Key Takeaways:

- Cummins (CMI) reported Q1 2026 sales of $8.4 billion, beating analyst estimates, but net income fell 21% to $654 million. Management raised its full-year 2026 revenue guidance on robust power generation demand.

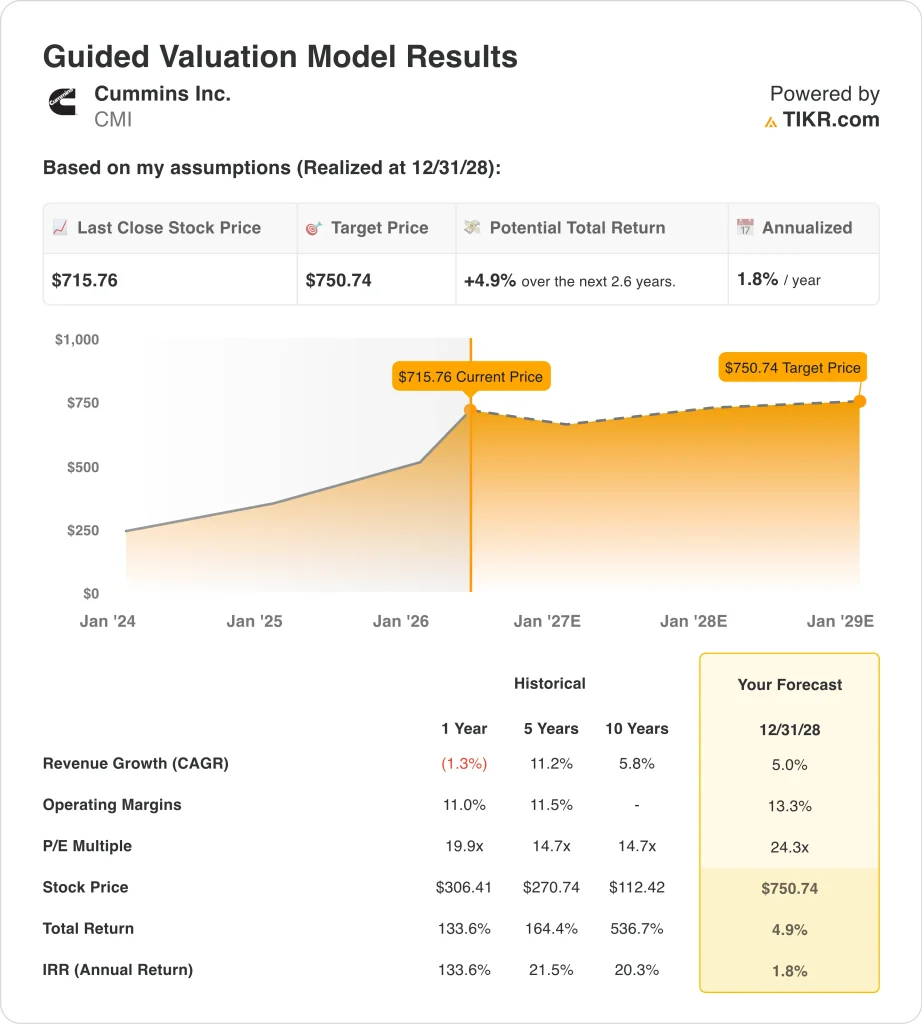

- CMI stock trades near $716, up around 144% over the past year and near its 52-week high of $717.

- CMI could rise from $716 to around $751 per share by December 2028, based on 5% revenue growth, 13.3% operating margins, and a 24.3x P/E multiple.

- That implies a modest 4.9% total return, or around 1.8% annualized over the next 2.6 years, suggesting limited near-term upside at the current price.

What Happened?

Cummins Inc. (CMI) delivered solid Q1 2026 results and raised its full-year guidance, but the stock is already reflecting a lot of optimism after a remarkable run. Revenue rose 3% to $8.4 billion, beating analyst estimates of around $8.35 billion.

But net income fell 21% to $654 million, as higher costs and investments weighed on profitability. Management raised its 2026 revenue outlook because power generation demand, which includes backup power systems and data center energy infrastructure, remains strong. So brokerages quickly lifted their price targets following the earnings report.

Cummins is a global manufacturer of diesel and natural gas engines, power systems, filtration products, and related components. The company serves a wide range of industries, including trucking, construction, mining, and power generation. Its Accelera division focuses on battery-electric and hydrogen-based powertrains for commercial vehicles.

In April 2026, Cummins sold its hydrogen fuel cell activities dedicated to rail to Alstom, sharpening its strategic focus on core markets. And in 2025, the company also completed a $4.1 billion acquisition of Solventum‘s purification and filtration business, while selling other non-core assets to streamline its portfolio.

The stock has been one of the best performers in the industrial sector over the past year, gaining around 144% and approaching its 52-week high. Much of this rally reflects investor excitement about power generation tailwinds tied to rising data center electricity demand and energy infrastructure spending.

However, the consensus analyst target price of around $693 now sits below the current stock price of $716, signaling that most near-term upside may already be reflected in the share price. Investors are therefore rethinking how much further the rally can reasonably extend on current estimates.

Here’s why Cummins stock could still deliver meaningful long-term returns as power generation infrastructure investment compounds across data centers and commercial energy systems.

What the Model Says for CMI Stock

We analyzed the upside potential for Cummins stock using valuation assumptions based on its power generation revenue growth, gradual margin recovery, and stable engine volumes across diversified industrial end markets.

Based on estimates of 5% annual revenue growth, 13.3% operating margins, and a normalized P/E multiple of 24.3x, the model projects Cummins stock could rise from $716 to around $751 per share.

That would be a 4.9% total return, or a 1.8% annualized return over the next 2.6 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for CMI stock:

1. Revenue Growth: 5%

Cummins grew revenue 3% year-over-year in Q1 2026 and raised its full-year guidance on power generation strength. The company’s 10-year revenue CAGR stands at 5.8%, so a 5% forward rate aligns well with its long-term historical profile.

Power generation tailwinds are offset by ongoing cyclical softness in commercial truck engine demand and the reshaping of its clean energy activities.

Based on analysts’ consensus estimates, we used 5% annual revenue growth, reflecting Cummins’ steady industrial exposure and strong power generation momentum balanced against near-term headwinds in legacy diesel truck markets.

2. Operating Margins: 13.3%

Cummins reported an LTM EBIT (earnings before interest and taxes) margin of around 11.5%. The company’s Accelera clean energy unit has weighed on overall margins as it scales.

But management expects profitability to improve as restructuring efforts take hold and high-margin power generation revenue grows as a share of the total mix.

Based on analysts’ consensus estimates, we used 13.3% operating margins, reflecting Cummins’ ability to expand profitability as power generation offsets ongoing investment in alternative drivetrain technologies over the forecast horizon.

3. Exit P/E Multiple: 24.3x

Cummins currently trades at an NTM P/E (next twelve months price-to-earnings ratio) of around 24x, broadly consistent with our 24.3x exit assumption. Historically, the stock has traded at lower multiples, but power generation growth has expanded investor expectations significantly.

Based on analysts’ consensus estimates, we use 24.3x as our exit multiple, consistent with current market pricing and reflecting steady but moderate long-term earnings growth.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for CMI stock through 2034 show varied outcomes based on power generation demand, margin recovery, and clean energy adoption (these are estimates, not guaranteed returns):

- Low Case: Power generation growth stalls, and margins stay compressed from clean energy investment → around 0.7% annual returns

- Mid Case: Power generation scales steadily, margins expand, and Accelera gains commercial traction → around 9.6% annual returns

- High Case: Data center demand accelerates, and alternative powertrains gain meaningful momentum → around 6.0% annual returns

Going forward, CMI stock presents a nuanced setup where near-term upside looks limited at current levels, but the longer-term model shows a more compelling case as power generation infrastructure investment compounds.

The near-term annualized return of around 1.8% suggests the stock may be fully priced today, and the near-term model return below 5% reinforces that view. Investors with a multi-year horizon should watch whether power generation demand sustains itself and whether margin expansion materializes as Cummins restructures its portfolio.

See what analysts think about CMI stock right now (Free with TIKR) >>>

Should You Invest in Cummins?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CMI, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track CMI alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Cummins stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!