Key Stats for Marvell Technologies Stock

- 52-Week Range: $57 to $176

- Current Price: $172

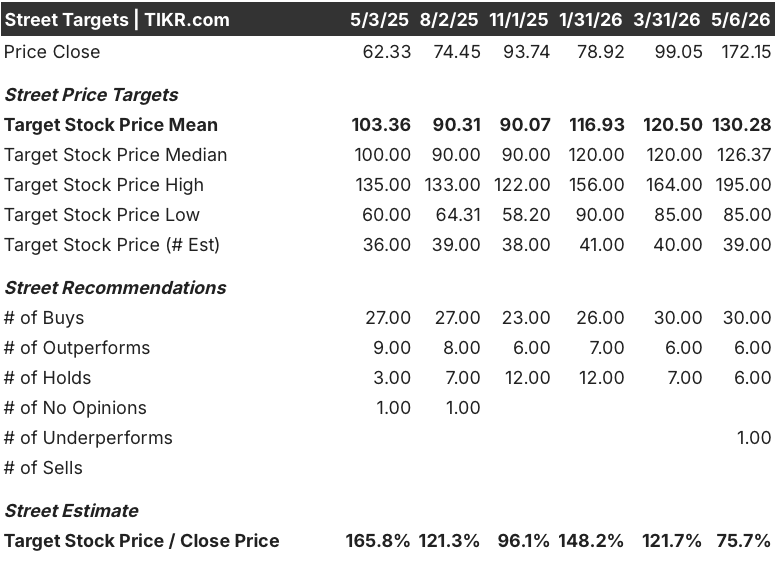

- Street Mean Target: $130

- Street High Target: $195

- Analyst Consensus: 30 Buys / 6 Outperforms / 6 Holds / 1 Underperform

- TIKR Model Target (Dec. 2030): $503

What Happened?

Marvell Technology (MRVL), a fabless semiconductor company that designs custom AI chips and high-speed optical interconnects for data center infrastructure, now trades at $172 — within striking distance of its 52-week high of $176 — after a series of landmark partnerships reset the market’s understanding of what this business is worth.

The move is not speculative.

Nvidia committed $2 billion to Marvell on March 31, integrating MRVL into its NVLink Fusion ecosystem so that Marvell’s custom XPUs (application-specific accelerators built to order for individual hyperscalers) can operate natively within Nvidia-dominated data centers.

On the same day Nvidia’s investment closed, Marvell reported Q4 fiscal 2026 results: revenue of $2.2 billion, up 22% year over year, with adjusted EPS of $0.80 beating the Street estimate of $0.79.

Data center revenue, MRVL’s largest business segment, reached $1.65 billion in Q4, up 21% year over year, driven by surging demand across optical interconnects, custom silicon, and switching products.

CEO Matt Murphy stated on the Q4 fiscal 2026 earnings call that “we expect year-over-year revenue growth to accelerate each quarter in fiscal 2027, driven by continued strength in our data center business, with bookings continuing to grow at a record pace,” anchoring the company’s fiscal 2027 outlook at approaching $11 billion — nearly $1 billion higher than guidance issued just three months prior.

Alphabet’s Google entered talks with Marvell in April to develop two new AI inference chips, including a memory processing unit and a new tensor processing unit (TPU), a deal that would give Marvell a meaningful foothold in Google’s chip ecosystem alongside Broadcom.

Marvell also completed the acquisition of Polariton Technologies in April, adding plasmonics-based silicon photonics technology designed to push optical interconnect bandwidth to 3.2T and beyond, extending MRVL’s lead in the scale-across data center connectivity market where it already expects to supply DCI modules to all five major U.S. hyperscalers this year.

The company’s fiscal 2028 outlook, which calls for revenue approaching $15 billion (roughly 40% growth year over year), is grounded in three converging forces: a custom XPU business expected to at least double year over year, an interconnect business forecast to outpace cloud CapEx growth by a wide margin, and the $3.25 billion Celestial AI acquisition bringing co-packaged optics technology that management targets at a $500 million annualized revenue run rate by Q4 fiscal 2028.

Wall Street’s Take on MRVL Stock

The Nvidia partnership reframes Marvell stock not as a one-customer custom silicon risk, but as the connective tissue of the entire AI infrastructure buildout, which changes the multiyear revenue visibility in a fundamental way.

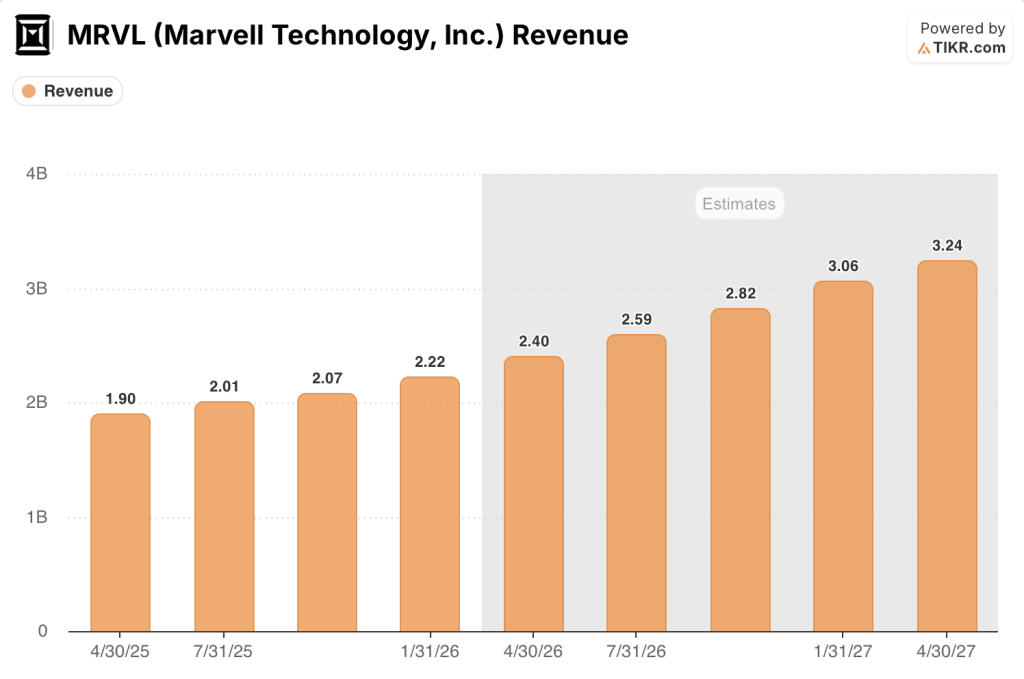

MRVL’s revenue is forecast to reach $2.40 billion in the April 2026 quarter (up around 27% year over year), accelerating to $3.06 billion by January 2027 and $3.24 billion by April 2027, reflecting year-over-year growth rates of around 38% and around 35% respectively, as the interconnect business ramps well above prior CapEx-tracking assumptions.

The 30 Buys, 6 Outperforms, 6 Holds, and 1 Underperform in the coverage table reflect near-universal conviction on the growth trajectory, with a mean price target of $130.28 and a Street high of $195 — but the current price of $172 has outrun that consensus mean by 32%, which is the real debate the data poses.

Barclays, which upgraded Marvell stock to overweight in April with a $150 target, called MRVL “first and foremost an optical company” and projected that optical ports at hyperscalers could double in 2026 and double again in 2027, implying around 90% optical revenue growth for two consecutive years.

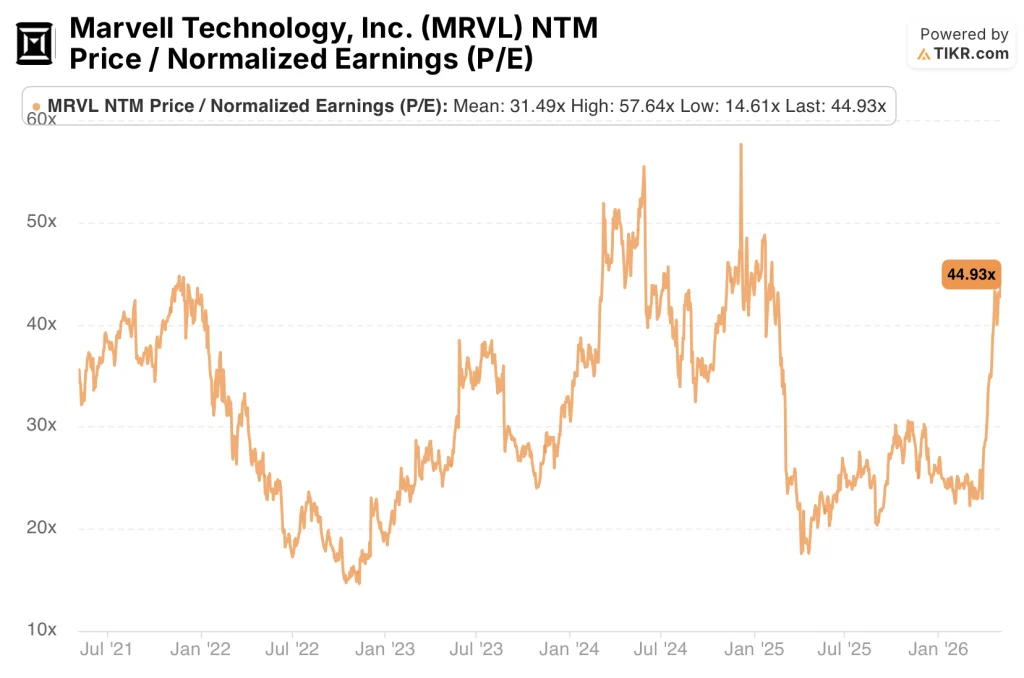

Trading at near 45x forward normalized earnings against a 5-year historical mean of 31x, Marvell stock appears overvalued on a pure multiple basis, though the case for premium pricing rests entirely on whether the fiscal 2028 revenue ramp to $15 billion — and the custom XPU doubling it requires — executes on schedule.

The risk is customer concentration: the top four U.S. hyperscalers account for the majority of data center revenue, and a single program delay or hyperscaler CapEx pullback in fiscal 2028 would put a material dent in the $15 billion revenue target.

The catalyst is the Q1 fiscal 2027 earnings call scheduled for May 27, where management will provide the first sequential data point on whether the interconnect and custom ramps are tracking to the aggressive bookings backlog Murphy described on the March call.

What Does the Valuation Model Say?

The TIKR mid-case model assigns Marvell a target price of around $503 over approximately 5 years, implying a roughly 25% annualized return from current levels, anchored to a revenue CAGR assumption of around 23% and a net income margin expanding toward around 30%, both of which sit comfortably below what the company’s own fiscal 2028 guidance implies.

Marvell stock appears overvalued at the current 44.93x NTM P/E relative to its 31.49x historical mean, though investors pricing in full execution on the $15 billion fiscal 2028 roadmap would argue the premium is earned.

The central tension here is timing: the $15 billion fiscal 2028 revenue target is ambitious, the Celestial AI co-packaged optics program does not reach a $500 million run rate until Q4 fiscal 2028, and the new Tier 1 XPU customer program is not yet in high-volume production.

What Has to Go Right

- The interconnect business sustains around 50% growth in fiscal 2027 as 1.6T PAM products ramp across multiple Tier 1 hyperscalers, with 800G remaining the high-volume baseline.

- The new Tier 1 XPU program (not yet named) moves from development into high-volume manufacturing in fiscal 2028 with purchase order commitments already covering the production corridor management described.

- Celestial AI’s photonic fabric chiplets hit the targeted $500 million annualized revenue run rate exiting fiscal 2028, validating the $3.25 billion acquisition price.

- Google chip partnership progresses from disclosed talks to signed agreements, with design-win revenue beginning to layer into the fiscal 2029 model alongside existing Amazon Trainium and lead XPU customer programs.

- AEC and retimer products more than double year over year in fiscal 2027 (from a roughly $200 million base) as Marvell completes design wins at 3 of the top U.S. hyperscalers.

What Could Go Wrong

- Hyperscaler CapEx growth moderates more sharply than the current fiscal year’s pace in calendar 2027, compressing bookings visibility and potentially pushing the $15 billion revenue target beyond fiscal 2028.

- Google opts to deepen its existing Broadcom relationship rather than formalize a chip co-development agreement with Marvell, removing a key unpriced catalyst from the bull case.

- The new Tier 1 XPU program experiences a development delay, as custom silicon programs routinely do, shifting meaningful fiscal 2028 revenue into fiscal 2029 and creating an air pocket in the custom doubling narrative.

- TSMC advanced node capacity constraints tighten further, given that Marvell relies on leading-edge fabrication for its 2nm DSP and custom XPU programs, a supply risk that COO Chris Koopmans acknowledged remains a structural feature of the AI semiconductor environment.

Should You Invest in Marvell Technology, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Marvell Technology, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Marvell Technology, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze MRVL stock on TIKR for Free →