Key Stats

- Current Price: $108 (May 6, 2026)

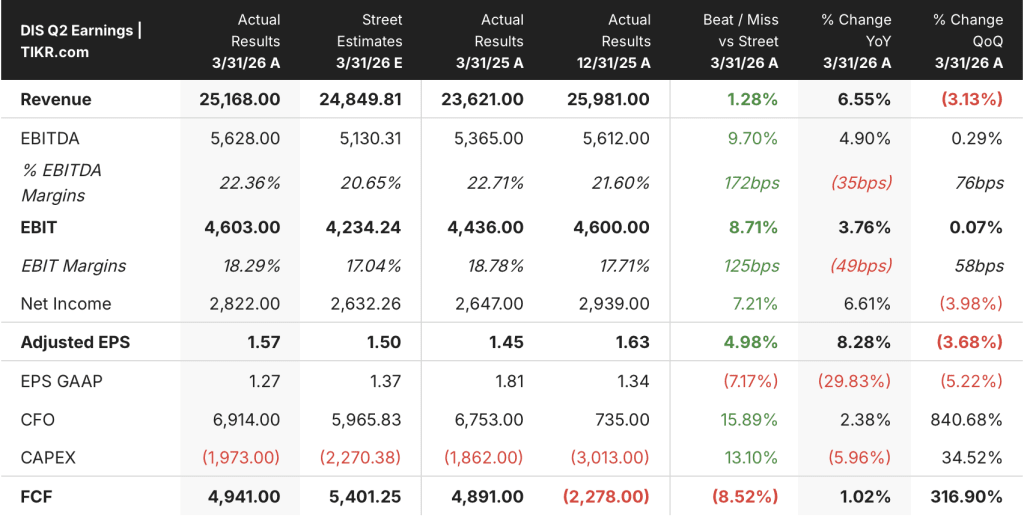

- Q2 FY2026 Revenue: $25.2B, up 7% YoY

- Q2 FY2026 Adjusted EPS: $1.57, up 8% YoY

- Entertainment SVOD Revenue Growth: Accelerated from 11% in Q1 FY2026 to 13% in Q2

- Disney Experiences Revenue Growth: 7% YoY; segment operating income up 5% YoY

- FY2026 Adjusted EPS Guidance: 12% growth (excluding 53rd week impact)

- FY2027 Adjusted EPS Guidance: Double-digit growth (excluding 53rd week impact)

- TIKR Model Price Target: $140

- Implied Upside: ~30%

Disney Stock Posts Q2 Beat as Streaming and Parks Both Outperform

Disney stock (DIS) surged 7.5% on May 6 after The Walt Disney Company reported Q2 FY2026 revenue of $25.2B, up 7% year over year, and adjusted EPS of $1.57, up 8% from $1.45 in the prior-year quarter.

Both results came in ahead of prior guidance, with new CEO Josh D’Amaro attributing the outperformance to stronger-than-expected revenue growth across segments.

Streaming was the standout driver, with Disney Entertainment’s entertainment SVOD revenue accelerating to 13% growth in Q2 from 11% in Q1 FY2026, fueled by both subscriber rate increases and volume gains.

D’Amaro noted on the earnings call that advertising revenue also grew at a double-digit rate compared to the prior-year period.

Disney Experiences delivered $7B-range revenue growth of 7% YoY, with segment operating income rising 5%, both figures representing second quarter records according to D’Amaro.

Domestic parks attendance declined 1% in Q2, but CFO Hugh Johnston stated that excluding international visitation headwinds, attendance would have grown, and that forward bookings for the back half of the year are tracking up strongly.

FY2026 adjusted EPS guidance of 12% growth was reaffirmed, as was double-digit adjusted EPS growth for FY2027, both figures excluding the impact of the 53rd week.

Disney Cruise Line capacity is expanding 40% on a booked occupancy basis that remains in line with the prior year, with the fleet growing from 8 to 13 ships by 2031.

Disney Stock’s Income Statement Shows Margin Stability Under Revenue Acceleration

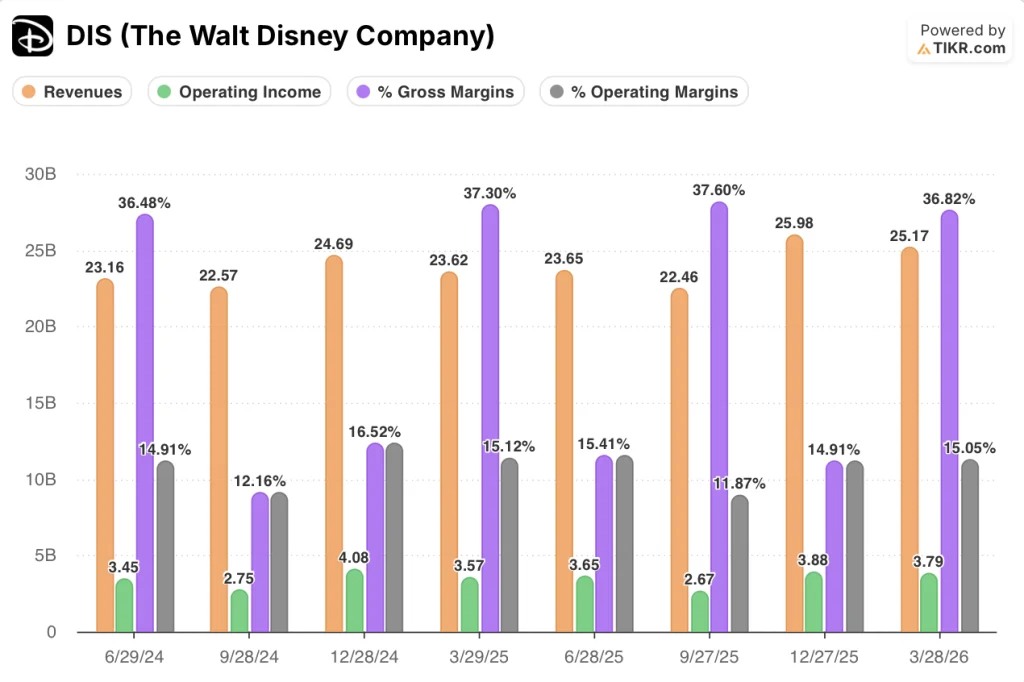

Disney stock’s income statement reflects a company holding operating margins steady while accelerating its top line across the last four reported quarters.

Revenue growth reaccelerated to 6.5% YoY in Q2 FY2026 (the quarter ended 3/28/26) after registering 5.2% growth in the prior quarter and a brief 0.5% decline in Q3 FY2025, recovering the revenue momentum that had been disrupted through mid-fiscal 2025.

Gross margin held at 37% in Q2 FY2026, nearly flat with 37% in Q2 FY2025 and consistent with the 38% peak in Q3 FY2025, indicating that cost structure has not deteriorated despite the stepped-up investment in cruise line expansion and park preopening costs.

Operating income reached $3.79B in Q2 FY2026, up 6% YoY from $3.57B in the prior-year quarter, with operating margin holding at 15% in both periods.

Johnston attributed the limited operating income flow-through in Experiences this quarter specifically to preopening costs for World of Frozen at Disneyland Paris and the Disney Adventure cruise ship, costs that will not recur in the second half of the fiscal year.

Entertainment streaming passed a notable threshold this quarter, with streaming revenue now more than double linear revenue within the Disney Entertainment segment, according to Johnston on the call.

What Does the Valuation Model Say?

The TIKR model prices DIS at $140, implying roughly 30% upside from the current price of $108.

The mid-case assumptions driving that target are a revenue CAGR of around 4% through fiscal 2035 and a net income margin expanding to ~12%, up from the current trailing rate of about 10%.

The Q2 report strengthens the model’s margin expansion premise: SVOD entertainment hit double-digit margins this quarter for the first time, cruise capacity is scaling into confirmed demand, and park preopening costs that compressed Q2 Experiences OI are poised to roll off in Q3.

The risk/reward picture on Disney stock has improved modestly on this print, but the upside is back-loaded. The annualized IRR in the mid case is 5% through fiscal 2034, which prices in steady execution rather than acceleration.

The question for Disney stock investors is not whether this was a good quarter, but whether a 3.5% revenue CAGR is conservative or whether the Disney+ ecosystem buildout and Experiences expansion stall before reaching management’s stated targets.

Disney delivered a clean Q2, but the path from current pricing to the TIKR model’s $140 target requires compounding execution across streaming, parks, and ESPN DTC over the next several years.

Near-Term Strength

- Q2 revenue of $25.2B grew 7% YoY, beating guidance, with Experiences setting second-quarter records for both revenue and segment OI

- Entertainment SVOD margins turned double-digit for the first time this quarter, validating the profitability case management has been building

- Domestic park attendance headwinds tied to international visitation and the Epic Universe opening are expected to ease in Q3, with forward bookings tracking ahead

- Disney Cruise Line’s 40% capacity expansion is running at booked occupancy in line with the prior year, indicating no demand shortfall from the fleet growth

Long-Term Execution Risk

- The TIKR mid-case revenue CAGR of 3.5% assumes consistent growth through fiscal 2035, but revenue growth has been uneven: 6.5% in Q2 FY2026, followed by near-flat performance as recently as Q3 FY2025 at negative 0.5%

- ESPN’s DTC transition remains early-stage after launching in 2025; management has not disclosed subscriber or revenue targets, leaving a key growth assumption effectively unverifiable

- The $140 model price target delivers a 4.9% annualized IRR in the mid case — a return profile that leaves little margin for execution misses on the Experiences expansion or streaming international scaling

- Macro sensitivity is present: Johnston acknowledged that a material further rise in fuel prices from current levels could affect consumer behavior at domestic parks, though no impact has been observed yet

Should You Invest in The Walt Disney Company?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Disney stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Disney stock alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze DIS stock on TIKR for Free →