Key Takeaways:

- Robinhood (HOOD) reported Q1 2026 revenue of $1.07 billion, up 15% year-over-year, but missed analyst estimates as crypto trading volumes declined. HOOD stock trades near $79, down around 30% year to date and well below its 52-week high of $154.

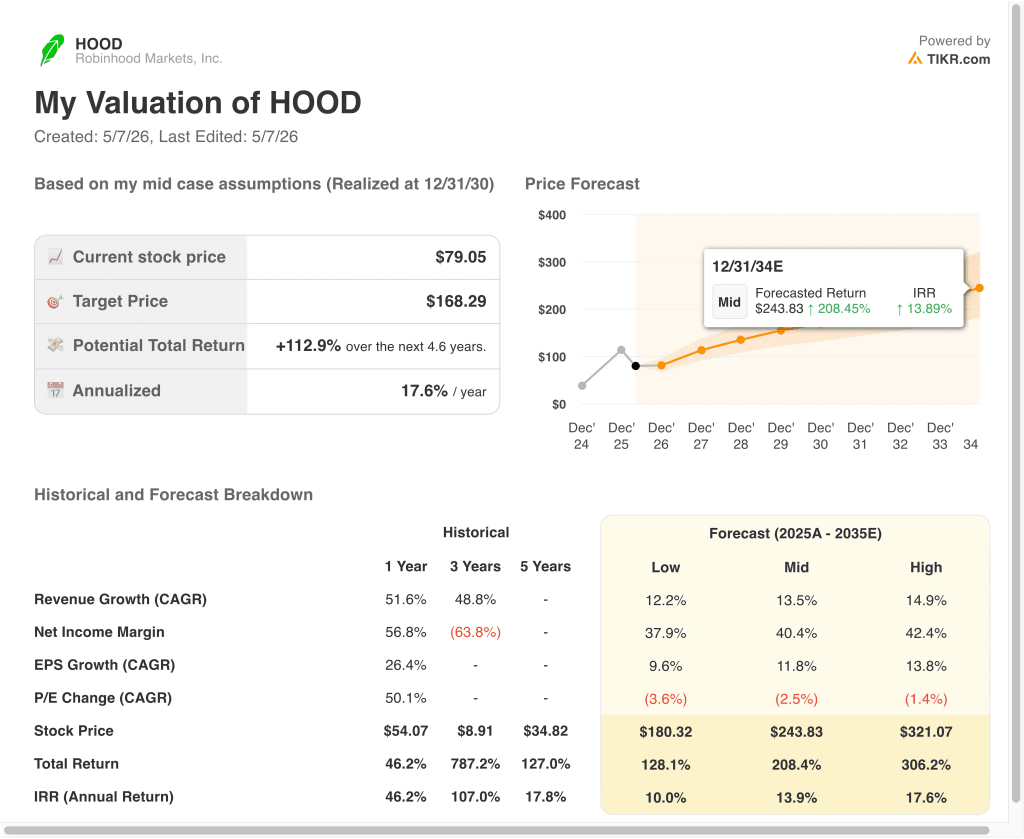

- HOOD stock could rise from $79 to around $125 per share by December 2028, based on 15% revenue growth, 46% operating margins, and a 34.0x P/E multiple.

- That implies a 58.7% total return, or around 19% annualized over the next 2.6 years.

What Happened?

Robinhood Markets (HOOD) reported Q1 2026 results that fell short of expectations, and shares declined in response. Revenue reached $1.07 billion, up 15% year-over-year, but it missed the analyst consensus of $1.14 billion.

Net income rose 3% to $346 million, and diluted EPS of $0.38 also missed estimates of $0.39. Transaction-based revenues softened because crypto trading activity slowed from its late 2025 peak. So investors who had priced in continued trading momentum felt the disappointment.

Robinhood is a digital financial services platform that allows users to trade stocks, ETFs (exchange-traded funds), options, gold, and cryptocurrencies at zero commission. The company also offers Robinhood Gold, a paid subscription service with premium features like margin investing and higher savings rates.

Beyond trading, Robinhood continues expanding into banking and international markets. In April 2026, Singapore regulators gave in-principle approval for Robinhood to launch brokerage services there, adding a meaningful new growth avenue. But near-term sentiment stays cautious because transaction revenues are volatile and closely tied to market activity.

The stock’s 52-week high of $154 shows how quickly sentiment can shift in Robinhood’s favor when trading volumes spike. And while the near-term miss was real, the platform continues to grow its Gold subscriber base, net interest income, and international footprint across multiple quarters.

Here’s why Robinhood stock could deliver strong multi-year returns as it builds a full-service financial platform and diversifies revenue beyond volatile crypto trading.

What the Model Says for HOOD Stock

We analyzed the upside potential for Robinhood stock using valuation assumptions based on its expanding Gold subscription business, international brokerage expansion into Singapore, and continued trading volume growth across equities, options, and crypto.

Based on estimates of 15% annual revenue growth, 46% operating margins, and a normalized P/E multiple of 34.0x, the model projects Robinhood stock could rise from $79 to around $125 per share.

That would be a 58.7% total return, or a 19% annualized return over the next 2.6 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for HOOD stock:

1. Revenue Growth: 15%

Robinhood delivered 15% year-over-year revenue growth in Q1 2026. Transaction revenues, Gold subscriptions, and net interest income all contributed to that result.

The company’s 3-year revenue CAGR (compound annual growth rate) stands at around 49%, so 15% reflects a meaningful step-down from recent hypergrowth. But it also accounts for the normalization of crypto and options volumes over time.

Based on analysts’ consensus estimates, we used 15% as our forward growth rate, reflecting Robinhood’s ability to sustain double-digit expansion through subscriptions, banking products, and international market entry.

2. Operating Margins: 46%

Robinhood’s LTM (last twelve months) operating margin stands near 46%. The company runs a highly scalable digital platform with minimal physical infrastructure. Its gross margin exceeds 80%, which creates strong leverage as the revenue base grows. And R&D (research and development) investment runs at around 22% of revenue, supporting product expansion.

Based on analysts’ consensus estimates, we used 46% operating margins, reflecting Robinhood’s capital-light structure and its ability to expand profitability as its subscriber base and product suite scale over time.

3. Exit P/E Multiple: 34x

Robinhood’s LTM P/E ratio stands near 38x, and the NTM (next twelve months) P/E sits at around 35x. The model applies a modest contraction, bringing the exit multiple to 34.0x by December 2028. This reflects the expectation that growth rates will moderate as the company matures and scales.

Based on analysts’ consensus estimates, we use 34.0x as our exit multiple, balancing Robinhood’s durable competitive moat in retail investing with the reality that premium multiples tend to compress over time.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for HOOD stock through 2034 show varied outcomes based on trading volume recovery, subscription growth, and international expansion (these are estimates, not guaranteed returns):

- Low Case: Crypto trading stays sluggish, and international launches generate modest contribution → around 10% annual returns

- Mid Case: Gold subscriptions grow steadily, Singapore gains traction, and trading volumes normalize → around 14% annual returns

- High Case: Crypto surges again, banking accelerates, and international markets compound growth → around 18% annual returns

Going forward, HOOD stock’s trajectory depends on whether crypto and options trading volumes recover in a meaningful way, but the platform’s expanding product suite and global ambitions create a credible long-term story.

The near-term model projects around 19% annualized returns if the growth assumptions hold, which qualifies it as a potentially compelling setup for patient investors. Yet the inherent cyclicality of transaction-based income means near-term results will likely stay volatile, and investors should weigh that risk carefully against the multi-year upside.

See what analysts think about HOOD stock right now (Free with TIKR) >>>

Should You Invest in Robinhood?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up HOOD, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track HOOD alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Robinhood stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!