Key Takeaways:

- Thermo Fisher Scientific (TMO) beat Q1 2026 adjusted EPS estimates, delivering $5.44 versus a consensus of around $5.24, and revenue grew 6% to $11.0 billion on the back of the Clario acquisition.

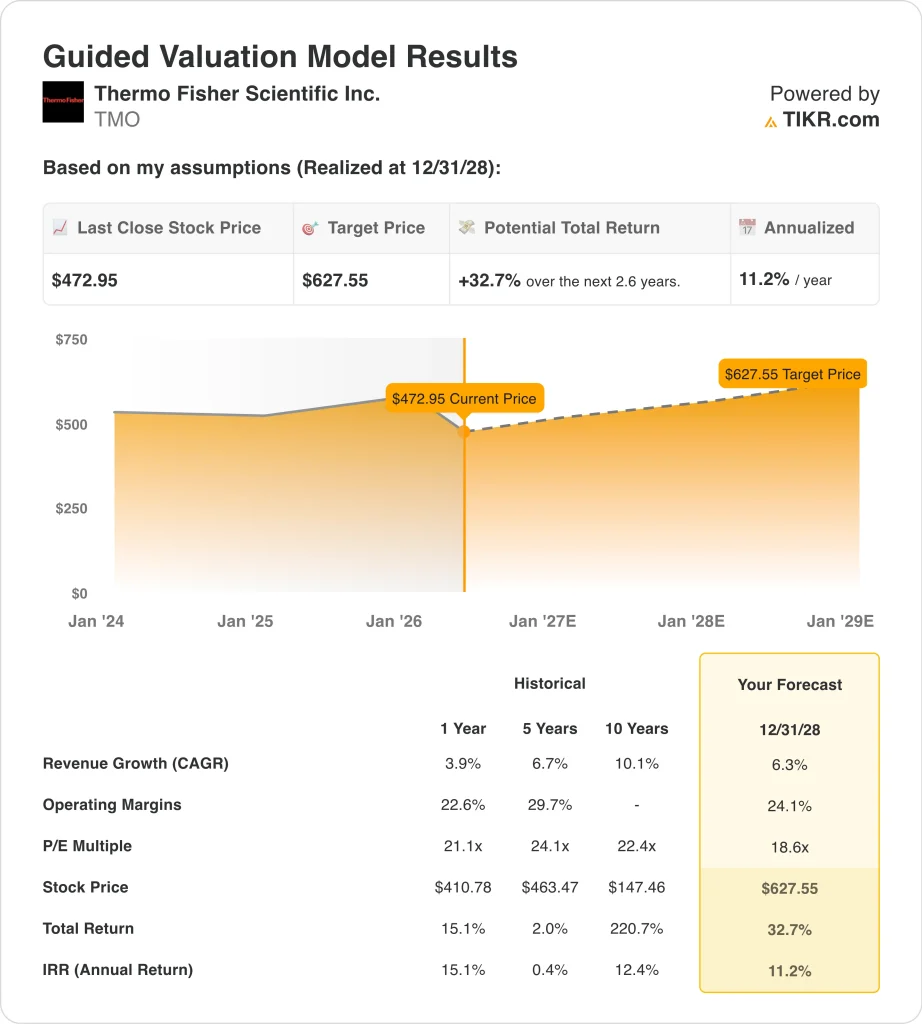

- TMO stock trades near $473, down around 20% year to date and well below its 52-week high of $644.

- TMO could rise from $473 to around $628 per share by December 2028, based on 6.3% revenue growth, 24.1% operating margins, and an 18.6x P/E multiple.

- That implies a 32.7% total return, or around 11.2% annualized over the next 2.6 years, making it an attractive setup by the model’s criteria.

What Happened?

Thermo Fisher Scientific (TMO) beat Q1 2026 earnings expectations but flagged meaningful near-term headwinds that kept the market cautious. Revenue grew 6% to $11.0 billion, supported in part by the acquisition of Clario Holdings, a clinical trial software company acquired for approximately $10 billion in late 2025.

Thermo Fisher Scientific is the world’s largest life sciences tool and equipment company. It manufactures scientific instruments, laboratory consumables, and specialty chemicals used in drug discovery, clinical testing, genomics, and bioproduction.

The company serves pharmaceutical and biotech companies, hospitals, academic research institutions, and government agencies. Its CDMO (contract development and manufacturing organization) business helps drug companies manufacture therapies at a commercial scale.

In July 2025, Thermo Fisher expanded its strategic partnership with Sanofi to support additional U.S. drug product manufacturing, reflecting the durability of large pharma outsourcing relationships. And in April 2026, the company agreed to sell its microbiology business to private equity firm Astorg for around $1.075 billion, sharpening its focus on higher-growth segments.

The consensus analyst target for TMO sits at around $620, implying around 31% upside from the current price. And the company has beaten adjusted EPS estimates in multiple consecutive quarters, suggesting the business is executing well against its own internal targets.

Management’s ability to consistently deliver against estimates while actively reshaping the portfolio gives investors reason to believe the current selloff is an overreaction to manageable near-term challenges rather than a structural deterioration of the business.

Here’s why Thermo Fisher stock could recover meaningfully as biopharma investment rebounds and clinical services from the Clario acquisition begin contributing at scale.

What the Model Says for TMO Stock

We analyzed the upside potential for Thermo Fisher stock using valuation assumptions based on its biopharma services growth, CDMO revenue expansion, and a recovery in academic and life sciences research spending across its instrument and consumables businesses.

Based on estimates of 6.3% annual revenue growth, 24.1% operating margins, and a normalized P/E multiple of 18.6x, the model projects Thermo Fisher stock could rise from $473 to around $628 per share.

That would be a 32.7% total return, or an 11.2% annualized return over the next 2.6 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for TMO stock:

1. Revenue Growth: 6.3%

Thermo Fisher grew revenue 6% in Q1 2026, with the Clario acquisition contributing meaningfully to the result. The company’s 10-year revenue CAGR stands at around 10.1%, and the 2-year forward consensus CAGR is around 6.4%. Core organic growth is expected to reaccelerate as biopharma capital spending normalizes following a post-COVID correction period.

Based on analysts’ consensus estimates, we used 6.3% revenue growth, reflecting Thermo Fisher’s steady reacceleration as biopharma investment recovers and newly acquired Clario assets begin contributing incremental revenue to the base.

2. Operating Margins: 24.1%

Thermo Fisher’s LTM EBIT margin stands near 18.8%, but the 5-year average is around 29.7%, reflecting the post-COVID margin correction in its biopharma services segment. The company is rebuilding margins through cost discipline and operating leverage in its laboratory products and biopharma services businesses. Clario adds software-driven clinical analytics that carry structurally higher margins than legacy hardware.

Based on analysts’ consensus estimates, we used 24.1% operating margins, reflecting Thermo Fisher’s path toward margin recovery as revenue growth accelerates and higher-margin services represent a larger portion of the mix.

3. Exit P/E Multiple: 18.6x

Thermo Fisher’s NTM P/E sits at around 18.6x, which reflects a meaningful derating from its 5-year average near 24x. The lower multiple captures both the post-COVID revenue reset and near-term uncertainty around academic spending and inflation risks. But the company has maintained consistent earnings beats even through this challenging period.

Based on analysts’ consensus estimates, we use 18.6x as the exit multiple, reflecting a market that has repriced TMO conservatively and where valuation re-expansion is plausible if biopharma demand normalizes and margin recovery continues.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for TMO stock through 2034 show varied outcomes based on biopharma spending trends, CDMO growth, and operating margin recovery (these are estimates, not guaranteed returns):

- Low Case: Academic demand stays weak, and biopharma capital spending recovers only slowly → around 4.7% annual returns

- Mid Case: Biopharma investment recovers, Clario integration delivers synergies, and margins rebuild → around 7.4% annual returns

- High Case: CDMO volumes accelerate, academic demand rebounds sharply, and margins recover faster → around 9.9% annual returns

Going forward, TMO stock carries a near-term model return of around 11.2% annually, which suggests the stock may be attractively priced at current levels relative to its long-term earnings power. The 20% year-to-date decline has created a meaningful discount to the analyst consensus target of around $620, and management has consistently delivered quarterly earnings beats even through the post-COVID correction.

Investors should monitor the pace of biopharma capital spending recovery and the Clario acquisition ramp as the two most important catalysts for validating whether the near-term model assumptions hold.

See what analysts think about TMO stock right now (Free with TIKR) >>>

Should You Invest in Thermo Fisher?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up TMO, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track TMO alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Thermo Fisher stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!