Key Takeaways:

- Marathon Petroleum Corporation (MPC) is one of the largest independent petroleum refining, marketing, and transportation companies in the United States, with a market cap of around $72 billion.

- MPC reported Q1 2026 adjusted EPS of $1.65, more than doubling the Wall Street consensus estimate of $0.75, driven by elevated refining margins tied to the Middle East conflict.

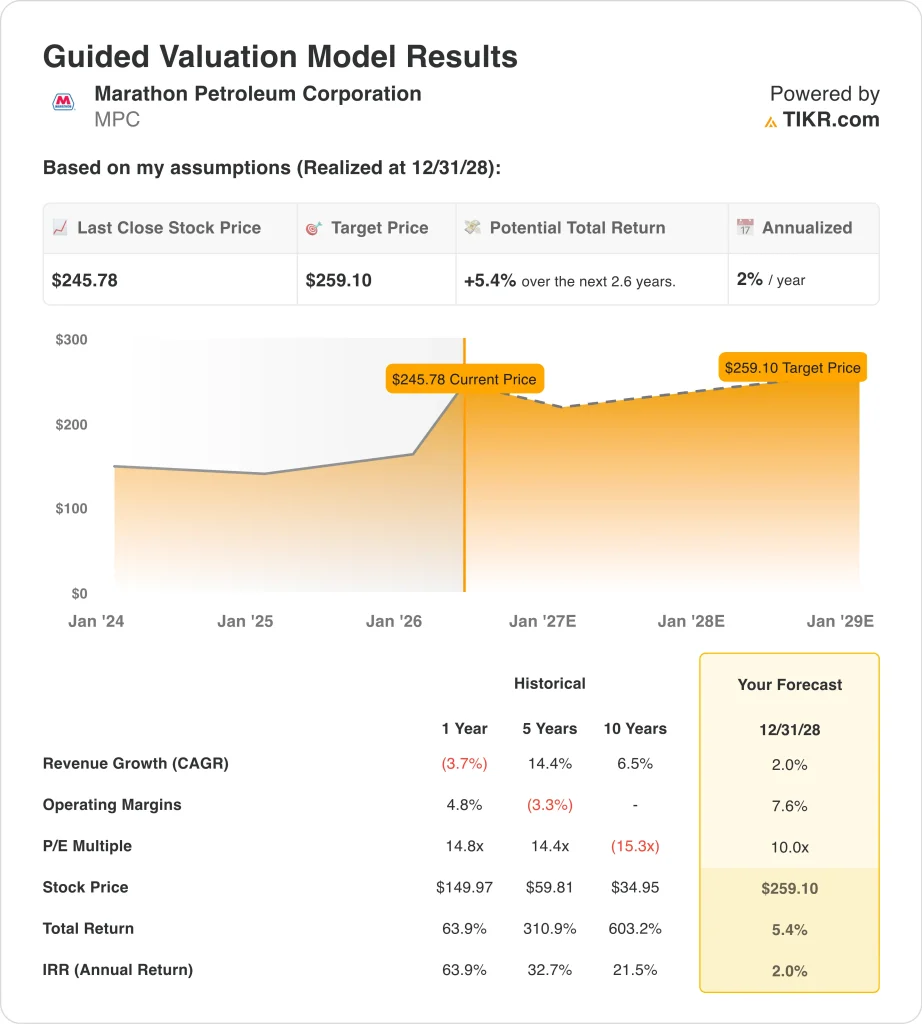

- The model projects MPC stock could rise from $246 to around $259 per share by December 2028, implying a 5.4% total return.

- That works out to just around 2% in annualized returns over the next 2.6 years, suggesting the stock is approaching full valuation at current prices.

What Happened?

Marathon Petroleum Corporation (MPC) delivered one of the biggest earnings beats of the quarter. Adjusted EPS came in at $1.65, more than doubling the consensus estimate of $0.75. Net income returned to $511 million after a loss in Q1 of the prior year. The Iran conflict dramatically widened refining margins and powered the quarter’s exceptional results.

The geopolitical backdrop has been a major tailwind for US refiners. Oil supply disruptions from the Middle East raised the spread between crude input costs and refined product prices. This spread is often called the crack spread, and it is the core profit driver for refining businesses. But early reports of a potential US-Iran deal sent energy stocks sharply lower in early May 2026.

Management also moved quickly on the capital structure and leadership front. Marathon secured a new $5 billion five-year revolving credit facility in April 2026. The company appointed Maria Khoury as CFO and Maryann Mannen as Chairman. Marathon also declared a $1.00 quarterly dividend, payable May 20, 2026, rewarding shareholders directly.

Investors are now debating whether the current margin environment is sustainable. The stock fell over 5% on May 6 as oil prices dropped on Iran deal speculation. This sharp reaction shows how sensitive the stock is to geopolitical headlines.

Here’s why Marathon Petroleum stock could face a more modest return path over the next few years despite the strong earnings momentum.

What the Model Says for MPC Stock

We analyzed the upside potential for Marathon Petroleum stock based on its refining capacity utilization, normalized crack spread assumptions, and capital return discipline.

Based on estimates of 2.0% annual revenue growth, 7.6% operating margins, and a normalized P/E multiple of 10.0x, the model projects Marathon Petroleum stock could rise from $246 to around $259 per share.

That would be a 5.4% total return, or a 2.0% annualized return over the next 2.6 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for MPC stock:

1. Revenue Growth: 2%

Marathon Petroleum reported Q1 2026 adjusted EPS of $1.65, which crushed the consensus estimate of $0.75. Q4 2025 adjusted EPS of $4.07 also significantly beat expectations of $2.88. But both beats were driven by an unusual geopolitical backdrop and do not reflect a structurally higher revenue baseline for the business.

The forward two-year consensus revenue CAGR is approximately 0.2% negative, reflecting analyst expectations for moderation as the Iran tailwind eventually fades. Marathon’s refining volumes are largely capacity-constrained, so top-line growth depends on product prices and throughput levels. Management guided Q1 throughputs at 2,770 thousand barrels per day, showing a stable but essentially flat operational picture.

Based on analysts’ consensus estimates, we used a 2.0% annual revenue growth rate. This is modestly above the negative consensus CAGR but reflects the potential for volume gains and modest price improvement. It does not assume a sustained peak refining margin environment going forward.

2. Operating Margins: 7.6%

Marathon Petroleum operates with an LTM EBIT margin of 5.1% and a gross margin of 10.7%. Refining is a thin-margin business in normal conditions, and spreads fluctuate significantly with crude oil dynamics. The current margin environment is temporarily elevated above historical norms due to the Middle East conflict.

The company carries approximately $32.2 billion in net debt and a net debt to EBITDA ratio of 2.72x. This leverage is manageable in the current favorable refining environment. But it could become more burdensome if margins compress back toward normalized long-term averages.

Based on analysts’ consensus estimates, we used 7.6% operating margins. This is a meaningful step up from the current 5.1% EBIT margin but reflects an assumption that spreads remain modestly above long-term averages. It is consistent with a structurally tighter refining supply environment rather than a peak cycle.

3. Exit P/E Multiple: 10x

Marathon Petroleum currently trades at a forward NTM P/E of 8.49x. The stock surged nearly 50% year to date, and the geopolitical tailwind appears largely priced in. The analyst street target of $255 sits just around 4% above the current price of $246, showing limited analyst conviction in further near-term upside.

The 52 week range of $145 to $262 captures how dramatically refining stocks can move with energy market conditions. The stock more than doubled from its 52 week low before pulling back modestly. This positions MPC near the upper end of its recent trading history and creates a challenging entry point for new investors.

Based on analysts’ consensus estimates, we used a 10.0x exit P/E multiple. This is slightly above the current 8.49x NTM P/E and assumes a modest re-rating as the market prices in normalized earnings power. Any further multiple compression toward energy sector historical averages would reduce projected returns.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

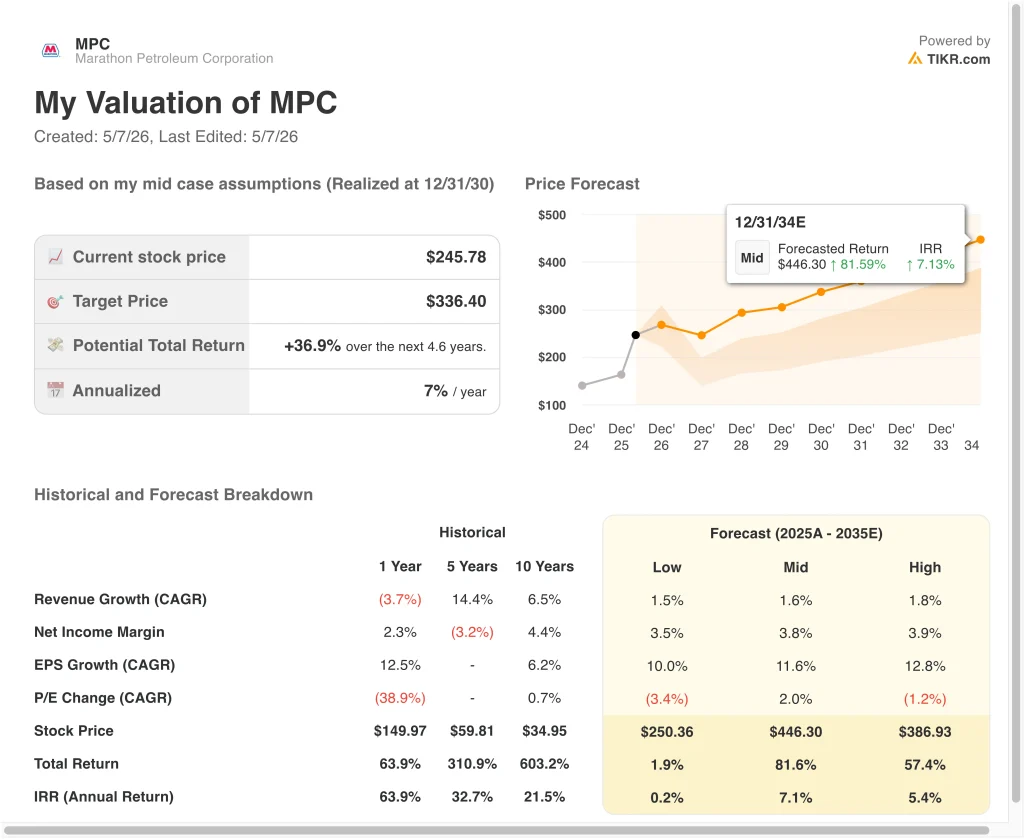

Different scenarios for MPC stock through 2034 show varied outcomes based on refining margin sustainability, crude spread normalization, and geopolitical conditions (these are estimates, not guaranteed returns):

- Low Case: Geopolitical tensions ease, and refining margins compress sharply → around 0% annual returns

- Mid Case: Refining spreads normalize modestly above historical averages with steady volumes → around 7% annual returns

- High Case: Supply constraints persist, but earnings growth trails the mid case assumptions → around 5% annual returns

Going forward, Marathon Petroleum’s stock will move based on refining margin conditions and Middle East geopolitical developments. The model suggests near-term returns are modest, given the stock’s sharp year-to-date rally and its sensitivity to Iran conflict resolution.

Patient investors may find comfort in the quarterly dividend and ongoing share repurchase activity, but the valuation upside from current prices appears limited under most scenarios.

See what analysts think about MPC stock right now (Free with TIKR) >>>

Should You Invest in Marathon Petroleum?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up MPC, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track MPC alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Marathon Petroleum stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!