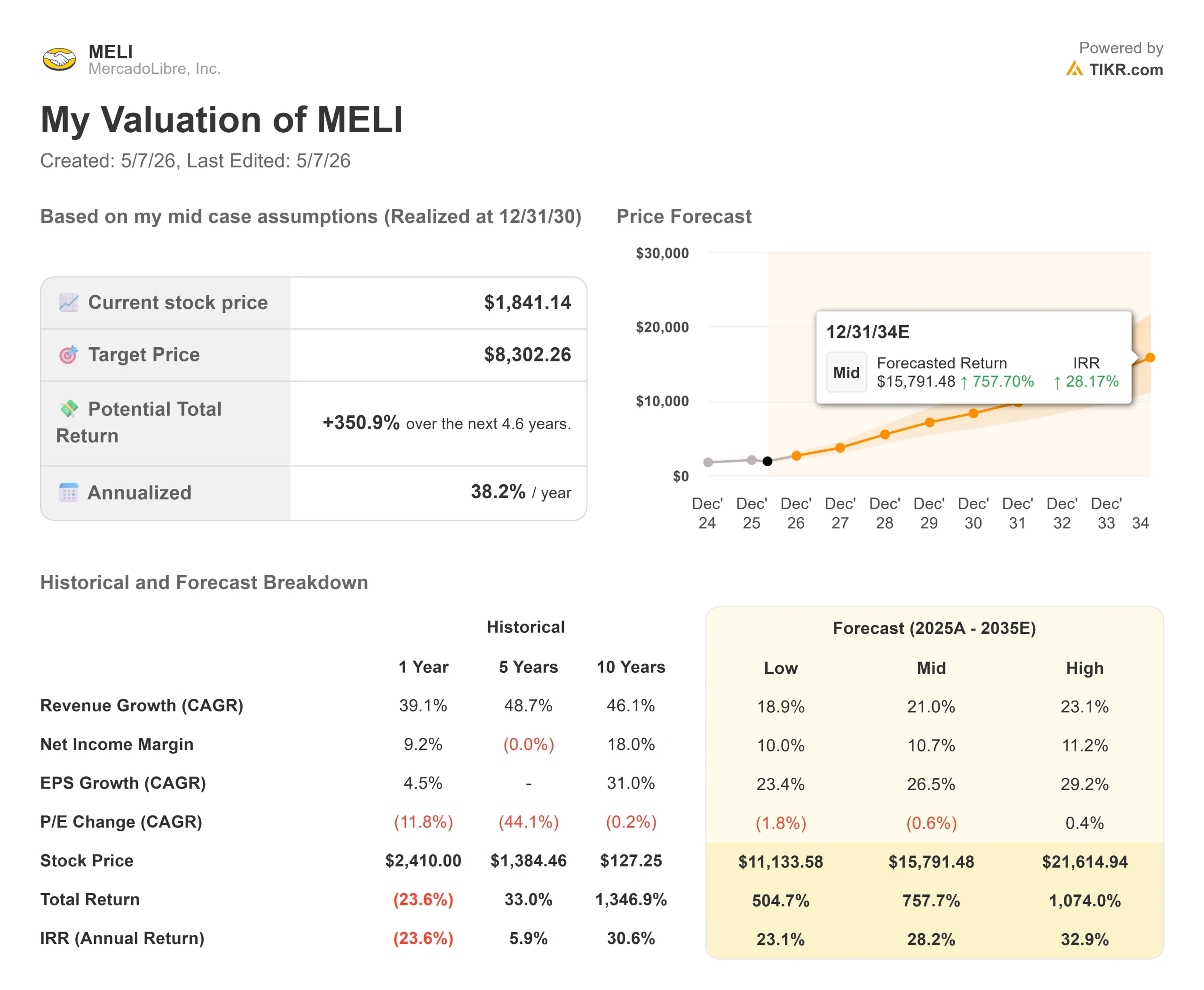

Key Stats for MercadoLibre Stock

- Current Price: $1,876.91

- Target Price (Mid): ~$8,302

- Street Target: ~$2,440

- Potential Total Return: ~351%

- Annualized IRR: ~38% / year

- Earnings Reaction: -8.05% (2/24/26)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Investors have punished MercadoLibre (MELI) hard in 2026, pushing the stock to a max drawdown of 38.80% on March 27 and leaving it nearly 30% below its 52-week high of $2,645.22 as Q1 2026 earnings arrive tonight. Bulls say the margin compression is deliberate and temporary, a planned offensive to capture Latin America’s offline-to-online shift before competitors can. Bears, now including UBS and JP Morgan, say the investment cycle has no clear end date, and the valuation is only fair at best. Both sides are looking at the same data. The disagreement is entirely about timing.

How Far Has MELI Fallen, and Why?

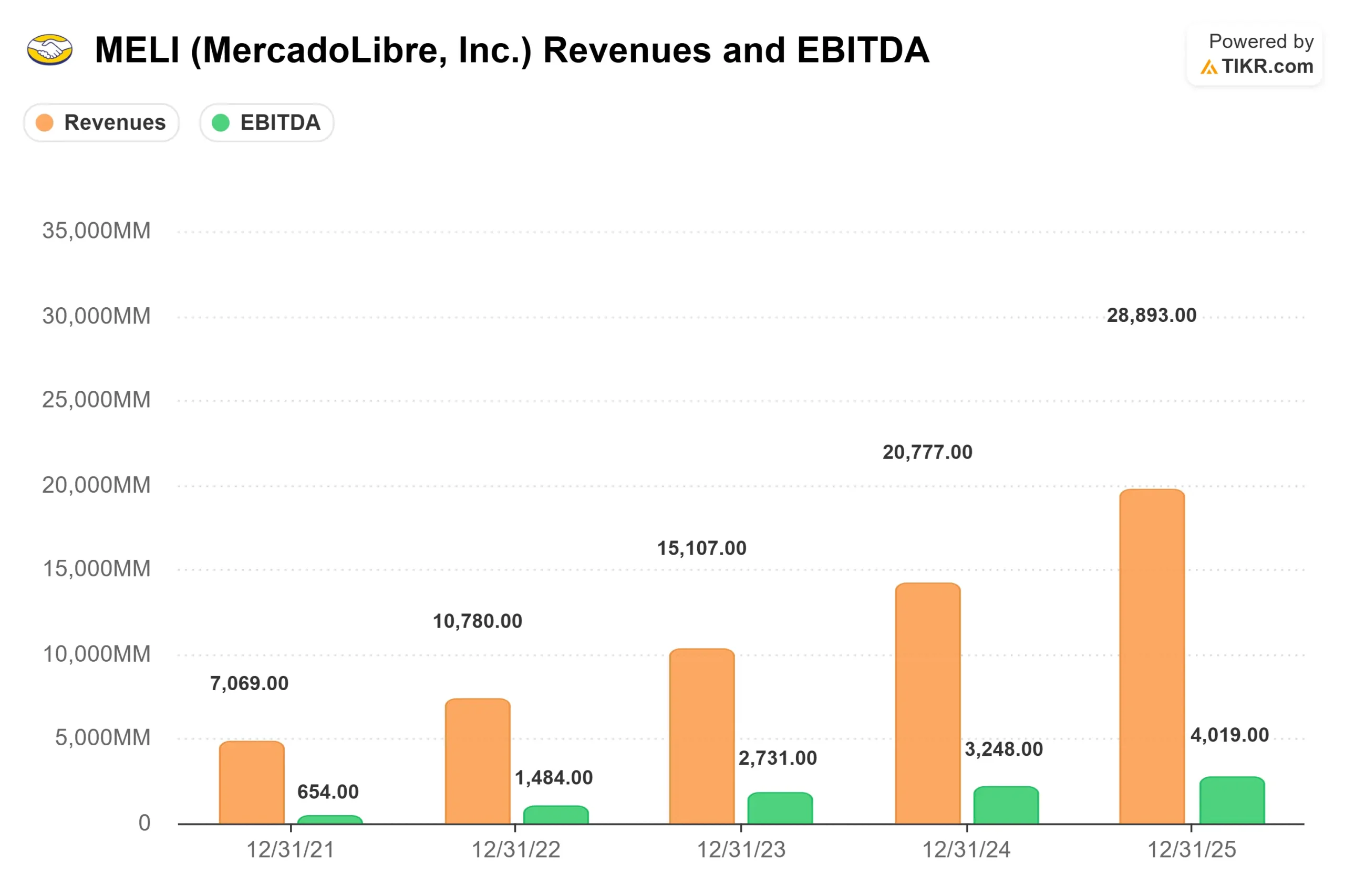

The stock’s slide from $2,645.22 to $1,876.91 is not due to deteriorating fundamentals. Full-year 2025 revenue grew 39% to $28.893 billion, and operating cash flow reached $12.116 billion, up 53% year-over-year. What the market is pricing in is doubt about when the heavy spending pays off.

On the Q4 2025 earnings call, CFO Martin de los Santos was explicit about what is causing the pressure: a 5-to-6 percentage point operating margin hit from four deliberate investments: lowering Brazil’s free shipping threshold, expanding credit cards across Brazil, Mexico, and Argentina, scaling first-party retail, and building cross-border trade from China. Each has a measurable growth output attached to it.

Jefferies upgraded MELI to Buy on April 7 with a $2,600 target, noting that earnings downgrades driven by margin compression had sent the valuation to record lows in both absolute and relative terms, while the investment was proving to be a strong revenue driver. UBS took the opposite view on April 29, downgrading to Neutral and cutting its target to $2,050, arguing that margin recovery would not arrive until 2027 at the earliest and that the valuation was fairly priced for the uncertainty ahead.

See historical and forward estimates for MercadoLibre stock (It’s free!) >>>

The Growth Engine Underneath the Margin Pressure

The Q4 2025 transcript shows a business accelerating on three fronts simultaneously.

In commerce, CEO Ariel Szarfsztejn (who assumed the role on January 1, 2026, succeeding founder Marcos Galperin, who became Executive Chairman) confirmed the results of lowering Brazil’s free shipping threshold were “very much aligned to what we were planning for.” Items sold in Brazil grew 45% year-over-year in Q4, accelerating from 26% in Q2 and 42% in Q3. GMV expanded 35% in both Brazil and Mexico. Conversion rates, buyer retention, and new buyer acquisition all hit records.

In fintech, Mercado Pago now holds the leading Net Promoter Score (a customer loyalty measure) in Brazil, Mexico, Argentina, and Chile simultaneously. Monthly active users have grown close to 30% for ten consecutive quarters. The credit portfolio nearly doubled year-over-year to $12.5 billion. Nearly 3 million new credit cards were issued in Q4, up from 1.5 million in Q2. CFO de los Santos confirmed that credit card cohorts older than two years in Brazil are already generating positive net interest margin after loan losses, which establishes a clear timeline for when the credit book flips from drag to driver.

In advertising, revenue grew 67% on an FX-neutral basis in Q4, powered by AI bidding tools, automated campaign management, and a budget orchestration system. Szarfsztejn noted this revenue stream remains small as a percentage of GMV “compared to its potential,” making it an early-innings compounder.

One number that deserves attention: the Mercado Pago AI assistant now resolves 87% of customer interactions without human intervention, and 20% of GMV is advised by MercadoLibre’s seller assistant. This is AI at operating scale, not in a pilot phase.

See how MercadoLibre performs against its peers in TIKR (It’s free!) >>>

Is the Valuation Cheap Enough?

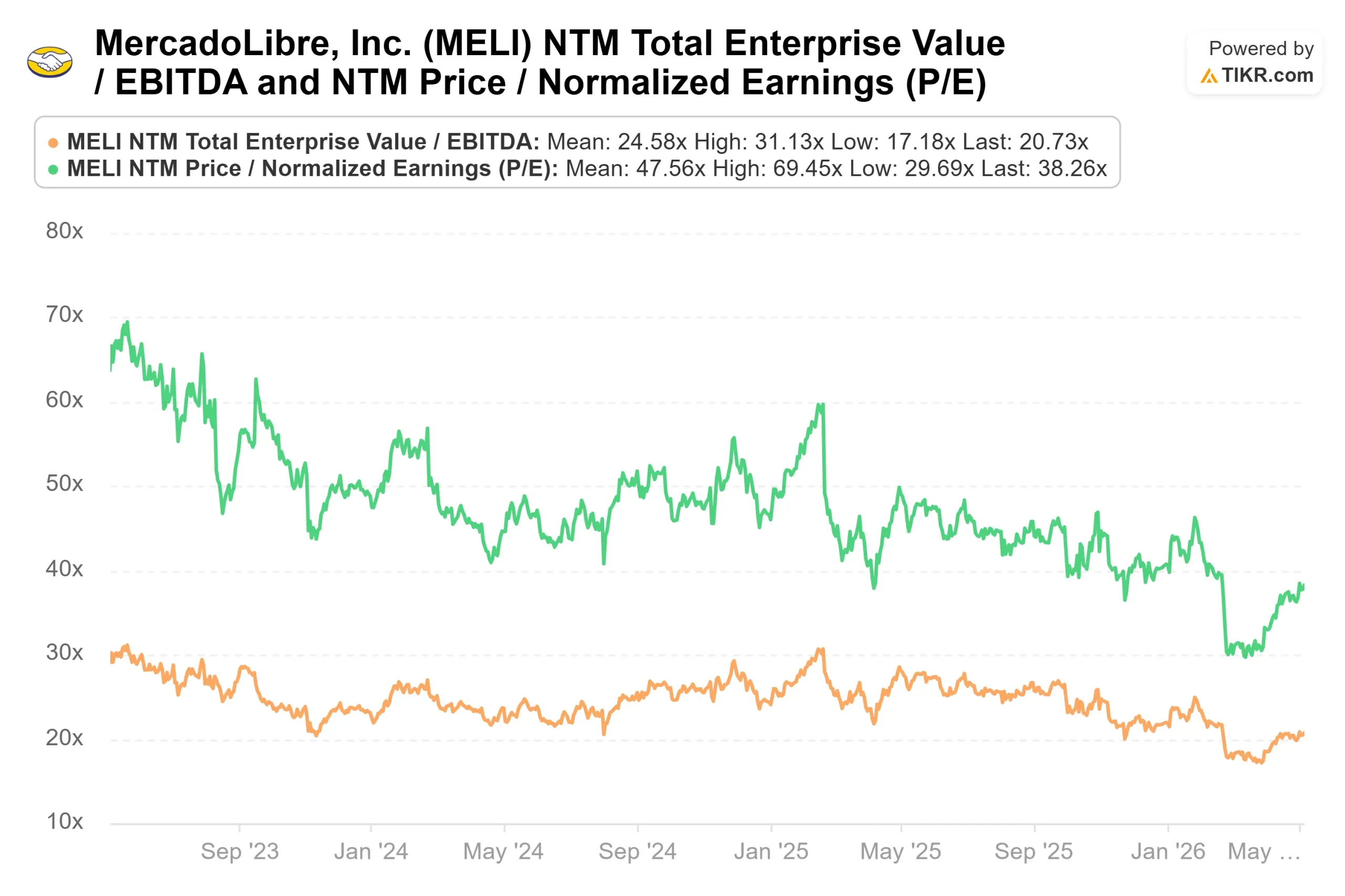

From TIKR’s multiples data, the NTM EV/EBITDA sits at 20.73x and NTM P/E at 38.26x, both at multi-year lows for MELI. The street mean target of $2,439.88 across 25 price estimates (18 Buys, 6 Outperforms, 2 Holds, 0 Underperforms, 0 Sells) implies around 30% upside from today’s price.

The path to that upside runs through one question: when does the credit card book reach profitability on an average basis across all cohorts, not just the older ones? De los Santos answered it partially: the consumer credit business already runs net interest margins after loan losses in the high 30s to high 40s. The credit card is not yet NIMAL-positive on average, but Brazil cohorts older than two years already are. When Mexico and Argentina cohorts mature, a significant cost drag flips into a revenue engine.

The bear case is equally clear. Cross-border trade from China is still scaling. First-party retail is not yet profitable on a fully allocated basis. The credit card ramp in Mexico and Argentina is early-stage. Any of these extending longer than expected compresses ROIC and delays the re-rating. The free cash flow picture is distorted by credit book expansion: levered FCF is negative because MercadoLibre is funding a rapidly growing loan portfolio. Operating cash flow of $12.116 billion tells a more accurate story about the underlying business.

TIKR Advanced Model Analysis

- Current Price: $1,876.91 (TIKR model entry price: $1,841.14)

- Target Price (Mid): ~$8,302

- Potential Total Return: ~351%

- Annualized IRR: ~38% / year

See analysts’ growth forecasts and price targets for MercadoLibre stock (It’s free!) >>>

The mid-case model uses a 21% revenue CAGR through 2030. The two primary growth drivers are GMV acceleration in Brazil and Mexico as buyer frequency compounds from the free shipping investment, and Mercado Pago revenue is growing as the credit card book matures across three markets. The margin driver is operating leverage returning as credit card cohorts reach profitability and fulfillment costs normalize, lifting net income margins toward around 11%. The primary risk is the investment cycle extending into 2028, compressing margins, and delaying the re-rating.

The upside: margin stabilization in 2026 alongside continued GMV growth re-rates the stock toward the street consensus near $2,440 near-term, with the model’s ~$8,302 mid-case by 12/31/30 representing a ~351% total return at a ~38% annualized IRR. The downside: if margin deterioration deepens with no clear improvement timeline, the stock tests its 52-week low of $1,593.21.

Conclusion

Watch Brazil’s items sold growth rate in tonight’s Q1 2026 results. It was 45% in Q4. If it holds above 35% alongside any improvement in Brazilian commerce margins, the investment is holding, and operating leverage is beginning to show. If it decelerates below 30% with no margin improvement, the bear case gets oxygen.

MercadoLibre has delivered 28 consecutive quarters of above-30% revenue growth while investing aggressively to own markets that remain heavily underpenetrated for digital commerce and financial services. Tonight’s print will tell us how much patience the market still has.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in MercadoLibre?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up MercadoLibre, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track MercadoLibre alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze MercadoLibre on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!