Key Takeaways:

- SanDisk (SNDK) is a pure-play NAND flash memory company recently spun off from Western Digital, while Micron (MU) covers DRAM, NAND, and HBM memory, and both are capitalizing on surging AI data center demand.

- Analysts expect both companies to see strong continued growth, with Micron generating $37.4B in annual revenue at 26.2% operating margins alongside $1.7B in free cash flow, while Sandisk’s quarterly revenue surged 97% year over year, though annual free cash flow remains negative at $120MM.

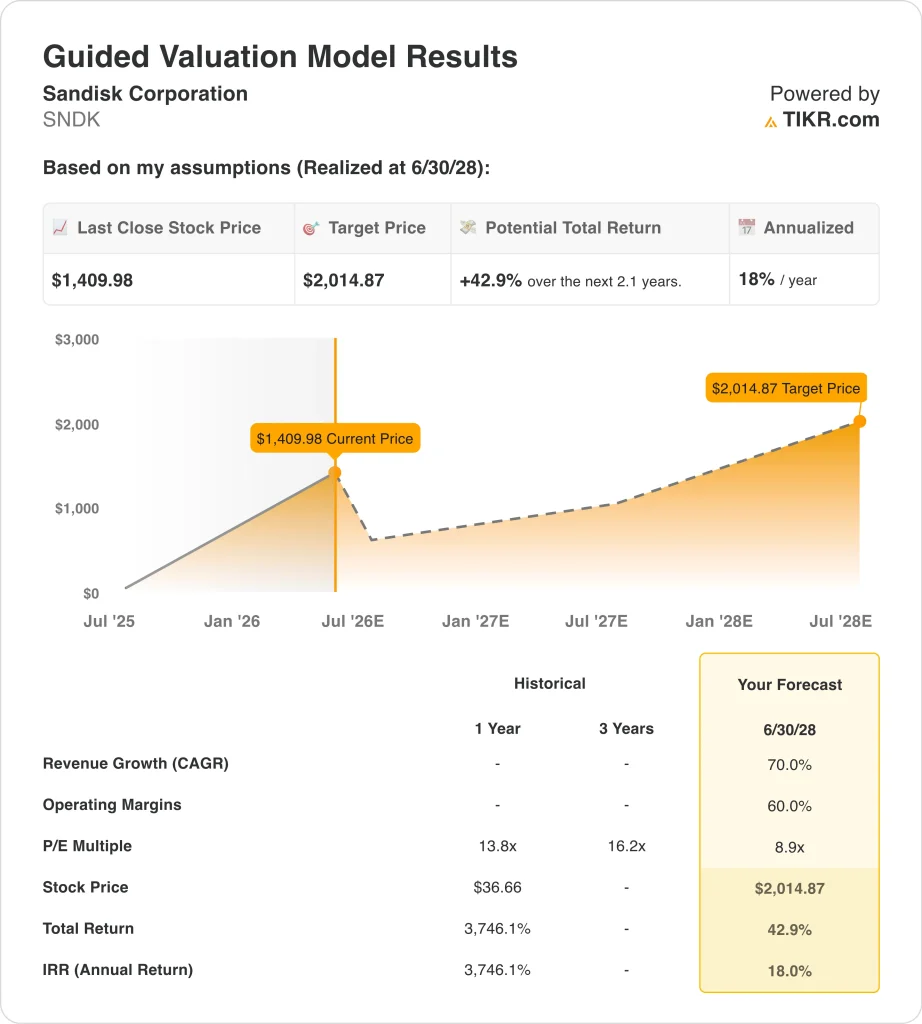

- Based on our valuation assumptions, MU stock could rise from around $667 to around $727 per share by August 2028, a roughly 9% total return or around 3.8% annualized, while SNDK could rise from around $1,410 to around $2,015, a roughly 43% total return or around 18% annualized.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

What’s Happening?

Memory and storage stocks have staged one of the most dramatic recoveries in recent semiconductor history. AI infrastructure spending is surging, and so is demand for chips that store and process massive amounts of data.

Both Micron Technology and Sandisk Corporation are direct beneficiaries of this trend. Micron has gained around 730% in the past year, while Sandisk has surged over 4,000% since its February 2025 spinoff.

Micron Technology (MU) manufactures and markets semiconductor solutions worldwide. The company produces DRAM, the fast temporary memory inside servers and AI systems, plus NAND flash and HBM. HBM stands for High Bandwidth Memory, and it is the fastest memory type packed inside modern AI processors. Micron posted Q2 fiscal 2026 adjusted earnings per share of $12.20, beating the analyst estimate of $9.21 by over 32%.

Sandisk (SNDK) produces NAND flash memory, a type of storage chip that retains data even without power. The company spun off from Western Digital in February 2025 and joined the Nasdaq 100 in April 2026.

Last quarter, Sandisk reported $5.95B in revenue, up 97% year over year, and net income up 350% to $3.62B. Both companies are riding the same AI wave, but their financials and valuations diverge sharply.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Micron Leads on Margins, But Sandisk Is Turning the Corner

Micron’s revenue recovery has been one of the strongest in the semiconductor space. Revenue dropped from $30.8B in fiscal 2022 to just $15.5B in fiscal 2023, but it bounced back to $37.4B in the most recent period.

That represents nearly a 50% jump in one year, driven by AI data center demand for DRAM and HBM. Sandisk’s revenue recovery has been smaller, rising from $6.7B in fiscal 2024 to $7.4B in fiscal 2025.

Micron’s operating margins have swung dramatically over the past three years. The company posted 31.6% in fiscal 2022, fell into the red in 2023, and recovered to 26.2% most recently. Volatility like this is common in memory chip businesses, since prices move sharply with supply and demand cycles. Sandisk improved its operating margin from negative 7.2% in fiscal 2024 to 6.9% in fiscal 2025.

Free cash flow tells a similar recovery story for Micron. After burning $6.1B in fiscal 2023, the company generated $121MM in fiscal 2024 and $1.7B in the latest period.

That trajectory is encouraging, but free cash flow remains modest relative to $37.4B in revenue. Sandisk still burns cash, but improved from negative $475MM in fiscal 2024 to negative $120MM in fiscal 2025.

Micron leads on profitability overall, with a 58.4% gross margin versus Sandisk’s 56% and much stronger operating margins. But Sandisk is catching up quickly, and its most recent quarterly results show an accelerating turn toward profitability.

Investors who prioritize current margins and free cash flow will favor Micron. Those who are betting on margin expansion and faster growth may find Sandisk the more interesting story.

See what analysts think about SNDK and MU stock right now (Free with TIKR) >>>

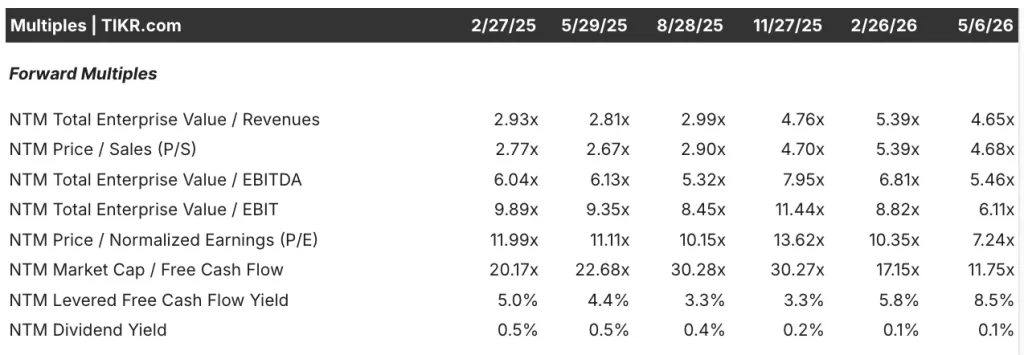

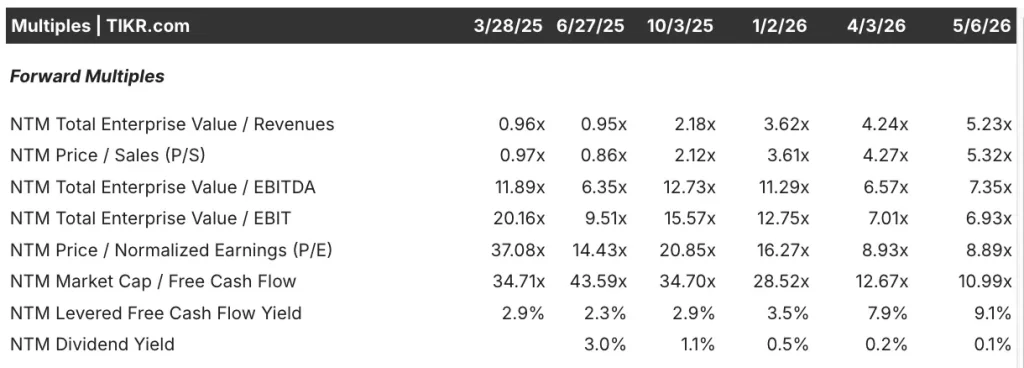

Both Stocks Have Repriced Sharply, But MU Looks Cheaper on Key Metrics

One of the most striking things about both stocks is how quickly their valuations have compressed. Micron traded at around 12x forward P/E just 15 months ago, but it now trades at around 7x. Sandisk’s forward P/E compressed even more dramatically, falling from around 37x in early 2025 to under 9x today.

Forward P/E compares a stock’s price to its expected future earnings. Micron trades at around 7x on this measure, and Sandisk trades at around 9x. Both are cheap relative to the broader semiconductor sector, which typically trades at 20x or higher. However, memory chip companies tend to trade at lower multiples because their earnings are more cyclical.

EV/EBITDA measures a company’s total value relative to its operating earnings before interest, taxes, and depreciation. Micron currently trades at around 5x on this metric, and Sandisk trades at around 7x.

That gap makes Micron look cheaper in operating earnings terms, even though Sandisk has recently grown faster. Both multiples are well below where they stood 12 months ago, showing how fast earnings have outpaced stock prices.

Micron’s stock at $669 trades well above the average analyst price target of $556. That is an unusual dynamic and may mean analysts have not fully updated their models after the big earnings beat.

Sandisk’s stock at $1,359 trades close to the average analyst target of $1,366. That tight gap suggests the street views SNDK as roughly fairly valued at current levels.

See analysts’ full growth forecasts and estimates for SNDK and MU stock (It’s free) >>>

Sandisk’s Upside Story Is Far More Compelling Than Micron’s Right Now

We analyzed the upside potential for Micron stock, which benefits from AI memory demand and a rapidly growing revenue base.

Based on estimates of 55% annual revenue growth, 80% operating margins, and a normalized P/E multiple of 6.1x, the model projects Micron stock could rise from around $667 to around $727 per share.

That would be a 9% total return, or a 3.8% annualized return over the next 2.3 years.

We analyzed the upside potential for Sandisk stock, which is capitalizing on explosive NAND flash demand from AI data centers.

Based on estimates of 70% annual revenue growth, 60% operating margins, and a normalized P/E multiple of 8.9x, the model projects Sandisk stock could rise from around $1,410 to around $2,015 per share.

That would be a roughly 43% total return, or an 18% annualized return over the next 2.1 years.

Based on analysts’ consensus estimates, we see two very different return profiles between Micron and Sandisk. Micron’s model points to a 3.8% annualized return, which is below what most investors consider attractive.

Sandisk’s model points to 18% annualized, driven by steep assumed margin expansion and rapid revenue growth. The key difference is Sandisk’s low starting margin base, so the assumed expansion looks steep but reflects genuine scaling.

Build your own Valuation Model to value any stock (It’s free!) >>>

Which One Do You Actually Buy?

Both companies are benefiting from one of the strongest demand cycles in semiconductor history. Micron is the more established player, with positive free cash flow, diversified products, and stronger margins today.

SanDisk is newer as a public company but growing faster, with quarterly revenue up 97% year over year. The two stocks appeal to very different types of investors.

Micron’s HBM business is among the fastest-growing segments in AI hardware. That segment supplies the extremely fast memory packed inside AI chips made by NVIDIA and others.

However, Micron’s current price of $669 already trades well above the analyst street target of $556. So investors considering Micron today should note the stock may have already priced in much of the good news.

Sandisk’s stronger modeled return and faster growth in the near term make it the more compelling upside story. But Sandisk still carries negative free cash flow and a shorter track record as a public company.

The company’s ability to convert booming datacenter revenue into sustained profitability is the critical test ahead. If Sandisk keeps growing its datacenter business and turns free cash flow positive, then it could become a genuinely compelling opportunity.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Should You Invest in Sandisk or Micron?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up SNDK or MU, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track SNDK or MU alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Sandisk and Micron stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!