Key Stats for Western Digital Stock

- 52-Week Range: $44 to $484

- Current Price: $483

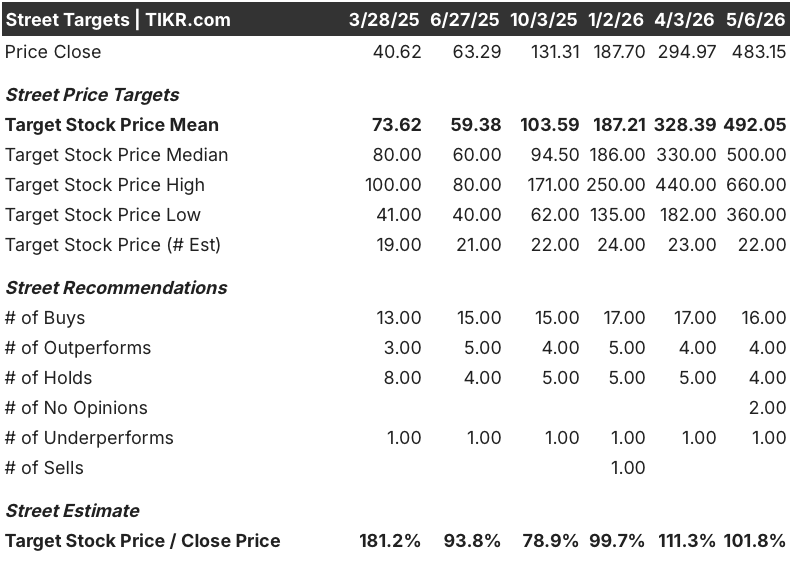

- Street Mean Target: $492

- Street High Target: $660

- Analyst Consensus: 16 Buys / 4 Outperforms / 4 Holds / 2 No Opinions / 1 Underperform

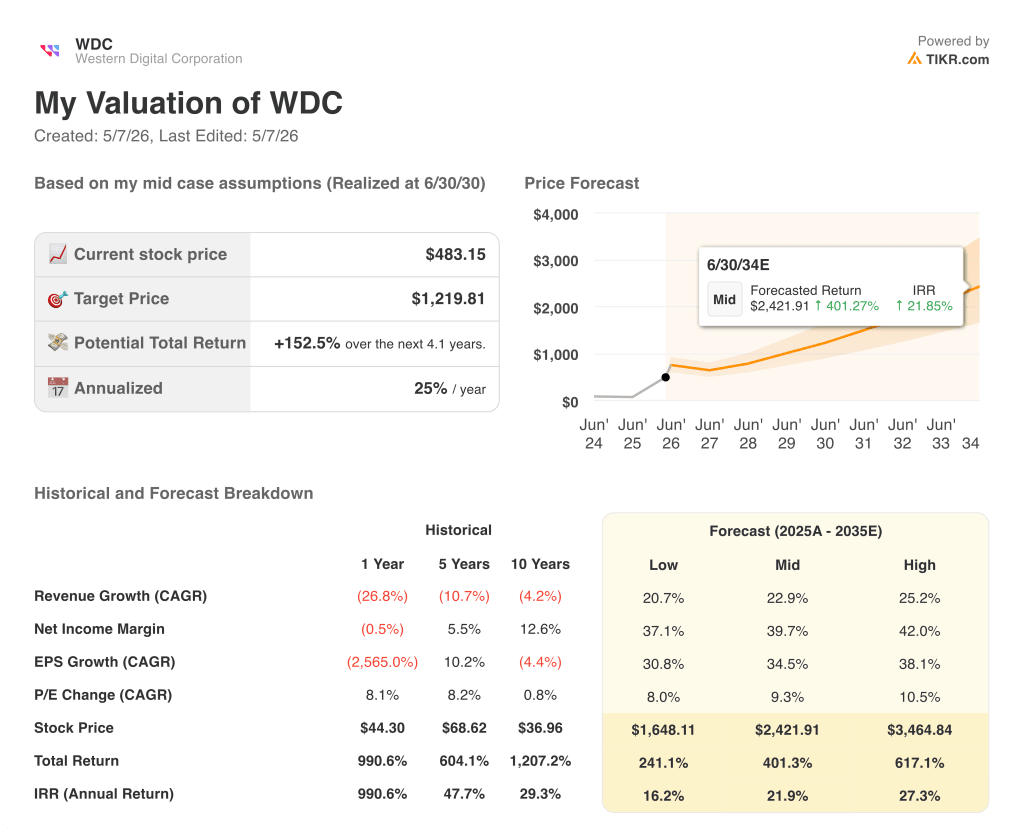

- TIKR Model Target (Dec. 2030): $1,220

What Happened?

Western Digital Corporation (WDC) makes hard disk drives (HDDs), the high-capacity magnetic storage devices that sit at the center of every major AI data center in the world.

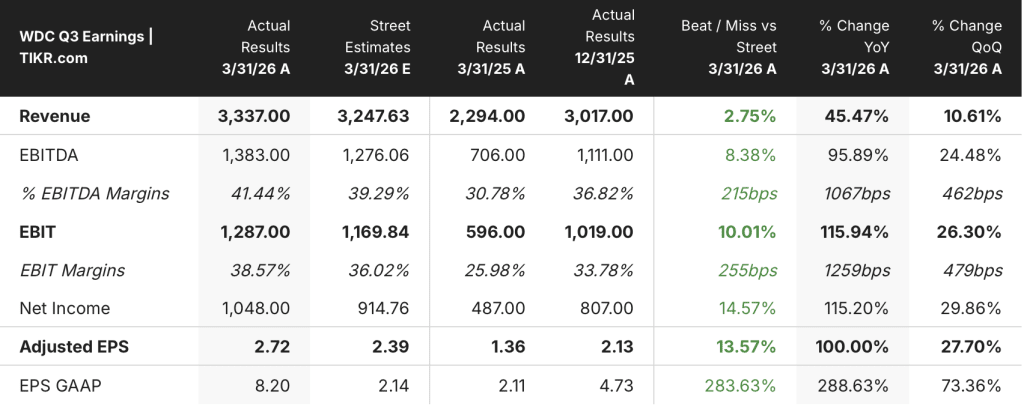

The company reported Q3 fiscal 2026 results on April 30, delivering $3.34 billion in revenue, a 45.5% jump year over year and a beat against the $3.25 billion consensus estimate.

Western Digital stock had already more than doubled year to date heading into the print, carried by the same AI infrastructure trade that lifted Seagate 150% and Sandisk over 360% in 2026.

Non-GAAP EPS came in at $2.72, up 97% versus the same quarter a year ago and ahead of the $2.39 analyst estimate.

Gross margin crossed 50% for the first time in the company’s recent history, landing at 50.5%, up 440 basis points sequentially.

The company guided Q4 revenue to $3.65 billion, roughly 40% growth year over year, ahead of the $3.46 billion Street estimate heading into the call.

Western Digital completed the spinoff of flash memory unit Sandisk in early 2025, allowing it to refocus entirely on HDDs and the hyperscaler data center market that now represents 89% of total revenue.

Cloud revenue reached $3 billion in Q3, up 48% year over year, driven by surging demand for high-capacity nearline drives from hyperscalers building AI inference and training infrastructure.

The company shipped 222 exabytes in the quarter, up 34% year over year, and reported a free cash flow figure of $978 million, representing a 29% free cash flow margin.

In February, Western Digital announced a new $4 billion share buyback authorization on top of a prior $2 billion program; the company raised its quarterly dividend 20% to $0.15 per share with this earnings release.

CEO Irving Tan framed the demand environment in structural terms on the Q1 2026 earnings call: “the AI-driven data economy is creating an unprecedented demand for high-capacity, reliable and high-performance storage on HDDs,” adding that the company now expects long-term data storage growth to exceed a 25% CAGR.

The company’s 40-terabyte next-generation ePMR drives are in qualification with three hyperscale customers, on track for volume production ramp in the second half of calendar 2026, and HAMR (heat-assisted magnetic recording) technology capable of eventually exceeding 100 terabytes per drive is in qualification with four customers ahead of a planned 2027 ramp.

Long-term customer agreements now extend into calendar 2028 and 2029, with major hyperscalers placing purchase orders 52 weeks in advance.

Track how analyst targets and consensus shift as WDC’s Q4 ramp plays out, on TIKR for free →

Wall Street’s Take on WDC Stock

WDC’s Q3 print didn’t just beat estimates; it resets the earnings trajectory for a company that was generating single-digit gross margins less than two years ago, and the forward estimates are only beginning to reflect what the hyperscaler demand cycle can do to a pure-play HDD business.

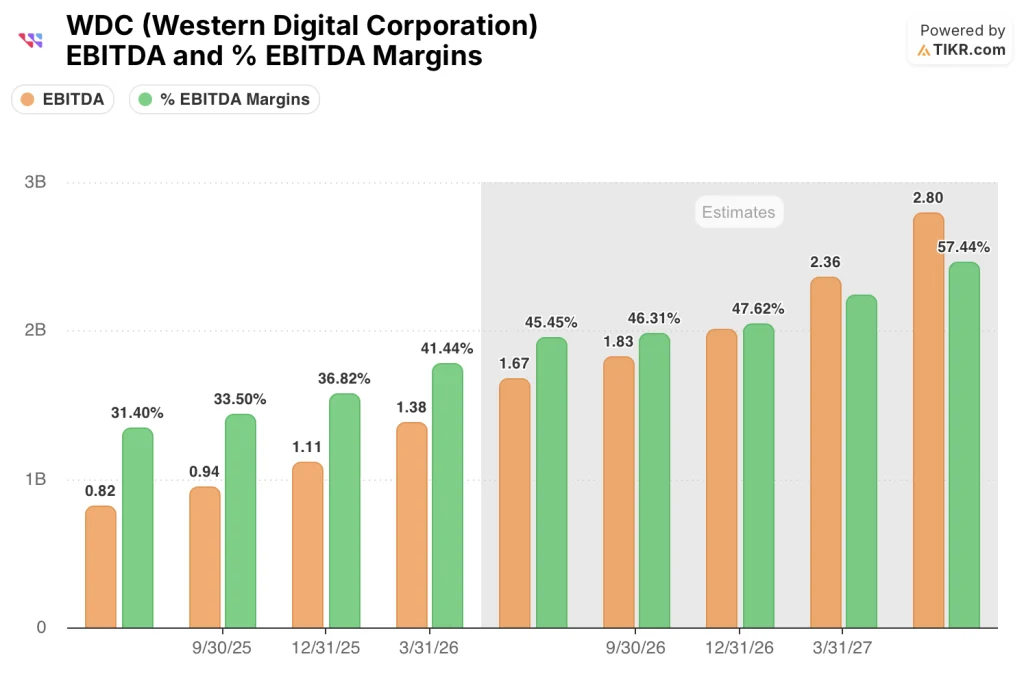

WDC’s EBITDA hit $1.38 billion in Q3, up 95.9% year over year, with EBITDA margins expanding to 41.4% from roughly 31% a year prior, and consensus models another 104% EBITDA growth for Q4 at around $1.67 billion, pointing to margins approaching 46%.

16 Buys / 4 Outperforms / 4 Holds / 2 No Opinions / 1 Underperform across 27 analysts, with a mean price target of around $492, implying roughly 2% upside from current levels, a spread that suggests the Street is running close to fair value while the business is still accelerating.

The street high target sits at $660, with the low at $360, a gap that will close based on one variable: whether 40-terabyte ePMR ramp execution and HAMR qualification timelines hold through the second half of calendar 2026.

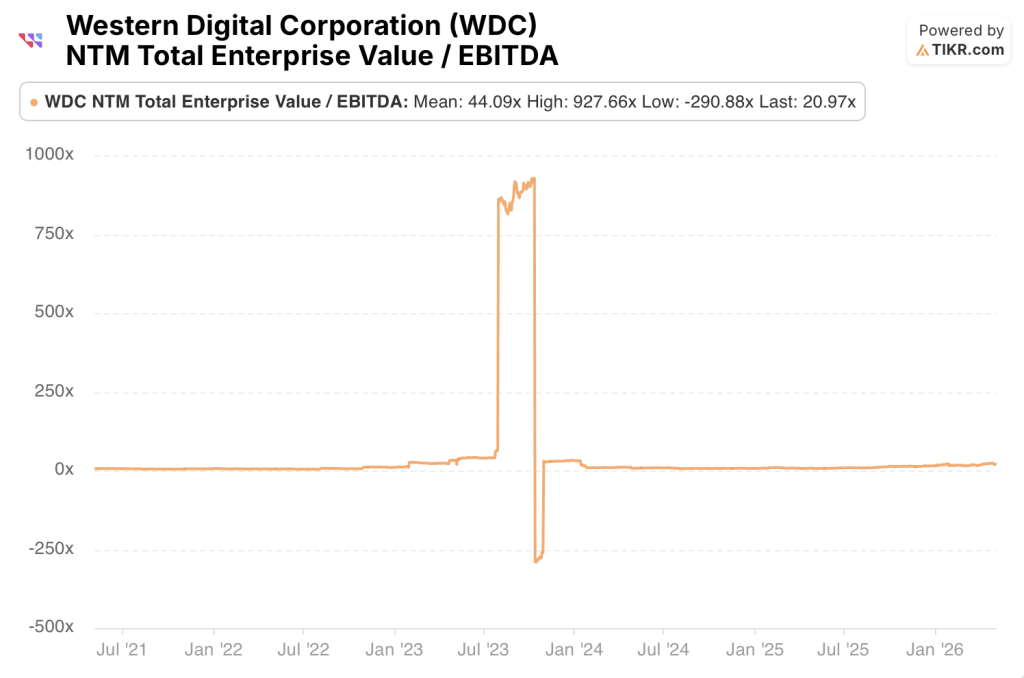

Trading at roughly 21x NTM EV/EBITDA against a 5-year historical mean of around 44x, Western Digital stock appears undervalued at a moment when EBITDA is growing over 95% year over year and consensus models another 104% growth in Q4, making the current multiple a significant discount to the stock’s own history at a far weaker point in the earnings cycle.

CFO Kris Sennesael flagged at the May 5 Barclays conference that exabyte CAGR expectations have moved from 25% to “maybe something trending that starts with a 3,” a demand revision that has not yet been absorbed into consensus price targets.

If the 40-terabyte ePMR ramp slips or HAMR qualification encounters yield issues, gross margin trajectory breaks, since both drives are central to the cost-per-terabyte declines that underpin the margin expansion story.

Q4 earnings and the first print containing 40-terabyte ePMR shipment data will be the first hard checkpoint for whether the $3.65 billion guide and 51% to 52% gross margin target track.

What Does the Valuation Model Say?

The TIKR model prices Western Digital stock at a mid-case target of around $1,220, reflecting a 23% revenue CAGR through 2035 and net income margins expanding to roughly 40%, an output that implies 152% total return from current levels at an annualized IRR of around 25%.

At $483, the market is pricing roughly 20 years of earnings power at today’s run rate, but the TIKR model’s low case, assuming around 21% revenue CAGR and 37% net income margins, still produces a price target of around $1,648 and an IRR of around 16%, meaning even a conservative read of the model leaves Western Digital stock significantly undervalued at current prices relative to a business that is compounding EBITDA at over 90% year over year with customer commitments stretching into 2029.

Bull Case

- 40-terabyte ePMR ramp on track for second half of calendar 2026, pushing average nearline capacity from 23 terabytes today toward 40 terabytes, a 75% exabyte capacity increase with no unit additions

- EBITDA margins reaching 46% in Q4 2026 and tracking toward the 50% range as ePMR cost-per-terabyte declines compound through fiscal 2027

- LTAs covering calendar 2028 and 2029 with major hyperscalers, combined with 52-week advance purchase orders, create earnings visibility unprecedented in the company’s history

- 20% dividend increase to $0.15 per quarter and $4 billion buyback program returning $2.2 billion to shareholders since Q4 fiscal 2025 demonstrate management confidence in cash generation durability

- UltraSMR adoption reaching 60% of exabyte shipments by end of fiscal 2027, compressing cost per terabyte and widening gross margin without incremental capital expenditure

Bear Case

- With a mean analyst target of $492 against a current price of $483, Western Digital stock offers almost no margin of safety at current Street consensus, meaning any execution stumble is priced with minimal buffer

- HAMR yield and reliability remain unresolved in qualification, and the company is 10 years into development; any slip to the 2027 ramp timeline removes a key long-term cost and capacity driver from the model

- Cost-per-terabyte declines running around 10% annually could compress if UltraSMR adoption stalls or the transition to 40-terabyte ePMR encounters qualification delays with the three hyperscale customers currently in testing

- WDC’s CEO and Chief of Global Operations sold a combined $10.2 million in shares in early May, a signal worth monitoring even if routine against a backdrop of a 150%-plus year-to-date gain

- The stock recently traded at 31x the next 12-month earnings versus 20x three months prior, a multiple expansion driven almost entirely by multiple re-rating rather than incremental estimate revisions, creating compression risk if growth momentum softens

Should You Invest in Western Digital Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Western Digital Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Western Digital Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze WDC stock on TIKR for Free →