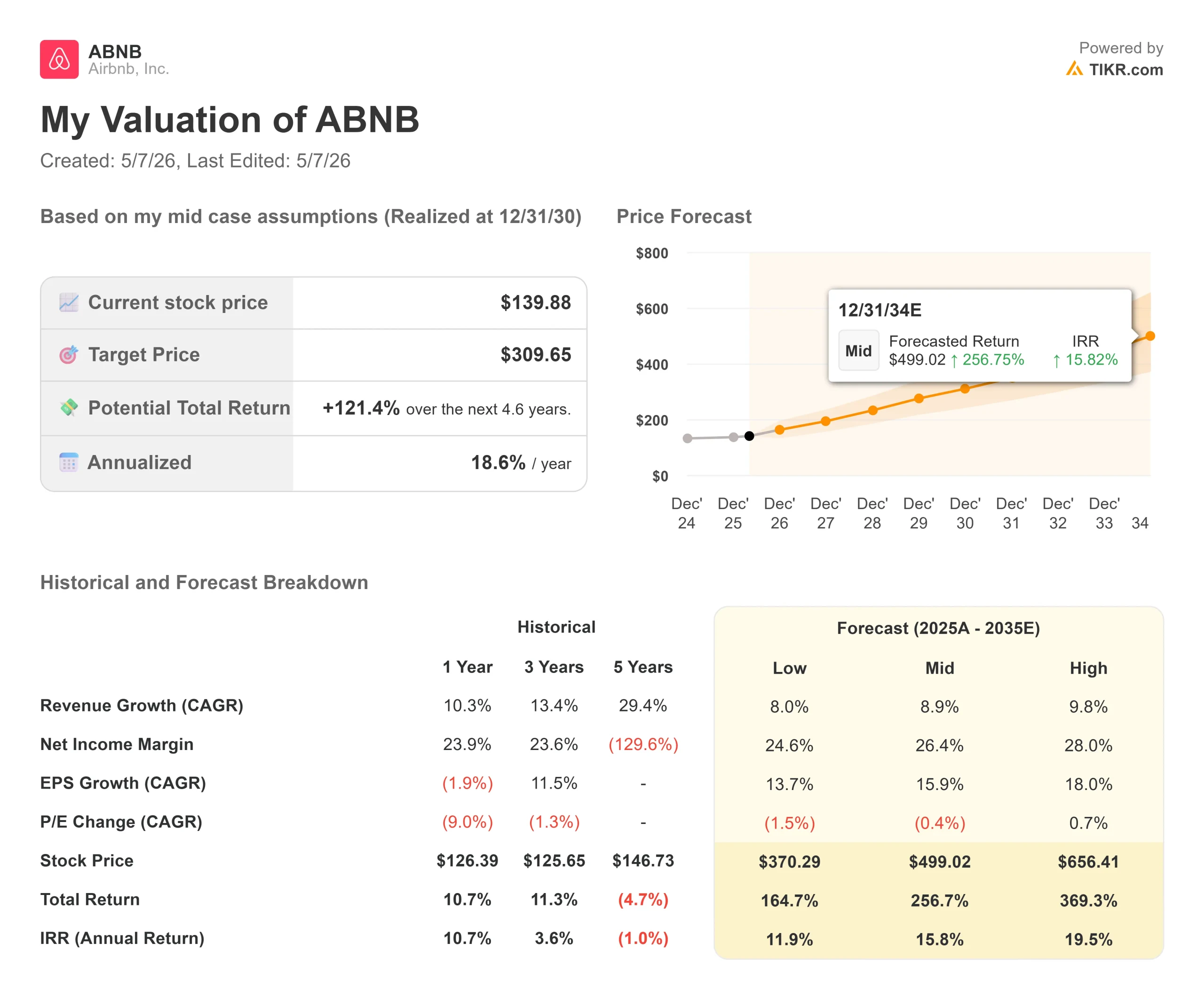

Key Stats for Airbnb Stock

- Current Price: $139.88

- Target Price (Mid): ~$310

- Street Target: ~$149

- Potential Total Return: ~121%

- Annualized IRR: ~19% / year

- Earnings Reaction (Q4 2025, 2/12/26): +4.65%

- Max Drawdown: 21.54% (11/20/25)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Two Upgrades, One Earnings Day

Travel stocks have had a complicated 2026. Airbnb (ABNB) is up just 2.3% year to date, lagging the broader market as geopolitical uncertainty and consumer spending pressure weigh on sentiment. But the analyst community is turning more constructive. On May 4, Oppenheimer analyst Jed Kelly raised his rating from Perform to Outperform with a $180 price target, citing conviction that Airbnb’s hotel expansion, Reserve Now Pay Later offering, and AI-powered search will generate durable revenue acceleration not yet reflected in consensus. Wells Fargo moved to Overweight at $178 on April 22. The Street’s mean sits at $149, just 6.5% above where the stock trades today.

The central question is whether the product rebuild Airbnb has been running for three years is now compounding fast enough to justify a re-rating. Tonight’s Q1 2026 results are the next test.

Bulls point to confirmed re-acceleration in Q4 and Q1 guidance of 14% to 16% revenue growth. Bears counter that regulatory pressure is tightening supply in key European cities and New York, and that geopolitical uncertainty could weigh on bookings in Q2 and Q3. Tonight’s numbers decide which side gets new ammunition.

See historical and forward estimates for Airbnb stock (It’s free!) >>>

What the Q4 Transcript Reveals

The Q4 re-acceleration was not a macro gift. It came from a structured internal product framework, CEO Brian Chesky called Project Hawaii, where a focused team was given one mandate: make it easier to find and book a home on Airbnb. The team shipped hundreds of improvements across search, checkout, and app conversion. Chesky said those changes “drove hundreds of millions of dollars in revenue in 2025 alone.”

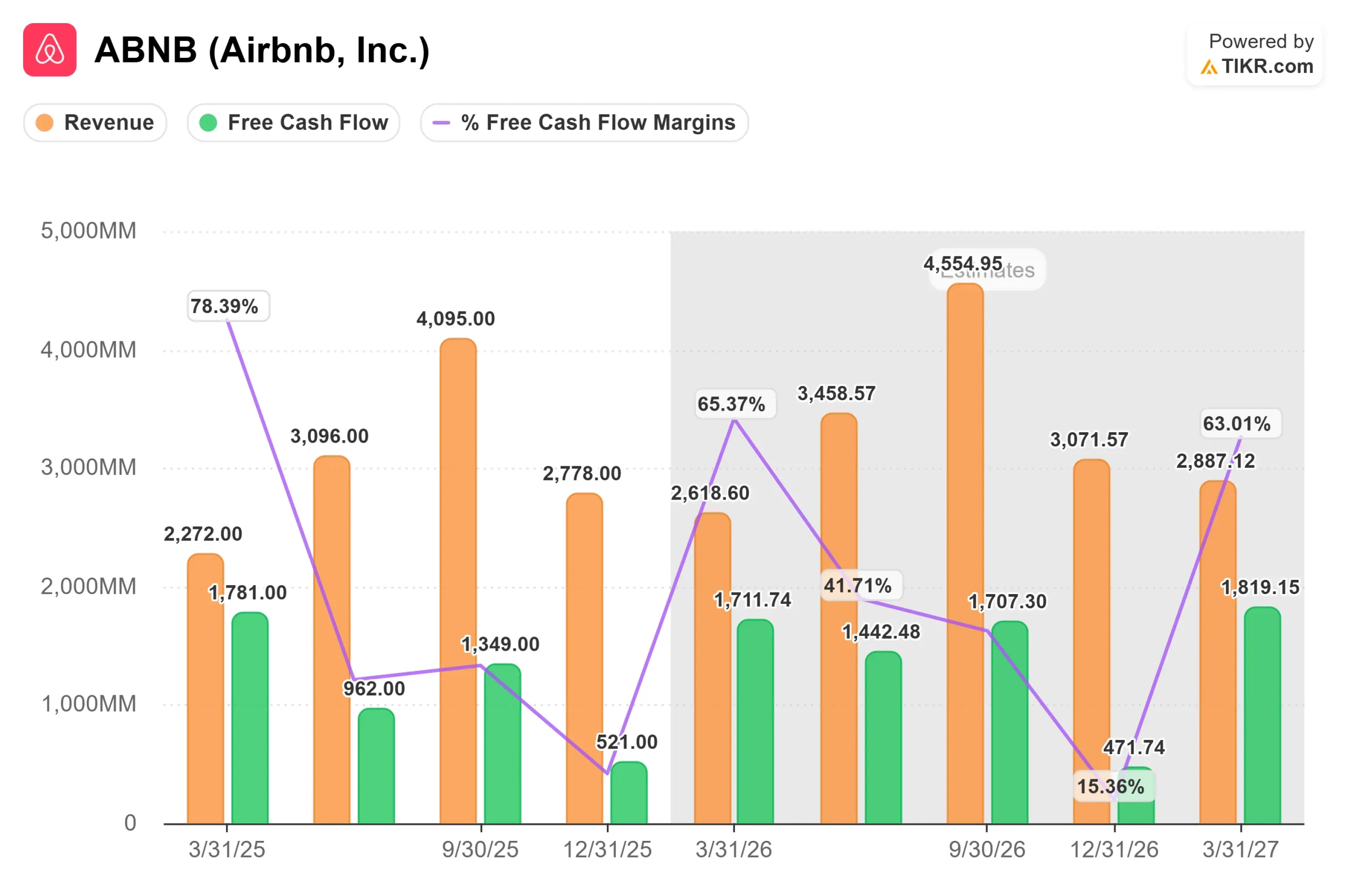

Three specific product launches in Q4 drove over 200 basis points of nights booked growth and roughly 300 basis points of gross booking value (GBV, meaning the total value of all reservations placed before cancellations) growth, according to CFO Ellie Mertz. The most impactful was Reserve Now Pay Later (RNPL), which lets eligible U.S. guests hold a booking at $0 upfront. RNPL shifted demand toward larger entire homes, extended booking lead times, and lifted average daily rate (ADR, the revenue earned per occupied night). Mertz confirmed the platform-wide aggregate increase in cancellation rate from RNPL was approximately 1%.

Supply quality also improved materially. Airbnb removed more than 500,000 low-quality listings in 2025 while Guest Favorites, its highest-rated listings, grew 30% year over year. By Q4, Guest Favorites represented nearly half of all bookings. Chesky said the net promoter score (NPS) is the strongest it has been since the pandemic.

On AI, Chesky pushed back on disintermediation fears directly: “The models in ChatGPT, the models in Gemini, the models in Claude are available to every single company. So pretty soon, every company becomes an AI platform if they make the shift.” Airbnb hired Ahmad Al-Dahle, who built Meta’s Llama models, as Chief Technology Officer to lead that shift. The AI customer support agent already resolves nearly one-third of English-language tickets in North America without a human. Voice-based AI support and global rollout are both planned for 2026.

Hotels are the longest-duration optionality in the story. Oppenheimer estimates hotels could add around 3 percentage points to Airbnb’s nights growth at minimal incremental cost, citing Manhattan specifically, where hotel supply is roughly 3 million nights below 2019 levels due to tighter regulation. Hotels represented a single-digit share of total nights booked in Q4 but were growing at nearly double the platform’s overall rate, per CFO Mertz on the earnings call.

Internationally, Brazil moved from a top-10 to a top-5 market after Airbnb introduced local payment methods and culturally targeted campaigns. In Q4, Brazil was Airbnb’s second-largest contributor of first-time bookers behind only the U.S. India grew bookings 50% year over year in the most recent quarter and is the next major priority. Airbnb generates more than 60% of its revenue internationally, per TIKR’s Segments data, but Chesky noted on the call that roughly 70% of that revenue comes from just five countries, which means the international expansion runway remains large.

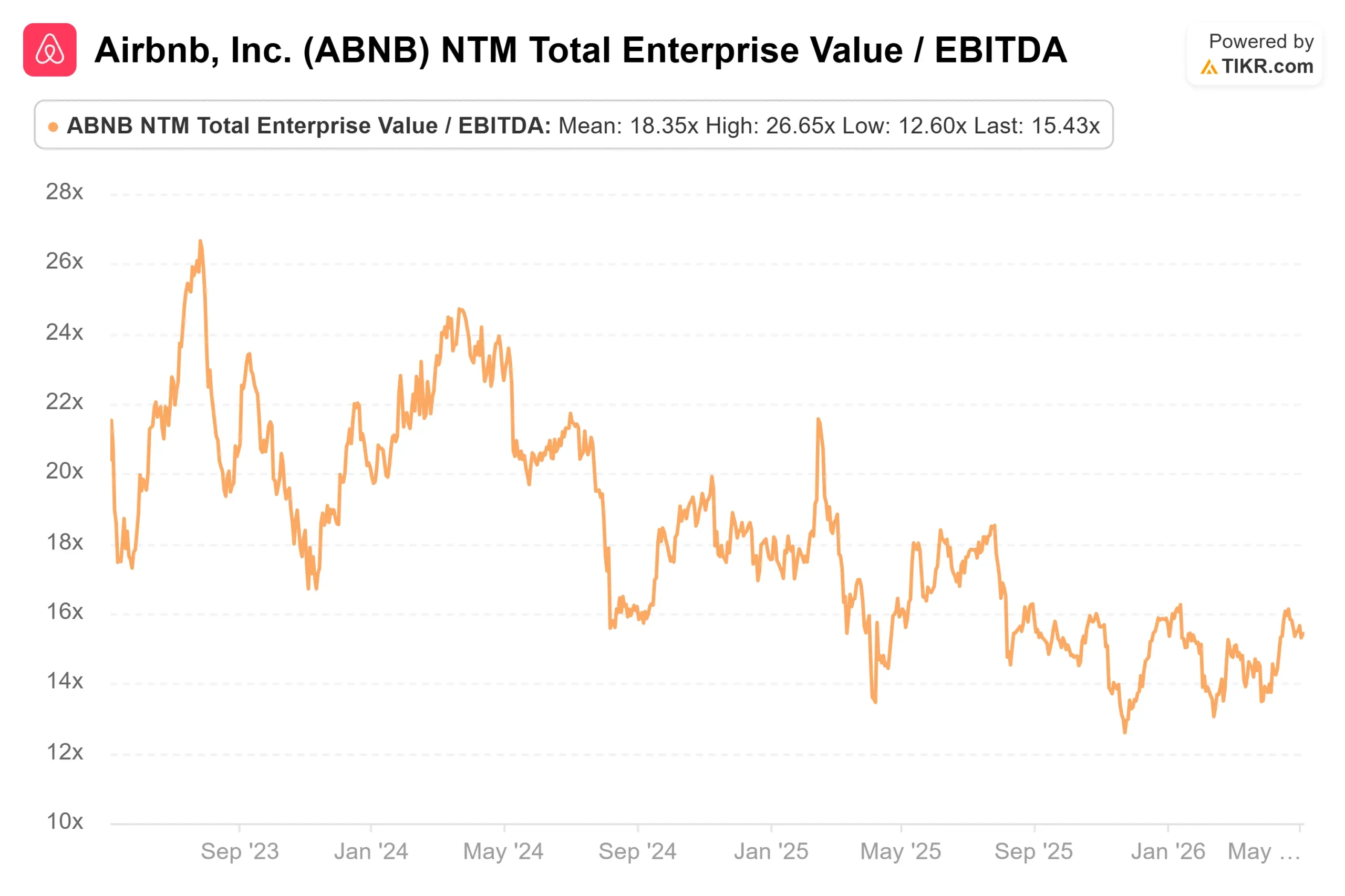

Airbnb trades at 15.43x NTM EV/EBITDA against a peer mean of 14.05x, per TIKR’s Competitors page. Booking Holdings (BKNG) sits at 11.98x and Expedia (EXPE) at 7.94x. Hilton (HLT) trades at 20.81x and Marriott (MAR) at 18.63x. Airbnb’s modest premium reflects a structural advantage that its peers cannot match: an 83.0% LTM gross margin on an asset-light model with no inventory, no capital expenditure, and a free cash flow margin of around 37% in 2025.

See how Airbnb performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $139.88

- Target Price (Mid): ~$310

- Potential Total Return: ~121%

- Annualized IRR: ~19% / year

See analysts’ growth forecasts and price targets for Airbnb stock (It’s free!) >>>

The TIKR model uses the mid-case scenario, which assumes a revenue CAGR of around 9% through 12/31/30. Two forces drive it. First, international expansion: Brazil and India are following a repeatable focused-team playbook, and Airbnb currently generates more than 60% of its revenue internationally, with most of it concentrated in just five countries, leaving a large untapped runway. Second, RNPL and Project Hawaii product improvements are extending to new markets and booking segments through 2026 and beyond. The margin driver is net income expanding from 20.5% in 2025 toward around 26% by 2030, supported by an asset-light model where, as Chesky noted, AI investment “will not affect the P&L.”

Airbnb’s own data shows searches for World Cup host city stays are up 80% during tournament dates, with approximately one in six World Cup guests in North America booking with Airbnb for the first time. Chesky also noted on the earnings call that 40,000 Paris Olympics hosts have continued listing since the Games ended, demonstrating that events add supply at no incremental cost to the platform.

The primary risk is regulatory. New York City’s Local Law 18 eliminated more than 90% of short-term rental supply there, and similar restrictions are advancing in Barcelona, Paris, and Amsterdam. If major European cities replicate that approach, GBV growth could underperform the model’s revenue CAGR regardless of product execution. Oppenheimer notes that at roughly 14x 2027E EBITDA, the current valuation implies limited downside even if hotel and RNPL initiatives do not scale as planned.

The Street’s $149 mean target implies around 6.5% upside and reflects a market waiting for confirmation. The TIKR mid-case requires neither hotels nor AI search to work perfectly. It requires Airbnb to compound revenue at around 9% annually while holding gross margins above 82%, something it has already demonstrated across four consecutive fiscal years.

Conclusion

Watch Nights and Seats Booked growth in tonight’s Q1 report. Airbnb guided high-single-digit growth for this figure. If the actual number meets or exceeds guidance, it confirms that RNPL and Project Hawaii are durable platform improvements, not a one-quarter launch effect. Q1 2026 results are released after market close on May 7, 2026. Airbnb is not the hypergrowth platform it was in 2022. It is a cash-generating marketplace with an 83.0% gross margin, a free cash flow margin of around 37%, and a product team applying the same innovation framework to hotels, experiences, and AI search simultaneously. The TIKR mid-case says the market has not priced that in.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Airbnb?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Airbnb, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Airbnb alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!