Key Stats for Intuit Stock

- 52-Week Range: $340.11 to $656.08

- Current Price: $388.55

- TIKR Target Price (Mid): ~$710

- TIKR Annualized IRR (Mid): ~15% per year

- Street Mean Target: ~$590 (Buy, 34 analysts)

- Next Earnings: 5/22/26

Value your favorite stocks like Intuit with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

The Market Is Worried About AI. The Numbers Tell a Different Story

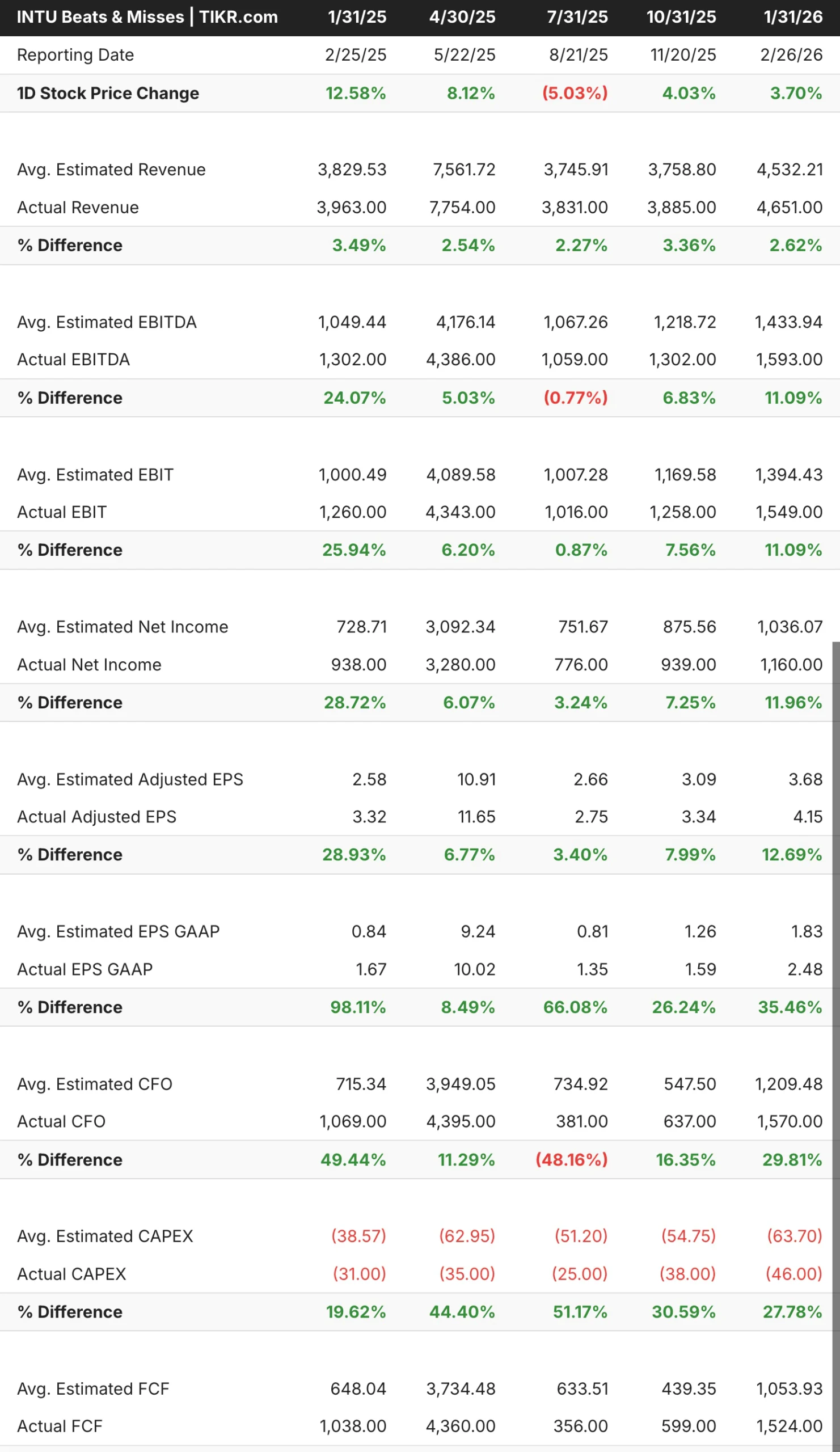

If you just looked at the stock, you might think something had gone seriously wrong at Intuit (INTU). It hasn’t. The company behind TurboTax, QuickBooks, Credit Karma, and Mailchimp has beaten revenue estimates in each of the last five quarters, reaffirmed its full-year guidance, and won a meaningful legal battle against the FTC in March over its TurboTax advertising practices.

What the market is wrestling with is a harder question about the future. If AI makes tax preparation cheap or free, what happens to TurboTax? If small business accounting gets automated, what happens to QuickBooks? Those are legitimate concerns, but they are not showing up in the results yet.

The beats have been consistent and, in some cases, pretty wide. Q1 fiscal 2026 EBITDA came in roughly 24% above what analysts were modeling, which is a meaningful gap for a business of this size. Revenue has beaten in every quarter shown in the table, which is not the pattern of a company losing ground to disruption.

See analysts’ growth forecasts and price targets for INTU stock (It’s free!) >>>

Revenue Has Nearly Doubled Since 2021. Margins Have Held Up

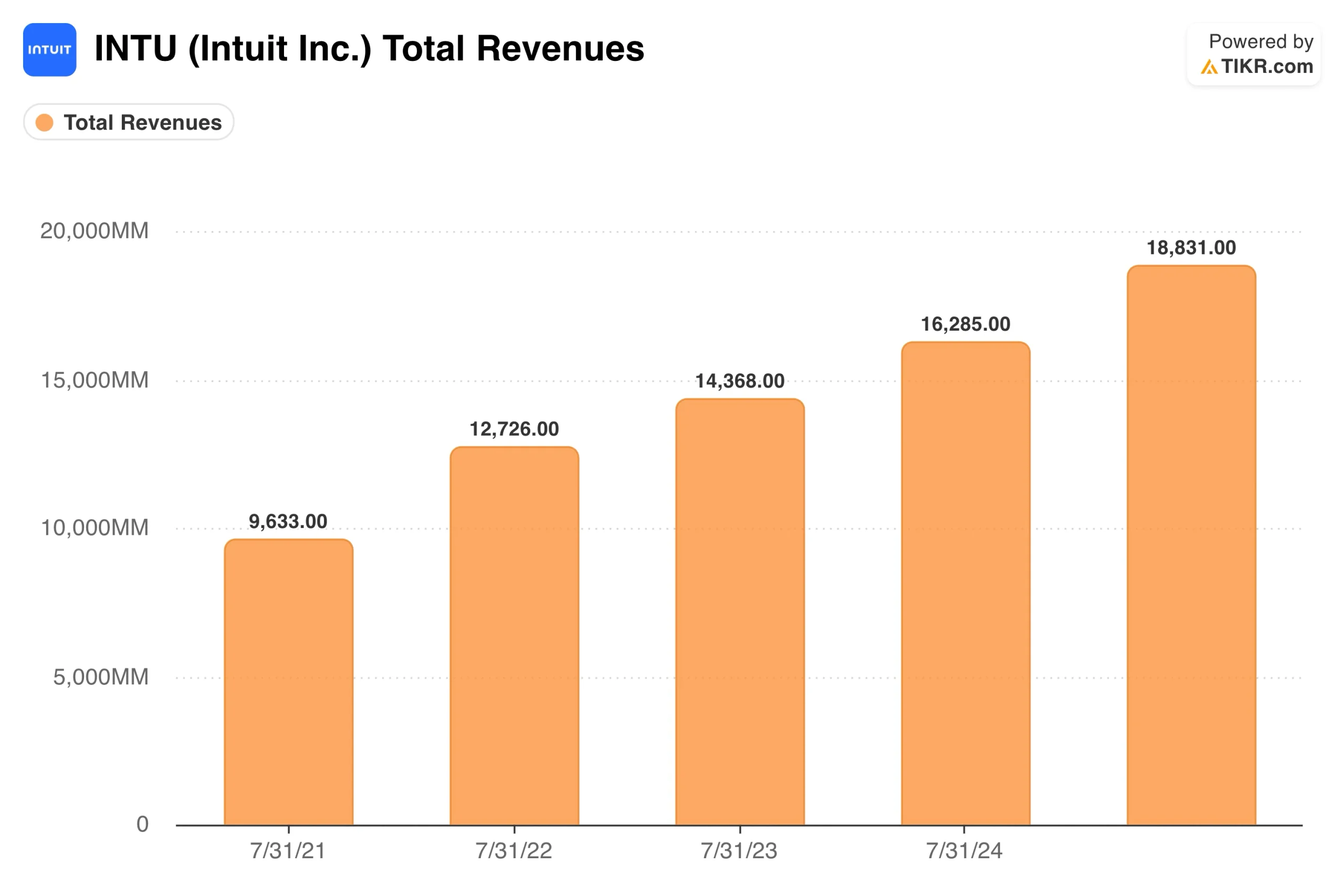

Intuit grew from $9.6 billion in revenue in fiscal 2021 to $18.8 billion in fiscal 2024, nearly doubling in four years while maintaining net income margins in the 28%-30% range. That combination of growth and profitability is what earns the company its premium multiple and why analysts have been reluctant to downgrade it even as the stock has sold off.

The forward model assumes around 11%-13% annual growth, which is slightly below what Intuit has historically delivered. The conservatism is mostly about Mailchimp, which has been the weakest part of the portfolio since the acquisition, and some uncertainty around how fast mid-market businesses adopt the Intuit Enterprise Suite. The mid-market opportunity is real, with QBO Advanced growing around 40%, but it is still early.

Value Intuit instantly (Free with TIKR) >>>

83% Upside in the Mid Case, With Real Risks Worth Understanding

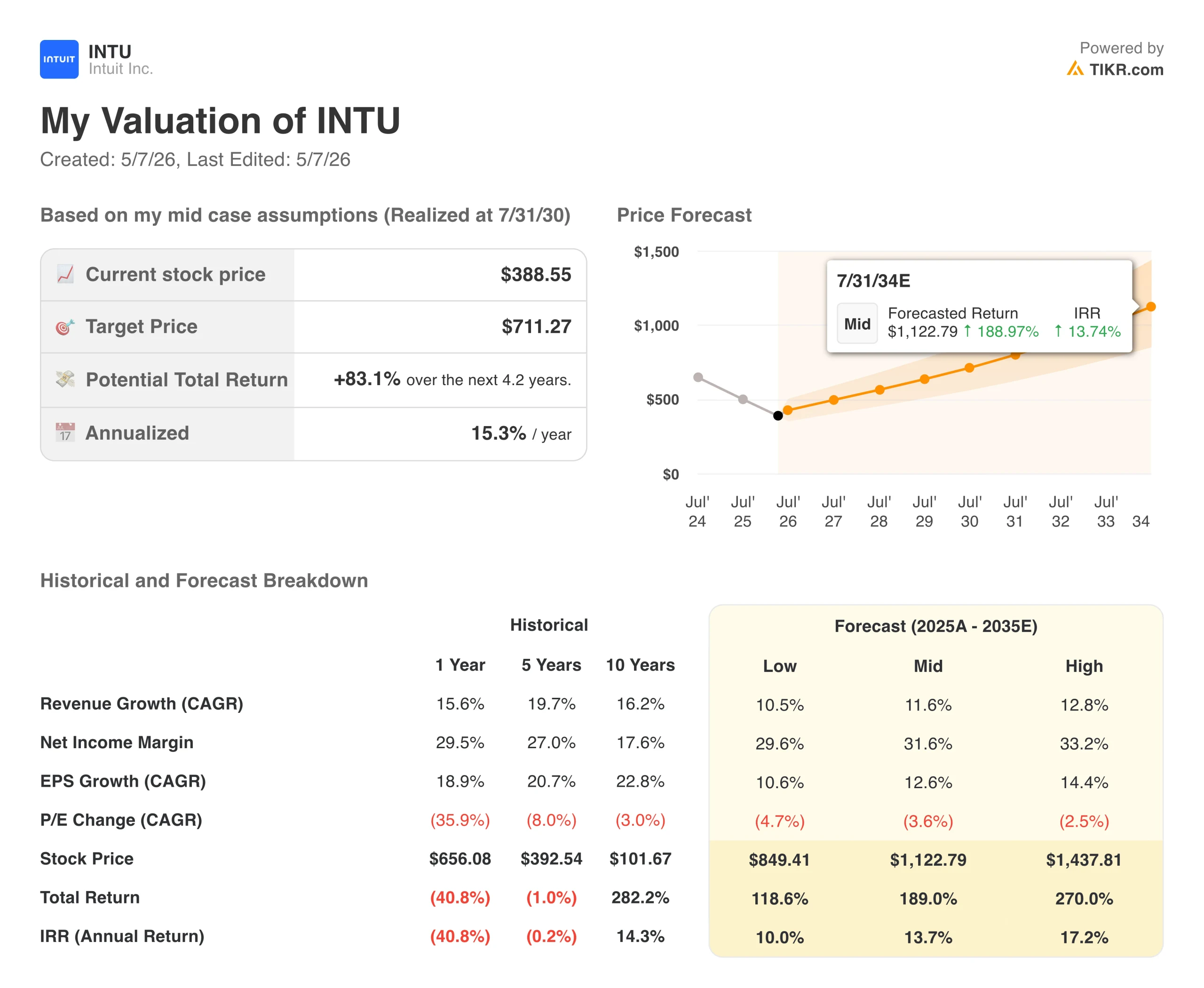

TIKR’s model targets around $710 in the mid case, which works out to roughly 83% total return over about 4.2 years, or around 15% annualized. That return is driven by around 12% annual revenue growth and net income margins that are gradually expanding into the low- to mid-30s as the business scales.

The AI debate around Intuit is genuinely two-sided, and it is worth carefully considering both sides before forming a view.

- Bulls: The most important point is that Intuit is not sitting still on AI. TurboTax Live, which pairs AI tools with human tax experts, grew revenue by around 51% last fiscal year, suggesting customers are willing to pay more for an assisted experience rather than less. The OpenAI partnership gives Intuit a customer acquisition channel through ChatGPT without revenue sharing. And the Intuit Enterprise Suite is posting strong early traction in the mid-market, where businesses are consolidating from 25 to 30 separate tools onto a single platform. With 29 Buy ratings and no Sells on the Street, the consensus view is that the current price is a mispricing rather than a warning sign.

- Bears: The bear case has a cleaner argument than it sometimes gets credit for. A government-sponsored free tax filing program would directly threaten the highest-margin product in Intuit’s portfolio. Mailchimp has not returned to double-digit growth since the acquisition and represents a real drag on the overall numbers. And while the stock has de-rated, it still trades at around 27 times forward earnings, which means there isn’t much cushion if revenue growth disappoints relative to the model’s requirements.

Should You Invest in Intuit?

The core question with Intuit is whether the AI disruption risk is structural or overstated. The results so far suggest the latter, but the market is asking for more proof before it re-rates the stock.

The next earnings report on May 22nd is the most important near-term data point. TurboTax filing season results will tell you how the consumer business held up, and Credit Karma’s trajectory will tell you whether the financial services cross-sell is gaining real traction. Those two numbers will do more to shape the next leg of this story than any price target will.

See analysts’ growth forecasts and price targets for Intuit stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!