Key Stats for Honeywell Stock

- Current Price: $217.03

- 52-Week Range: $186.76 to $248.18

- Street Mean Target: ~$248

- TIKR Model Target Price: ~$310

- Implied Upside (TIKR): ~48%

- Dividend Yield: 2.4%

Value your favorite stocks like HON with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

A Mixed Quarter, Soft Q2 Guidance, and a Confirmed Spin Date All in the Same Week

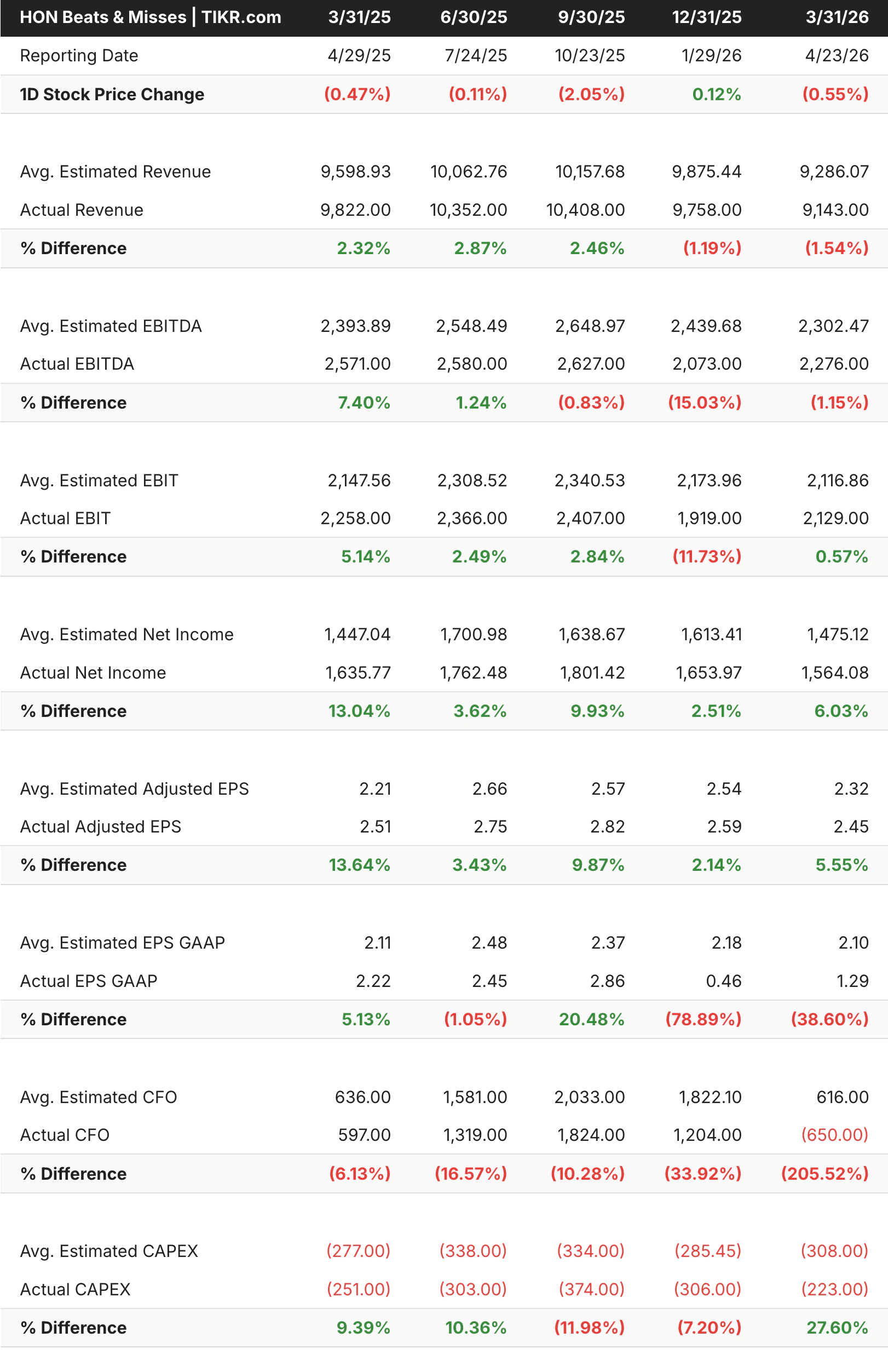

Honeywell (HON) reported Q1 2026 on April 23rd. Revenue of $9.14 billion came in about $140 million short of consensus, while adjusted EPS of $2.45 beat estimates of $2.32 by around 6%. The company delivered 11% adjusted earnings growth and 90 basis points of margin expansion, bringing the margin to over 23%.

The stock fell anyway, as Q2 guidance called for $2.35 to $2.45 in adjusted EPS against a Street consensus of $2.56, and revenue guidance of $9.4 to $9.6 billion, below the $9.7 billion expectation. Management cited temporary supply chain constraints in January and February, with March recovering to the strongest revenue month of the quarter.

Adjusted EPS has beaten estimates in all five of the quarters shown in the table, while revenue has missed in the two most recent periods. The stock’s muted reaction to earnings beats reflects a market focused almost entirely on what the two standalone businesses will look like after the separation.

The bigger news that week was the confirmation that the Aerospace Technologies spinoff closes June 29, with $20 billion in financing already raised.

See analysts’ growth forecasts and price targets for Honeywell stock (It’s free) >>>

Margins Have Drifted Lower, The Spin Is Designed to Fix That

Revenue has grown from $34.4 billion in 2021 to $37.4 billion in 2025, but operating margins have compressed from around 22% to roughly 19% over that same period. Gross margins have held in the 36-38% range.

The compression reflects the cost drag of managing a conglomerate through an active restructuring cycle. The Aerospace segment operates at 26.5% margins and has a $19 billion backlog that grew 20% year over year.

As a pure-play, it should command a meaningfully higher multiple than it receives today inside the blended structure. The remaining automation business, covering building, industrial, and process automation, will be leaner and more focused once the separation is complete, with stranded cost removal already accelerating ahead of the spin.

Value Honeywell instantly (Free with TIKR) >>>

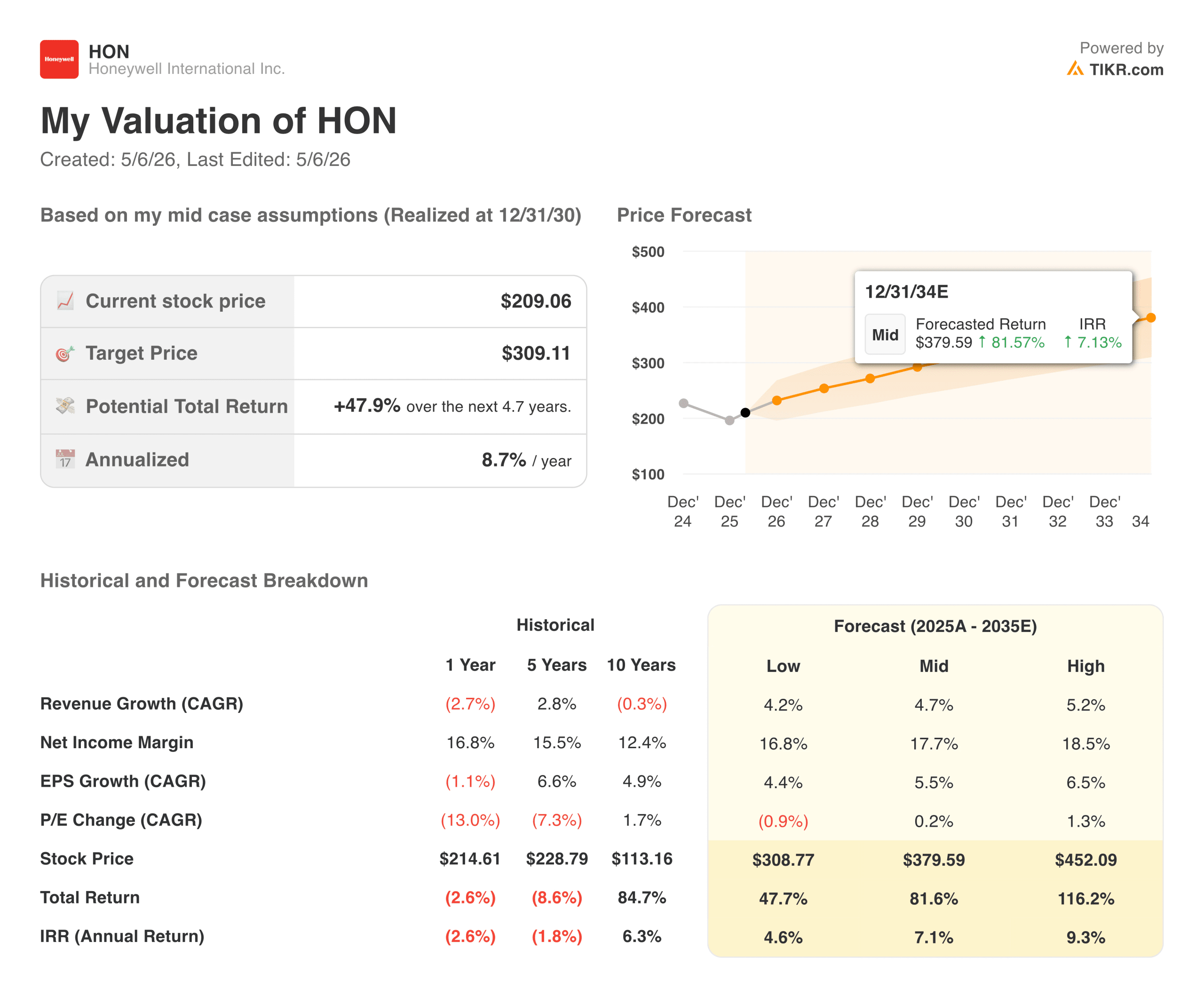

What a Fair Price for HON Looks Like Right Now

TIKR’s model targets around $310, implying a total return of roughly 48% over five years, or about 9% annualized.

Add the 2.4% dividend, and the total annual return in the mid-case lands near 11%. The assumptions are reasonable: revenue growing around 5% annually, margins expanding to roughly 18%, and EPS compounding near 6% per year with essentially flat multiple change.

What the Bulls Are Betting On:

- The Aerospace spin unlocks hidden value. A pure-play with a $19 billion backlog and 26.5% margins should trade at a premium multiple as a standalone, and investors buying HON today get that asset at the conglomerate discount.

- Two investor days before the close provide real clarity. Aerospace on June 2 and 3, Automation on June 11. Both are first looks at standalone economics and have historically been catalysts for re-rating.

- Supply chain constraints look temporary. March recovered strongly, full-year Aerospace guidance was maintained, and the backlog trajectory gives management real visibility.

What the Bears Are Watching:

- Q2 guidance was a meaningful miss. If constraints extend beyond Q1, full-year estimates come under pressure before the spin even closes.

- The post-spin automation business is unproven as a standalone. Investors who owned HON for aerospace exposure will need to make a fresh decision, which creates near-term selling pressure.

- Margin recovery in automation is not guaranteed. Stranded cost removal helps, but the pace and magnitude remain uncertain until the new structure is up and running.

Should You Invest in Honeywell?

Honeywell is almost finished becoming something different from what it was two years ago. The separation closes in six weeks; investor days follow shortly after, and the stock is trading 13% below its 52-week high, with the most important catalysts still ahead.

At around 20 times forward earnings with a 2.4% dividend and a TIKR model pointing toward $310 at roughly 9% annualized, the valuation does not require perfection.

The June investor days will be the real test, giving investors their first clean look at what each business is actually worth on a standalone basis.

See analysts’ growth forecasts and price targets for Honeywell stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!