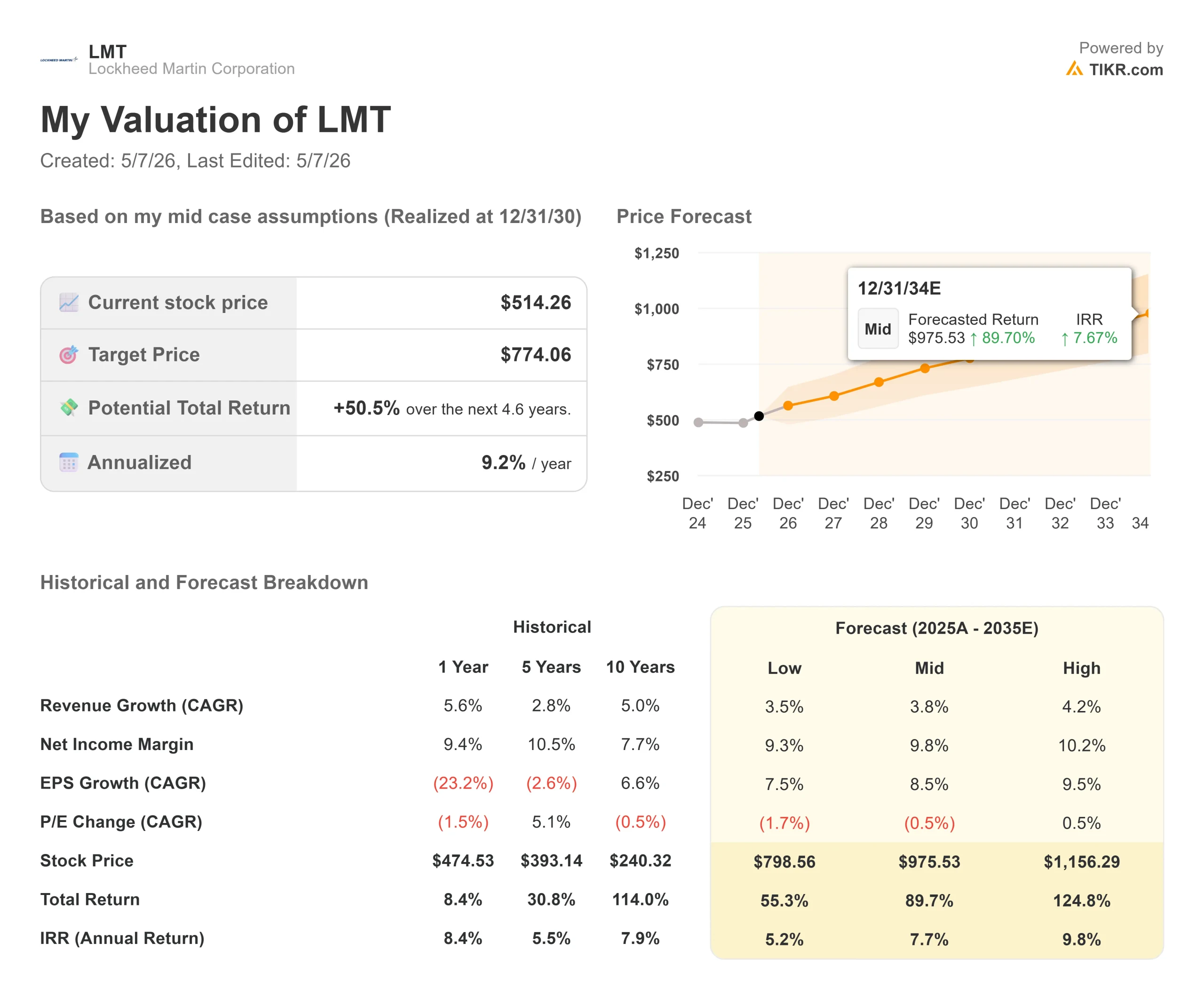

Key Stats for Lockheed Martin Stock

- Current Price: $508.25

- Target Price (Mid): ~$774

- Street Consensus Target: ~$638

- Potential Total Return: ~51%

- Annualized IRR: ~9% / year

- Earnings Reaction: -3.08% (April 23, 2026)

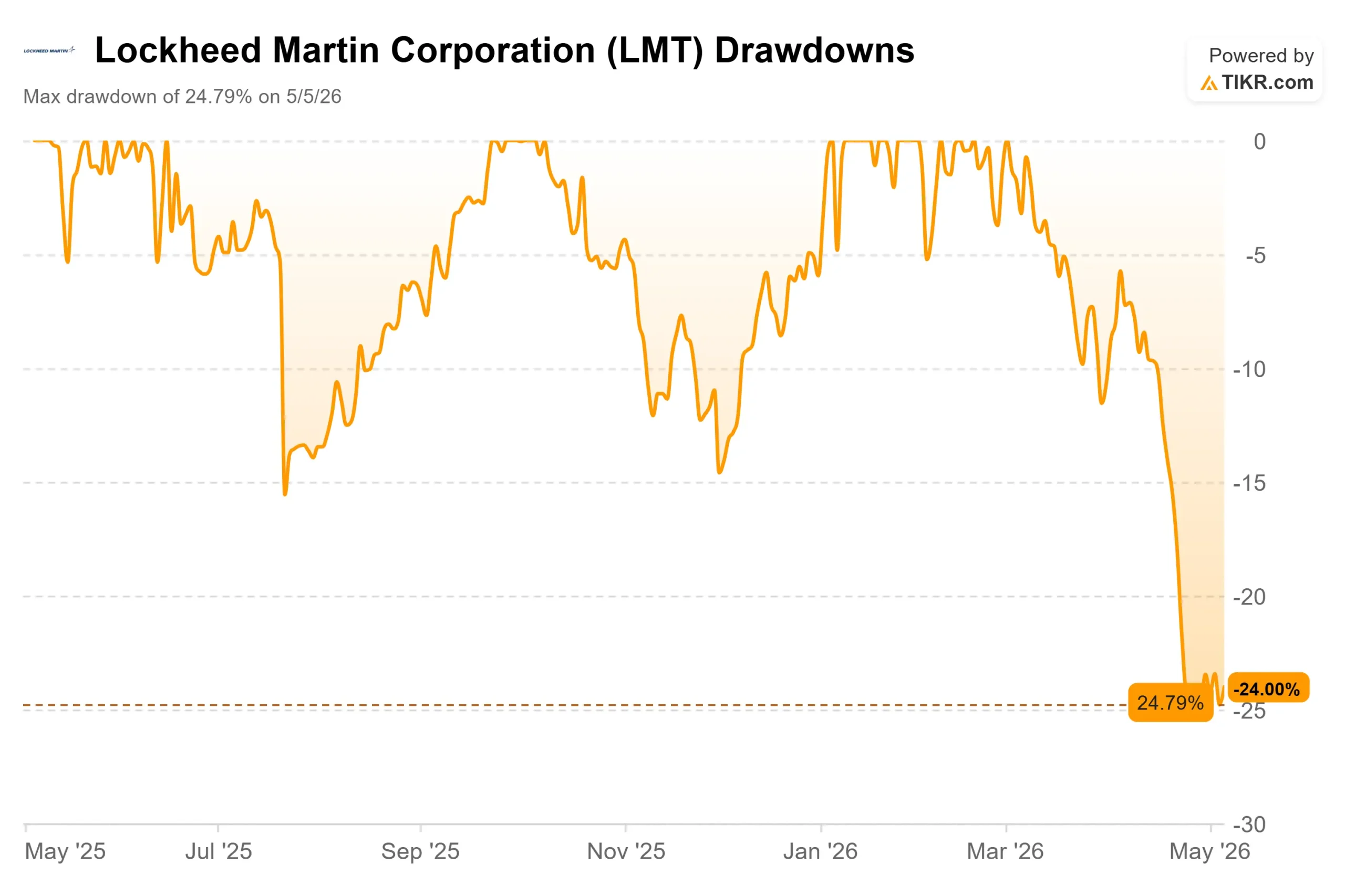

- Max Drawdown: -24.79% (May 5, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Defense investors are staring at a split screen. Lockheed Martin (LMT) hit a 52-week high of $692 earlier this year and has since dropped to around $508, a drawdown of 24.79% that bottomed on May 5. Bulls see a once-in-a-generation munitions ramp that the market is discounting too heavily. Bears point to negative free cash flow, fixed-price contract risk, and a leadership change at the company’s largest segment at exactly the wrong time.

The question is simple: Does the sell-off reflect the new reality, or is this a discount worth buying?

What Broke Down in Q1

On April 23, Lockheed reported Q1 2026 revenue of $18.021 billion, missing the $18.253 billion consensus by 1.3%. Adjusted EPS came in at $6.44 against an estimate of $6.73, a 4.3% miss. Free cash flow swung to ($291) million from $955 million a year earlier. The stock fell 3.08% that day and continued sliding to its max drawdown.

The source of the damage was Aeronautics, Lockheed’s largest segment with $30.6 billion in 2025 revenue. Segment operating profit fell 14% year-over-year, driven by two programs at once. The F-16 hit flight test rework issues on a new aircraft configuration being delivered to Taiwan and Morocco. The C-130 carried supply chain headwinds from 2025 into the quarter. CFO Evan Scott told analysts these one-time items across three business areas accounted for around $190 million of sales headwind and around $240 million of profit headwind. Strip those out, and the quarter was largely on track.

Analysts responded by cutting price targets. Morgan Stanley moved to $653. Bank of America cut to $600. RBC set a $575 ceiling. Susquehanna was the most constructive, trimming only to $700.Then, on May 6, Lockheed announced that Aeronautics president Greg Ulmer is retiring after more than 30 years. His successor is Orlando “OJ” Sanchez Jr., a former Air Force F-22 combat pilot who most recently led Skunk Works, Lockheed’s classified advanced development division. Sanchez takes over on June 1.

See historical and forward estimates for Lockheed Martin stock (It’s free!) >>>

Why the Demand Story Hasn’t Changed

The operational case for Lockheed’s products is stronger than the stock price implies.

Missiles and Fire Control (MFC), which covers air and missile defense and precision strike weapons, grew Q1 sales 8% year-over-year with operating profit up the same amount. Lockheed booked $7 billion in PAC-3 orders in Q1 alone: a $2.2 billion contract for 2026 deliveries and a $4.8 billion undefinitized contract to accelerate production. PAC-3 output is already up more than 60% from two years ago. The goal is to triple annual interceptor production from 650 to around 2,000 units over three to four years, with similar ramps underway for THAAD and PrSM (Precision Strike Missile).

The contract structure protecting these investments is unlike anything the defense industry has typically seen. CEO Jim Taiclet described seven-year government commitments with inflation-indexed escalators, advance government payments to keep the ramp cash flow neutral, and clawback provisions that protect Lockheed if volumes are later reduced: “if for whatever reason the government decides that the production rate won’t be as high in years 5, 6, whatever…there are kind of reach back or clawback mechanisms for making the company whole.”

On aircraft, demand is accelerating. The Pentagon’s FY2027 budget request includes 85 F-35s, nearly double the 47 procured in 2026. Israel approved two full combat squadrons of F-35 and F-15Ia aircraft. Lockheed also signed a $1.5 billion direct commercial sale of 12 F-16 Block 70 fighters to Peru, the first F-16 direct commercial sale in decades. Taiclet was direct about the F-35’s battlefield relevance, noting that U.S. and Israeli F-35s effectively negated Iran’s air defense network during Midnight Hammer operations this year.

Space grew Q1 sales 7% year-over-year. The Orion spacecraft carried four astronauts around the moon during NASA’s Artemis II mission in April, and Lockheed is already assembling capsules for Artemis III, IV, and V.

Full-year 2026 guidance remains intact: profit of $8.4 billion to $8.7 billion and free cash flow of $6.5 billion to $6.8 billion.

See how Lockheed Martin performs against its peers in TIKR (It’s free!) >>>

What the Valuation Shows

At $508, Lockheed trades at 16.89x next twelve months (NTM) earnings and 11.94x NTMEV/EBITDA, a discount to every major peer. RTX trades at 25.63x NTM P/E and 17.03x NTM EV/EBITDA. Northrop Grumman sits at 19.76x NTM P/E and 14.97x NTM EV/EBITDA. General Dynamics comes in at 20.63x NTM P/E and 14.68x NTM EV/EBITDA. Lockheed is the cheapest large-cap defense name on both metrics despite running the most direct exposure to the munitions ramp.

With trailing twelve months revenue of $75.1 billion and return on equity of 67.6%, the underlying business is not broken. The discount reflects Aeronautics execution risk and the classified program uncertainty. No charges were taken on either classified program in Q1, the first such clean quarter in several. Taiclet’s own words on the call: “I feel better about that program than I have probably since I got here 6 years ago.” Classified program cash burn is expected to run $500 million to $700 million per year in 2026 and 2027 before tapering, a bounded and disclosed headwind.

The Aeronautics leadership transition adds short-term uncertainty but carries strategic logic. Sanchez ran Skunk Works, where the classified programs originate. Putting him in charge of the segment containing those programs, as they enter a critical delivery phase, is a targeted fix rather than a general reshuffling.

TIKR Advanced Model Analysis

- Current Price: $508.25

- Target Price (Mid): ~$774

- Potential Total Return: ~51%

- Annualized IRR: ~9% / year

See analysts’ growth forecasts and price targets for Lockheed Martin stock (It’s free!) >>>

[GRAPH: TIKR Valuation Model LMT Price Forecast through 12/31/30]

The mid-case uses a revenue CAGR of around 4%, driven by MFC volume growth as PAC-3, THAAD, and PrSM ramp through the decade, and Aeronautics recovery as F-35 deliveries normalize and F-16 stabilizes. The margin driver is operating leverage on rising munitions volumes, with mid-case net income margins expanding toward around 10% from the current trailing level of 9.4%. The primary risk is a return of classified program charges, which would delay the margin recovery and keep the multiple depressed. At 11.94x forward EV/EBITDA with government clawback protections and inflation-indexed contracts, the downside appears more contained than the current price suggests.

Conclusion

The number to watch at Q2 earnings on July 21, 2026, is the Aeronautics segment operating margin. The segment ran between 10% and 10.5% margins from 2021 to 2023 based on TIKR data before slipping under execution pressure. A recovery back toward that historical range would confirm Q1’s headwinds were genuinely one-time and validate Sanchez’s appointment as the right fix. If margins stay depressed, the execution discount is earned. Lockheed Martin’s business is not broken. At $508, the stock is priced as it might be.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Lockheed Martin?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Lockheed Martin, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Lockheed Martin alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Lockheed Martin on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!