Key Takeaways:

- Baker Hughes Company (BKR) is a global provider of oilfield products, services, and industrial technology, including a rapidly growing data center power segment.

- BKR reported Q1 2026 adjusted EPS of $0.58, beating the consensus estimate of $0.49, and issued full-year revenue guidance of $26.2 billion to $28.3 billion.

- The model projects BKR stock could rise from $67 to around $88 per share by December 2028, implying a 32.1% total return.

- That works out to around 11% in annualized returns over the next 2.6 years, a level that historically indicates an attractive opportunity.

What Happened?

Baker Hughes Company (BKR) has been one of the strongest-performing energy stocks of 2026. The stock is up around 42% year to date, reaching its 52-week high of $70.41. Q1 2026 adjusted EPS of $0.58 beat the consensus estimate of $0.49. But beyond earnings, the company’s technology pivot is generating significant investor attention.

Baker Hughes is winning major orders for gas turbines and power systems to support AI data centers. The company secured a 1.21 gigawatt generator order to power a Boom Supersonic AI data center solution in February 2026.

Multiple other gas turbine orders followed throughout early 2026. Management is confident in achieving $1.5 billion of data center orders ahead of its original three-year timeline.

On the portfolio side, Baker Hughes agreed to sell Waygate Technologies to Hexagon for around $1.45 billion in April 2026. This divestiture simplifies the business and improves capital allocation flexibility.

The company also opened a new subsea manufacturing facility in Norway and paid its regular quarterly dividend of $0.23 per share. The Iran conflict is also supporting oil exploration spending, providing a near-term tailwind for the core oilfield services business.

Investors are balancing the exciting technology pivot story against the modest overall revenue growth outlook. The core oilfield services market remains cyclical and dependent on oil prices. But the data center and energy transition businesses add a durable secular growth layer. Here’s why Baker Hughes stock could offer a compelling risk-adjusted return for investors through 2028.

What the Model Says for BKR Stock

We analyzed the upside potential for Baker Hughes stock based on its industrial and energy technology momentum, growing data center order pipeline, and improving operating margins from portfolio simplification.

Based on estimates of 3.0% annual revenue growth, 14.5% operating margins, and a normalized P/E multiple of 28.4x, the model projects Baker Hughes stock could rise from $67 to around $88 per share.

That would be a 32.1% total return, or a 11.0% annualized return over the next 2.6 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for BKR stock:

1. Revenue Growth: 3%

Baker Hughes issued full-year 2026 revenue guidance of $26.2 billion to $28.3 billion. Q1 2026 adjusted EPS of $0.58 exceeded the $0.49 estimate, and Q4 2025 adjusted EPS of $0.78 beat the $0.67 estimate. These consistent beats reflect solid operational execution across the business segments.

The company is pivoting quickly toward higher-growth industrial technology markets. Baker Hughes is confident in achieving $1.5 billion in data center-related orders ahead of its original timeline. These orders represent an important secular tailwind that adds diversification beyond the more cyclical oilfield services business.

Based on analysts’ consensus estimates, we used a 3.0% annual revenue growth rate. The forward two-year consensus revenue CAGR stands at approximately 2.1%, so our assumption is modestly above consensus. It reflects the potential upside from data center order momentum and a supportive oil exploration spending environment.

2. Operating Margins: 14.5%

Baker Hughes carries an LTM EBIT margin of 12.8% and a gross margin of 23.6%. The industrial and energy technology segments generally carry higher margins than the core oilfield services business. The ongoing portfolio simplification, including the Waygate Technologies divestiture, should modestly improve the overall margin profile.

The company maintains an extremely clean balance sheet with net debt of just $230 million and a net debt to EBITDA ratio of only 0.04x. This financial flexibility allows Baker Hughes to invest in growth, return capital through dividends, and pursue acquisitions without constraint. The quarterly dividend of $0.23 per share and 1.4% yield add to the total return picture.

Based on analysts’ consensus estimates, we used 14.5% operating margins. This reflects a meaningful step up from the current 12.8% EBIT margin, driven by technology mix improvement and operating leverage. It is consistent with management’s stated goal of improving profitability as the technology portfolio grows.

3. Exit P/E Multiple: 28.4x

Baker Hughes currently trades at a forward NTM P/E of 28.36x. This is a premium multiple for an oilfield services company, but it reflects the market’s willingness to pay for the technology pivot story. The data center power opportunity and energy transition tailwinds add a growth premium that justifies a higher multiple than traditional oilfield services peers.

The analyst’s target of $70.24 sits just around 5% above the current price of $67. This narrow gap suggests analysts are cautious about near-term upside at current valuation levels. But the guided valuation model shows a more meaningful opportunity over a longer two to three-year horizon.

Based on analysts’ consensus estimates, we used a 28.4x exit P/E multiple. This is in line with the current trading multiple and assumes the technology differentiation story continues to command a premium. A reversion toward traditional energy services multiples would reduce the projected return significantly.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

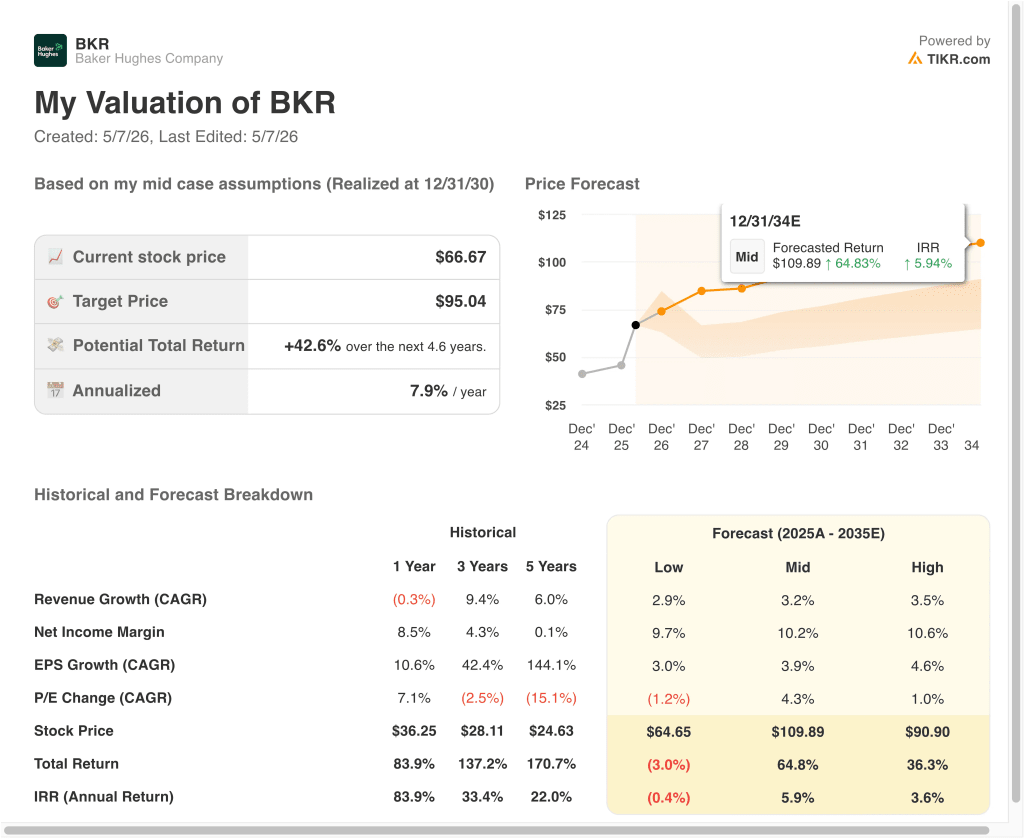

Different scenarios for BKR stock through 2034 show varied outcomes based on data center order execution, energy technology demand, and oil exploration spending trends (these are estimates, not guaranteed returns):

- Low Case: Oil and gas spending disappoints, and data center orders fall short of targets → around 0.4% negative annual returns

- Mid Case: Energy technology and data center momentum delivers steady progress → around 6% annual returns

- High Case: Technology pivot succeeds, but growth execution trails the mid case path → around 4% annual returns

Going forward, Baker Hughes’ stock will move based on the pace of its industrial technology transformation and the trajectory of global energy investment. The near-term guided valuation model is more optimistic than the longer-term advanced scenarios, suggesting the 2028 window may represent the better return opportunity.

Investors who believe in the secular data center and energy transition themes may find the near-term risk-reward more compelling than the headline long-term numbers suggest.

See what analysts think about BKR stock right now (Free with TIKR) >>>

Should You Invest in Baker Hughes?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up BKR, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track BKR alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Baker Hughes stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!