Key Stats for Snap Stock

- Current Price: $6.28

- Target Price (Mid): ~$32

- Street Target: ~$8

- Potential Total Return: ~417%

- Annualized IRR: ~42% / year

- Earnings Reaction: (7.40%) (May 6, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Snap (SNAP) delivered its strongest profitability quarter in years on May 6, and the market punished it anyway. Shares fell 7.4% after hours, even as the company beat on revenue, crushed EBITDA estimates, and narrowed its net loss. Bulls see a platform that finally has cost discipline and a diversifying revenue base. Bears point to soft Q2 guidance, a terminated AI partnership, and a large-advertiser segment that has not yet recovered. The key question investors are wrestling with right now is whether this quarter marks a real turning point, or just a favorable setup before conditions get tougher.

Q1 Was Better Than the Reaction Suggests

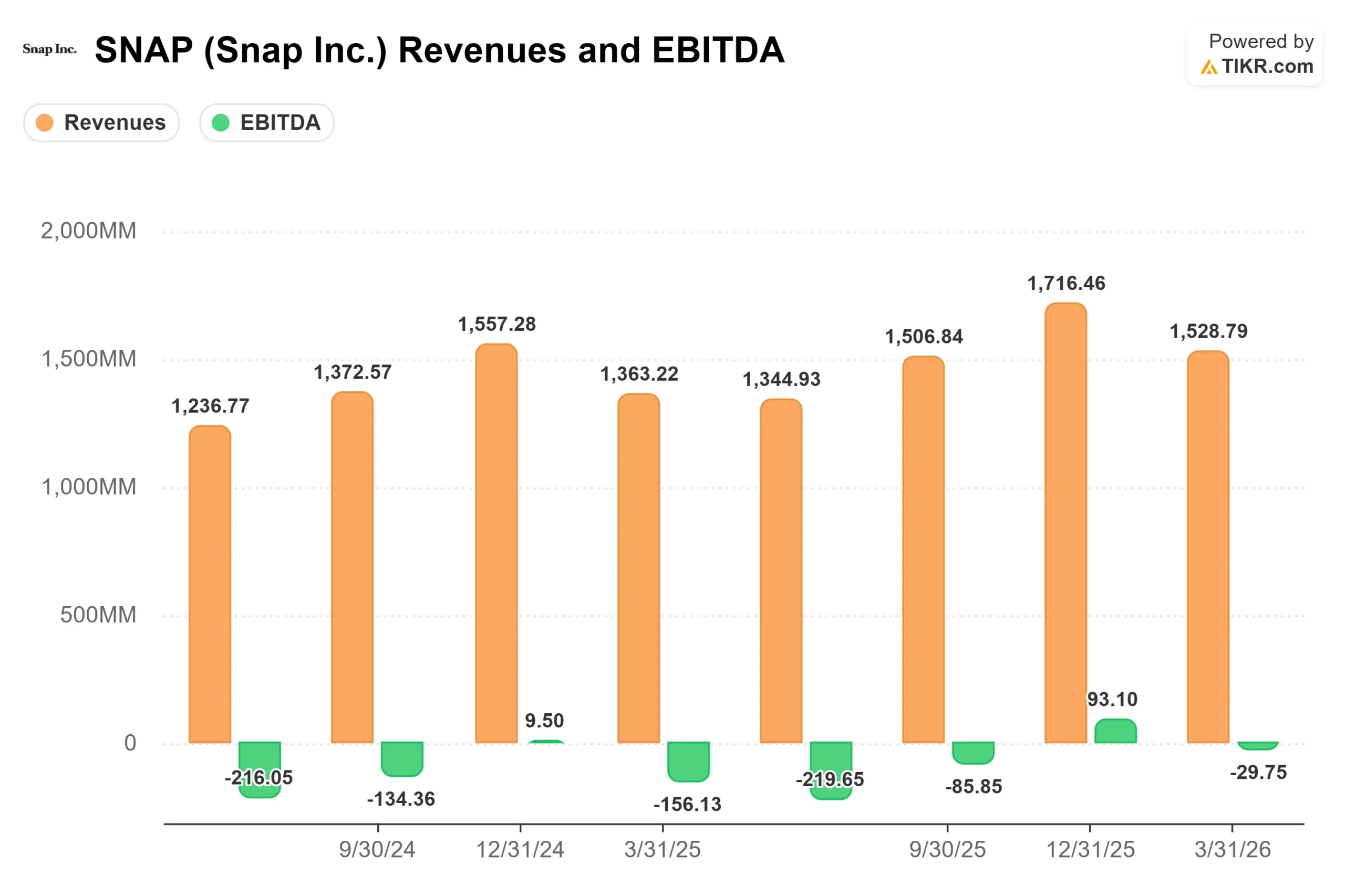

Snap reported Q1 2026 revenue of $1.53 billion, up 12% year-over-year and at the high end of guidance. Adjusted EBITDA came in at $233 million, beating the $215 million consensus by 8.6% and more than doubling from $108 million a year earlier, per TIKR. Free cash flow reached $205.56 million in Q1, per TIKR’s Beats & Misses data, while the trailing twelve-month levered FCF stands at $662 million. Net loss narrowed to $89 million from $140 million in Q1 2025.

Two things spooked the market. Q2 revenue guidance of $1.52 billion to $1.55 billion gave analysts no reason to raise full-year estimates. Snap also disclosed it had ended its Perplexity AI partnership in Q1, removing a high-margin contribution that had been expected later in 2026. As CFO Derek Andersen stated on the call, guidance “assumes no contribution from Perplexity.”

See historical and forward estimates for Snap stock (It’s free!) >>>

The Restructuring Changes the Math

In April, Snap announced it would cut approximately 1,000 employees, or 16% of its global workforce, citing AI-driven efficiency gains. The company expects to reduce its annualized cost base by more than $500 million in the second half of 2026. Activist investor Irenic Capital Management, which disclosed a roughly 2.5% stake in Snap’s Class A shares in March, had been publicly pushing for exactly this kind of cost discipline. The stock rose 7% to 8% the day the layoffs were announced.

That $500 million in savings is not yet in the numbers. Andersen confirmed the full impact hits in Q3 and beyond, with restructuring charges of $95 million to $130 million creating a near-term net income headwind in Q2. But adjusted gross margin already expanded 3 percentage points year-over-year to 57% in Q1. Andersen said on the call that the company believes this “puts us on track for achieving our goal of 60% or better for fiscal 2026.” With gross margins expanding and over $500 million in operating cost reductions arriving in H2, GAAP net income profitability is becoming calculable rather than theoretical.

Subscriptions Are Now a Real Second Engine

Snap’s Other Revenue segment, driven primarily by Snapchat+ subscriptions, grew 87% year-over-year to $285 million in Q1 and now represents roughly 19% of total revenue. CEO Evan Spiegel, Co-Founder and Chief Executive Officer of Snap Inc., explained the logic on the call: subscriptions reduce dependence on the advertising cycle and carry attractive margin characteristics at scale.

Two newer tiers are driving the acceleration. Memories storage pulled in more new subscribers than management expected, and many upgraded to higher-ARPU (average revenue per user) plans. Lens+, a premium tier providing exclusive AI-powered camera lenses, is contributing to both higher subscription ARPU and gross margin expansion. These are structural improvements, not one-quarter anomalies.

See how Snap performs against its peers in TIKR (It’s free!) >>>

The Ad Recovery Is Real but Still Uneven

Total advertising revenue grew 3% year-over-year to $1.24 billion in Q1, held back by an estimated $20 million to $25 million impact from Middle East geopolitical tensions in March, and continued softness among large North American brand advertisers.

The underlying platform data is improving. According to Measured, a third-party ad measurement firm cited by Spiegel on the earnings call, median incremental return on ad spend on Snapchat grew 104% between the April-to-September 2025 period and the October 2025-to-March 2026 period. North America upfront advertising commitments for 2026 grew approximately 10% year-over-year, per Andersen, a leading indicator that agencies are allocating more budget to Snap. SMB (small and medium-sized business) advertisers grew their North America spend by more than 30% year-over-year in Q1. Dynamic Product Ads revenue grew more than 30% year-over-year. App Purchases revenue grew 87% year-over-year.

Large brand advertisers typically plan on quarterly or semiannual cycles, meaning revenue lags platform improvements. The upfront data suggests a recovery is building, but it has not fully flowed through to reported revenue yet.

On valuation multiples, Snap trades at 1.71x NTM EV/Revenue and 9.40x NTM EV/EBITDA per TIKR. Pinterest (PINS) trades at 2.36x NTM EV/Revenue and 8.21x NTM EV/EBITDA. Snap’s revenue discount to Pinterest is notable, given that both platforms target similar performance advertisers. Pinterest reached GAAP profitability earlier, which partly explains the gap. Whether Snap closes that discount depends on how quickly this year’s cost cuts translate into GAAP earnings.

TIKR Advanced Model Analysis

- Current Price: $6.28

- Target Price (Mid): ~$32

- Potential Total Return: ~417%

- Annualized IRR: ~42% / year

See analysts’ growth forecasts and price targets for Snap stock (It’s free!) >>>

The TIKR mid-case model, built at an entry price of $6.11, projects a target of ~$32 by December 31, 2030, representing a potential total return of around 417% and an annualized IRR of approximately 42%. The live price of $6.28 modestly reduces that implied return.

The two revenue CAGR drivers are subscription revenue compounding well above 30% annually as Snap layers in new tiers, and advertising recovering as large brand budgets respond to improved measurement. TIKR consensus estimates model total revenue growing at approximately 9% annually through 2030, reaching around $9.1 billion. The margin driver is gross margin expanding from 57% toward 60%+, amplified by more than $500 million in annualized cost reductions arriving in H2 2026.

The upside scenario is Specs. Snap’s augmented reality (AR) glasses, which overlay digital content onto the physical world, are expected to launch commercially in 2026, with a presentation at Augmented World Expo on June 16. A successful consumer launch opens a hardware and software revenue stream that the Street consensus has not yet modeled. The downside scenario: large North American advertisers do not return in a meaningful way, eCPM (effective cost per thousand impressions) compression from scaling Sponsored Snaps inventory continues, and GAAP profitability slips past 2027. In that case, the stock likely retests its 52-week low of $3.81.

Conclusion

Watch North America’s large advertiser revenue at Q2 2026 earnings on August 5, 2026. A return to flat year-over-year in that segment would confirm that upfront commitment growth is flowing into actual spend and remove the central bear argument. Snap just proved it can manage costs. The remaining question is whether the revenue base that profitability scales on is actually recovering.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Snap?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Snap, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Snap alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!