Key Stats for Plug Power Stock

- 52-Week Range: $0.69 to $4.58

- Current Price: ~$3.27

- Street Mean Target: ~$3.65 (Hold, 30 analysts)

- 2025 Full Year Revenue: $709.92M

- Q4 2025 Gross Margin: +2.4%

- Full Year 2025 Gross Margin: ~-38%

- Shares Outstanding (2025): ~1.15 billion

Value your favorite stocks like PLUG with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

The Quarter That Changed the Conversation

For years, Plug Power (PLUG) carried the hydrogen dream and the financial pain that came with it. The company builds hydrogen fuel cells, electrolyzers, and the infrastructure needed to produce and distribute green hydrogen at scale.

The problem is that producing green hydrogen is expensive, and Plug was selling it below cost for years to build market share, burning cash at a scale that eventually pushed the stock to an all-time low of $0.69 in May 2025.

What shifted the narrative was Q4 2025. For the first time in recent memory, Plug reported a positive gross margin of 2.4%, a swing of roughly 125 percentage points from the same quarter a year earlier. It is a single quarter, and the full year 2025 gross margin was still around -38%. But direction matters, and the market reacted accordingly, with the stock gaining over 23% on the day results were reported.

A new CEO, Jose Luis Crespo, took the helm in March 2026, with management targeting EBITDAS-positive performance in Q4 2026 and full profitability by the end of 2028.

See analysts’ growth forecasts and price targets for PLUG stock (It’s free!) >>>

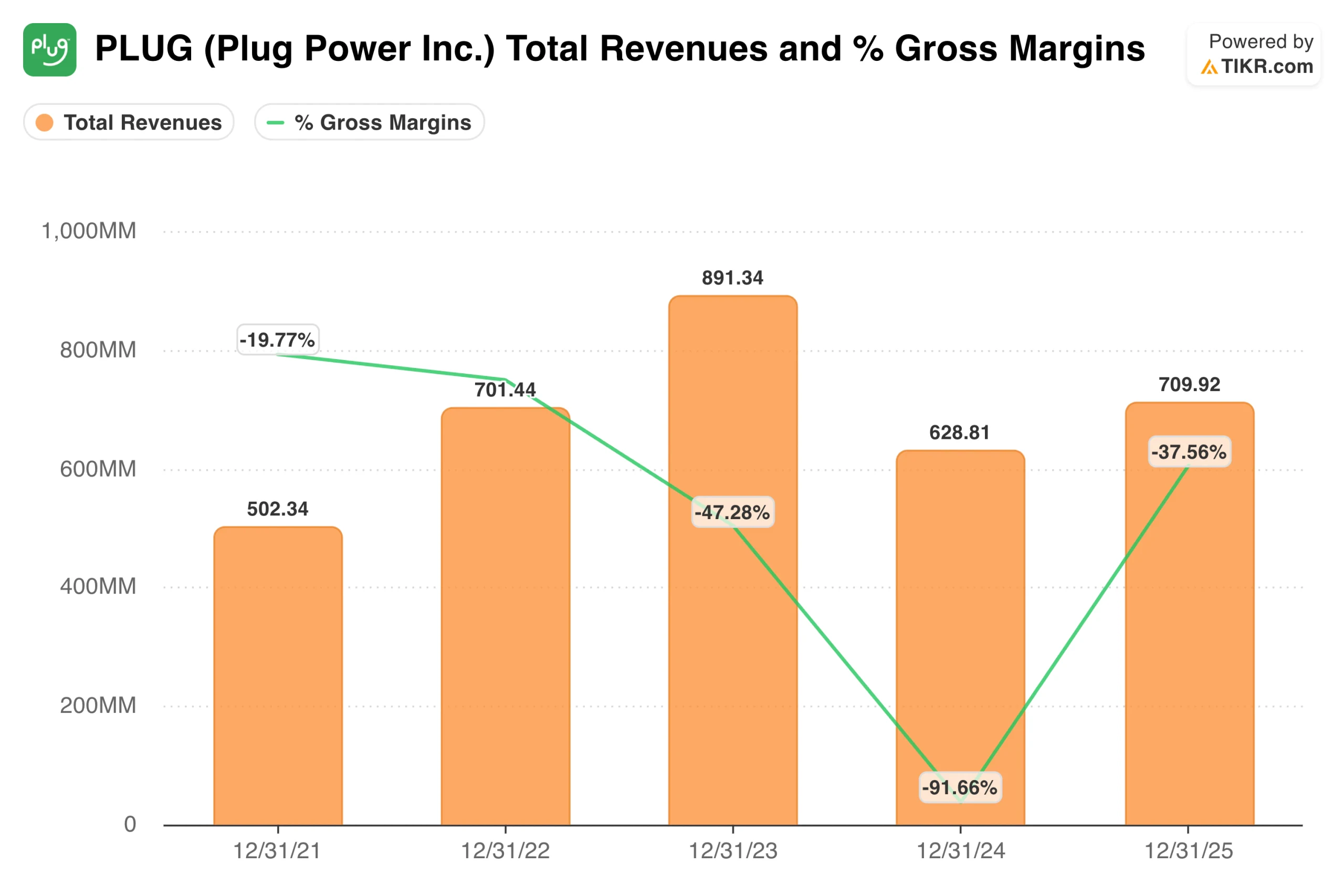

Revenue Grew. Margins Told a Different Story

Plug Power grew revenue from $502 million in 2021 to $891 million in 2023, then fell back to $629 million in 2024 before recovering modestly to $710 million in 2025. That is not the trajectory most investors anticipated when this stock was trading at multiples of today’s price.

The gross margin line is more instructive as margins were already negative at around -20% in 2021, reflecting the economics of a company subsidizing hydrogen fuel for its forklift customers while waiting for scale to bring costs down. By 2024, they had collapsed to around -92%, the worst point in the company’s recent history.

The 2025 recovery to around -38% at the full year level, with Q4 turning positive, is what the current bull thesis rests on. If that trajectory holds through 2026, the business starts to look structurally different from what investors endured over the past two years.

Value Plug Power instantly (Free with TIKR) >>>

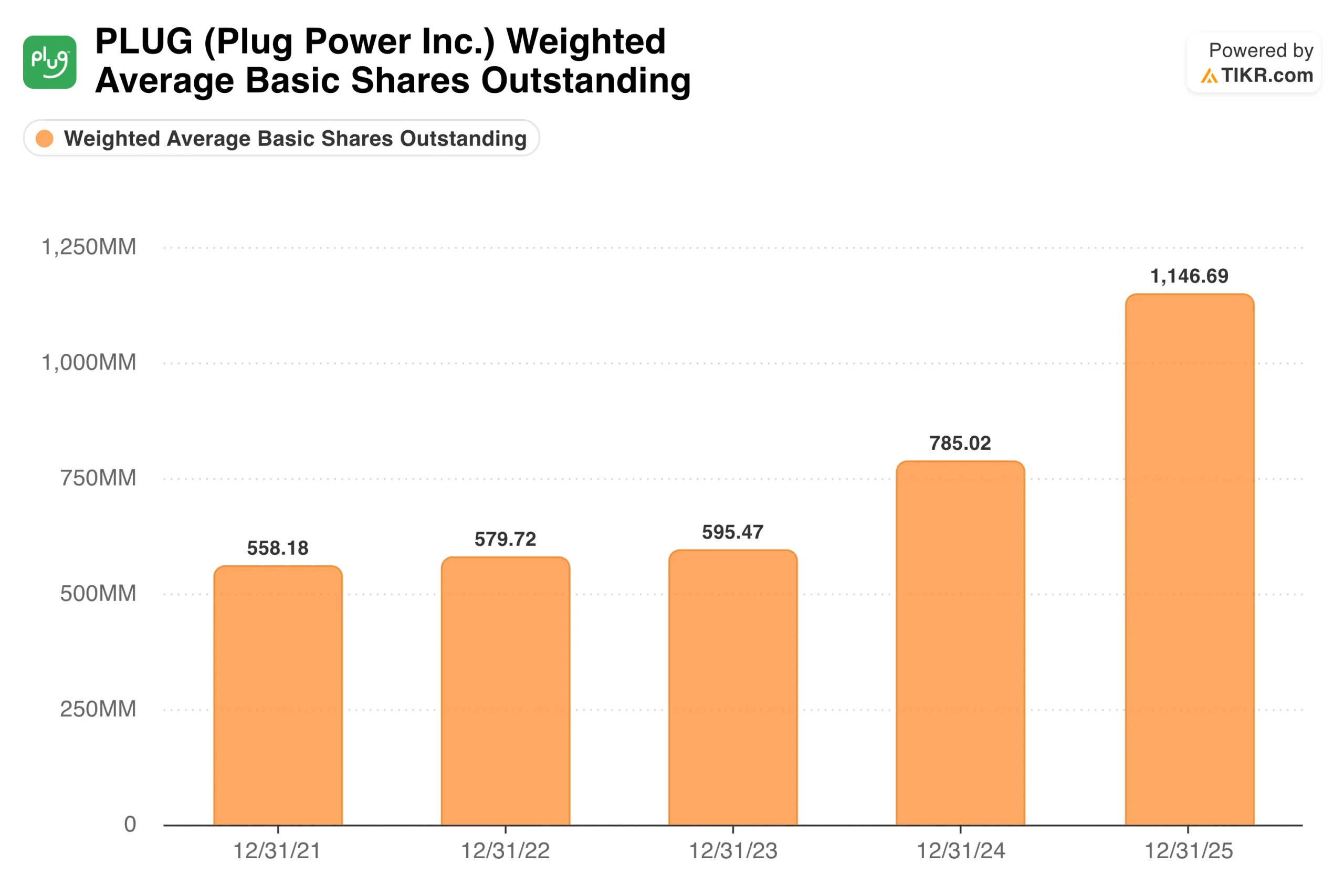

The Chart Wall Street Glosses Over

From 2021 through 2023, Plug’s share count stayed roughly flat between 558 million and 595 million shares. Then it stepped up sharply to 785 million in 2024 and reached roughly 1.15 billion in 2025, more than doubling over the period.

This matters for two reasons. Any per-share improvement in earnings is partly due to losses being spread over more shares, rather than a proportional improvement in the underlying business. And there is no guarantee that further equity issuances are behind us, particularly with cash burn still meaningful and asset monetizations still pending.

The EPS Improvement Is Real. It Also Needs Context

Basic EPS went from -$0.82 in 2021, widened to -$2.68 in 2024, then narrowed to -$1.42 in 2025. But the share count roughly doubled over that same period, which means the per-share improvement somewhat flatters the underlying business’s actual progress.

The narrowing loss does reflect genuine operational improvement. Cash burn declined roughly 26% year over year in 2025, and Project Quantum Leap, Plug’s internal restructuring initiative, is driving real reductions in operating expenses. Investors should be careful when reading EPS in isolation, without accounting for the shares issued to produce it.

What Has to Go Right, and What Could Go Wrong

The bull case rests on a few specific things. Gross margins need to continue improving through 2026 toward breakeven on a full-year basis. The planned asset monetizations targeting over $275 million in proceeds need to close. And the electrolyzer pipeline needs to convert into revenue, with the 275 MW Hy2gen Canada contract being the most visible near-term example.

The bear case does not require the hydrogen thesis to be wrong. It just requires the timeline to slip. Plug has missed its own targets before, and cash on hand at year-end 2025 was $368.5 million against over $535 million in operating cash burn for the year. The company also closed a $1.66 billion DOE loan guarantee in January 2025 and later suspended activities under that program, which reset expectations for its production buildout.

Q4 2025 proved that the business model can produce a positive gross margin. What it did not prove was that it could do so consistently at scale without continued dilution.

Should You Invest in Plug Power

Plug Power is not a company you can evaluate with a standard earnings multiple. What you are really assessing is whether execution over the next two to three years matches the targets management has laid out.

The Q4 2025 gross margin turn is the first hard evidence in years that the cost structure is improving in a durable way. A new CEO, a clearer capital plan, and a growing electrolyzer pipeline give the bull thesis more credibility today than it had 18 months ago.

But share dilution has been severe, the cash runway depends on asset sales closing on schedule, and full profitability extends to the end of 2028, according to management’s own projection. Analyst consensus is Hold, with a mean target of around $3.65, while the three most recent ratings from Susquehanna, Jefferies, and Wells Fargo average closer to $2.20.

The two metrics worth watching most closely through 2026 are gross margin progression and whether the planned asset monetizations close on schedule.

See analysts’ growth forecasts and price targets for Plug Power stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!