Key Stats for Home Depot Stock

- 52-Week Range: $310 to $427

- Current Price: $323

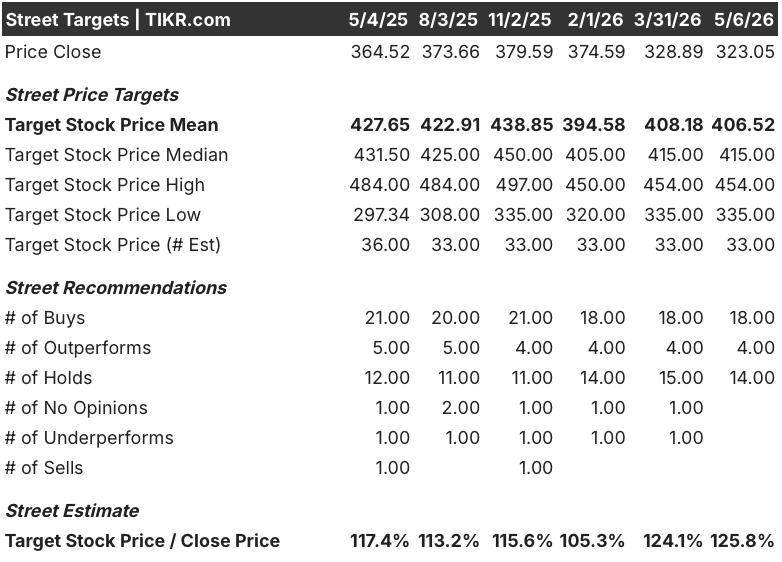

- Street Mean Target: $407

- Street High Target: $454

- Analyst Consensus: 18 Buys / 4 Outperforms / 14 Holds / 1 Underperform

- TIKR Model Target (Dec. 2030): $511

What Happened?

Home Depot (HD), the world’s largest home improvement retailer, beat fourth-quarter earnings estimates and maintained its full-year outlook despite a housing market that has been functionally frozen for three years.

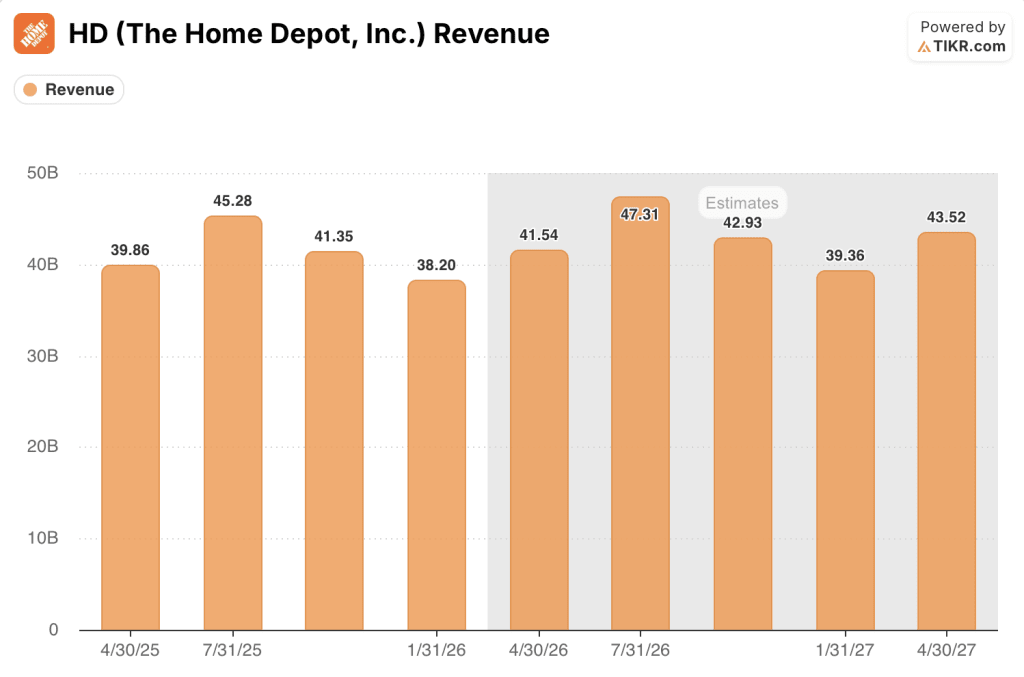

Adjusted diluted EPS came in at $2.72 for the quarter, well ahead of the $2.54 Wall Street expected, while Q4 revenue of $38.2 billion edged past the $38.1 billion consensus.

Comparable sales rose 0.4% for the quarter, with strength from January storm activity and outperformance from professional contractor customers, even as larger discretionary projects from DIY homeowners remained under pressure.

Digital platforms delivered an 11% jump in online sales in Q4, with the company rolling out real-time delivery tracking for big and bulky materials across all categories, a feature the company said improved Pro engagement and incremental transactions.

CFO Richard McPhail stated at the J.P. Morgan Retail Round Up Forum that “we have the right to win every dollar” of the $700 billion Pro addressable market, citing a $1.2 trillion total addressable market after the planned acquisition of HVAC distributor Mingledorff’s expanded the TAM by $100 billion.

Home Depot stock now trades near its 52-week low of $310.40 as management targets 80 new stores by 2027, guides SRS Distribution (its specialty trade wholesale subsidiary) to mid-single-digit organic sales growth in fiscal 2026, and presses forward with an enterprise-wide AI rollout under new Chief Technology Officer Franziska Bell, hired from Ford Motor in April.

Wall Street’s Take on HD Stock

Home Depot stock’s Q4 beat reframes the housing narrative: the question is no longer whether HD can survive the downturn, but how much share it takes before the cycle turns.

HD’s revenue consensus for Q1 FY2026 stands at around $42 billion, growing around 4% year-over-year, with Q2 FY2026 estimates at around $47 billion, also growing around 4-5%, as SRS organic sales are guided to accelerate to mid-single digits after posting low-single-digit growth in 2025 despite industry shingle shipments falling 28% year-over-year in Q4.

Eighteen buy-rated analysts and four outperforms sit alongside fourteen holds, with a mean price target around $407 and a street high of $454; Wall Street is not bearish on HD, but the hold camp reflects a market waiting for the housing inflection McPhail says has not yet arrived.

The target spread from $335 to $454 maps almost precisely to the difference between a housing market that stays frozen through 2027 and one where mortgage rates drift toward 5%, a scenario the bears and bulls each have data supporting at current rate levels.

Trading at roughly 22x forward earnings against a five-year historical forward P/E range closer to 25-28x, and with revenue poised to compound as the SRS and GMS acquisitions annualize across a $1.2 trillion addressable market, Home Depot stock appears undervalued relative to the scope of the Pro franchise being assembled below the stock price.

Home Depot raised its quarterly dividend 1.3% to $2.33 per share even as buybacks remain paused until the company targets a 2.0x leverage ratio, expected sometime in the first half of 2027, signaling management confidence in the free cash flow profile through the downturn.

The specific number to watch is Q1 FY2026 comparable sales growth at the May 19 earnings call, where management has guided for mid-single-digit EPS pressure due to acquisition annualization; the comp trend beneath that noise will show whether the housing bottom is holding.

What Does the Valuation Model Say?

TIKR’s mid-case model prices Home Depot stock at around $511, reflecting around 4% annualized revenue growth and a 10% net income margin assumption through fiscal 2031, anchored by SRS organic sales expanding mid-single digits and the HVAC vertical from Mingledorff’s adding new distribution footprint across five southeastern states.

At roughly 10% annualized returns in the mid case against a current price of $323, Home Depot stock is undervalued for investors with a multi-year horizon, with the IRR expanding to around 11% in the high case as housing turnover recovers and the $700 billion Pro wallet share gains compound.

The investment hinges on a single question: how long does the housing lock-in last, and how much share does Home Depot capture before the cycle ends?

What Has to Go Right

- Mortgage rates declining toward 5-6% unlock pent-up housing turnover, which McPhail described at J.P. Morgan as sitting at historical 3% lows for nearly four consecutive years, a level “never seen for this long” in HD’s operating history

- SRS Distribution delivers mid-single-digit organic sales growth in fiscal 2026 despite Q4 2025 roofing shipments running down 28% year-over-year, demonstrating the franchise can take share even in the weakest industry volume since 2019

- Mingledorff’s HVAC acquisition closes in Q2 and extends SRS cross-sell opportunities across roofing, wallboard, and HVAC in a $100 billion vertical previously outside HD’s total addressable market

- SIMPL Automation’s AI-driven distribution center technology improves pick speed and cycle times at scale, compressing same-day and next-day delivery costs as HD approaches 50% of stocked-product deliveries fulfilled at those speeds

What Could Go Wrong

- Housing affordability remains structurally impaired: 30-year mortgage rates near 6.3% and home prices still roughly 50% above 2019 levels suppress turnover well beyond current guidance assumptions, with existing home sales running at a 3.98 million seasonally adjusted annual rate in March

- The GMS acquisition continues to pressure gross margin through the first half of FY2026, with annualization adding an estimated 50 basis points of headwind in Q1 alone; any revenue shortfall amplifies that deleverage

- Q1 FY2026 EPS is guided mid-single-digit negative year-over-year entirely due to acquisition timing, and if the market reads that miss as demand deterioration rather than accounting mechanics, Home Depot stock faces a re-rating risk into the spring selling season

- Large discretionary DIY projects, specifically kitchen and flooring, remain stubbornly depressed with no confirming recovery signal as of the February earnings call, and big-ticket comp transactions of $1,000-plus have recovered only through maintenance and repair, not discretionary remodel

Should You Invest in The Home Depot, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up The Home Depot, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track The Home Depot, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze HD stock on TIKR for Free →