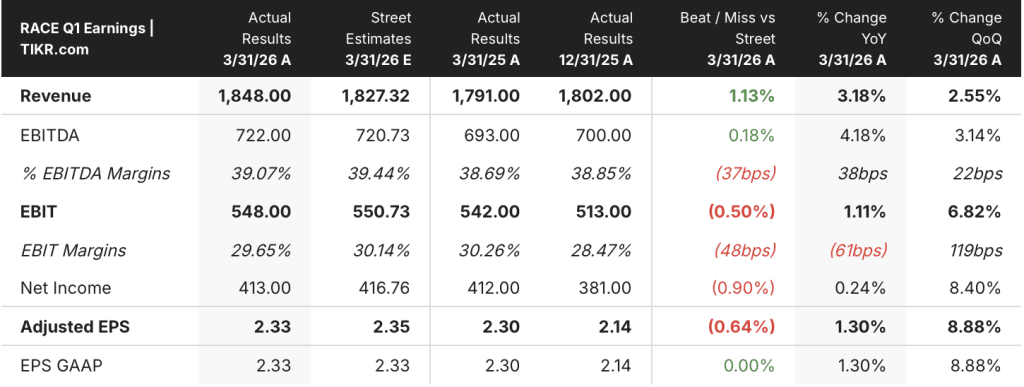

- Q1 2026 Revenue: €1,848M, up 3% YoY (up 6% at constant currency)

- Q1 2026 EBITDA: €722M, up 4% YoY; EBITDA margin 39%

- Q1 2026 EBIT: €548M, up 1% YoY; EBIT margin 30%

- Q1 2026 Adjusted EPS: €2.33, up 1% YoY

- Q1 2026 Industrial Free Cash Flow: >€650M

- Order Book: Extended to end of 2027

- Full-Year 2026 Guidance: Confirmed

- TIKR Model Price Target: €449 (mid case)

- Implied Upside: ~57%

Ferrari Stock Delivers Another Strong Quarter. The Mix Story Is Getting Richer.

Ferrari stock (RACE) rose ~2% on May 6 after Maplebear — correction: Ferrari N.V. reported Q1 2026 revenue of €1,848M, up 3% YoY in reported terms and up 6% at constant currency, beating consensus of €1,827M.

Adjusted EPS came in at €2.33, up 1% YoY, matching GAAP EPS exactly, though marginally below the Street estimate of €2.35 — a negligible gap given that currency headwinds from the U.S. dollar and Japanese yen created approximately €200M of full-year drag, according to CFO Antonio Picca Piccon on the Q1 earnings call.

The revenue beat was driven by sports car mix, personalization, and country mix weighted toward the Americas, with personalizations accounting for approximately 20% of cars and spare parts revenue at constant currency, particularly for the SF90 XX family and the Purosangue.

Deliveries of the Dodici Cilindri family, the Purosangue, and the SF90 XX family all increased in Q1, while the 296 family and Roma Spider declined in line with their model life cycles, and the F80 remained in ramp-up phase.

The 296 Speciale family, the Amalfi Spider, and the 849 Testarossa saw their first shipments in Q1, with all three expected to grow their delivery contribution through the rest of 2026, according to Picca Piccon.

Sponsorship, commercial, and brand revenues increased on higher sponsorships, licensing activity, and a one-time commercial item of less than €10M, plus incremental engine rental revenues from the renewed Haas agreement and the new Cadillac Formula 1 deal.

EBITDA reached €722M, up 4% YoY, with EBITDA margin at 39% — ahead of the prior-year quarter’s 39% and sequentially above Q4 2025’s 39%, while EBIT margin contracted 61 basis points YoY to 30%, driven by higher depreciation tied to new model production start and elevated SG&A from the Amalfi Spider launch, the second-phase Ferrari Luce reveal, and the opening of the London Old Bond Street flagship store.

Industrial free cash flow exceeded €650M, supported by profitability growth and a positive working capital swing including net advances from clients.

Management confirmed full-year 2026 guidance, noting that H1 profitability will be slightly better balanced with H2 than originally planned, a result of pulling forward deliveries to other regions during the initial weeks of the Middle East conflict.

The order book extended further toward end of 2027 during Q1, with all current models contributing to intake, and the Ferrari Luce world premiere set for May 25 in Rome, after which the company will begin taking orders.

Ferrari stock’s investment case heading into the Luce launch rests on whether the company can sustain its mix-driven margin structure through a year where currency headwinds, higher D&A, and elevated SG&A are all running simultaneously.

Ferrari Stock Valuation Model Results (TIKR)

The TIKR model values Ferrari stock at €449 in the mid case, implying ~57% upside from the May 6 close of €286, with a 10% annualized return over the next ~5years.

The mid case assumes a revenue CAGR of 6.1% through 2035 and a net income margin of 24%, with EPS growing at an 8.7% CAGR and the model reaching €649 per share by December 2034.

The low case, at a 5.5% revenue CAGR and 22% net income margin, still implies a stock price of ~€505 by 2034, representing roughly 77% total return from current levels.

The high case, at a 6.7% revenue CAGR and 25% net income margin, puts the stock at ~€808 by 2034, a total return of 182%.

Q1’s mix execution and free cash flow discipline support the mid-case trajectory, though the 61-basis-point EBIT margin compression and the guided moderation in H2 mix lift suggest the margin expansion path will require the Luce launch to deliver on its commercial promise.

Ferrari stock enters its most consequential product cycle in years: a confirmed order book through end of 2027 and the Luce premiere in 20 days set up the long-term thesis, while currency headwinds and deliberate reinvestment spending are compressing near-term margins.

Near-Term

- Full-year FX headwind remains approximately €200M, a figure Picca Piccon confirmed has not changed despite currency volatility

- EBIT margin contracted 61 basis points YoY to 30% in Q1, with higher D&A tied to new model production and SG&A elevated by simultaneous launch activity across Amalfi Spider, Ferrari Luce reveal, and the London store opening

- H1 profitability balance is slightly stronger than originally planned due to rerouted Middle East deliveries, reducing the sequential tailwind management had anticipated from H2 mix ramp

- The 296 family volume decline and Daytona SP3 phaseout are creating a near-term delivery gap that F80 ramp and 296 Speciale must fill through the year

Long-Term

Personalization held at 20% of cars and spare parts revenue in Q1, and the Purosangue Handling Speciale package signals incremental monetization of the existing installed base without requiring new model launches

The order book extended further toward end of 2027 in Q1, with all current models contributing to intake and no abnormal cancellations reported from the Middle East

The Ferrari Luce world premiere on May 25 is oversubscribed, with more than 100 additional client requests turned away, suggesting commercial demand well ahead of supply constraints

The F80 is transitioning to global distribution, the 296 Speciale is growing through 2026, and the 849 Testarossa represents an entirely new revenue contributor entering the mix

Should You Invest in Ferrari N.V.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Ferrari stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Ferrari N.V. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze RACE stock on TIKR for Free →