Key Stats

- Current Price: $433 (May 7, 2026)

- Q1 2026 Revenue: $2.71B, up 7% YoY

- Q1 2026 Non-GAAP EPS: $3.37, up 6% YoY

- Q1 2026 Orders: Record Q1 orders, up 38% YoY

- Q1 2026 Ending Backlog: $15.7B, up 11% YoY

- Full-Year 2026 Revenue Guidance: ~$12.8B (raised from $12.7B)

- Full-Year 2026 Non-GAAP EPS Guidance: $16.87 to $16.99 (raised from $16.7 to $16.85)

- TIKR Model Price Target: $602

- Implied Upside: ~39%

Motorola Stock Beats Q1 Estimates on Record Orders and Raised Guidance

Motorola stock (MSI) delivered record Q1 revenue of $2.71B, up 7% year over year, with non-GAAP EPS of $3.37 beating the prior-year quarter’s $3.18 by 6%.

Software and Services drove the headline, with segment revenue up 18% versus the prior-year quarter, according to CFO Jason Winkler on the Q1 2026 earnings call.

Segment operating earnings in Software and Services reached $395M, with operating margin expanding to 34.2% from 28.7% in Q1 2025, driven by favorable mix and improved operating leverage, according to Winkler.

Products and SI revenue grew 1% year over year, with $181M from acquisitions and $30M in foreign currency tailwinds included in the quarter.

Products and SI operating margin contracted to 24.8% from 28.1% in Q1 2025, weighed down by unfavorable mix and higher supply chain costs.

Orders grew 38% in Q1, producing a record ending backlog of $15.7B, up 11% from $14.1B a year ago, marking the fourth consecutive quarter of double-digit orders growth in both segments.

CEO Greg Brown cited continued investment in Silvus as a meaningful growth driver, noting the business is expected to generate $750M in full-year revenue, raised $75M from prior guidance, according to Brown on the Q1 2026 earnings call.

Command Center technology grew 27% in Q1, driven by Tier 1 city activations for next-generation 911, while Video grew 16%, led by body-worn cameras, ALPR, and the cloud-based Alta platform, according to Winkler.

The company faces $60M in tariff headwinds concentrated in the first half of 2026, and memory costs are expected to more than double to over $100M this year, though management maintained its full-year target of 100 basis points of operating margin expansion, according to Winkler.

Capital allocation in Q1 included $201M in dividends, $118M in share repurchases, and the closure of Exacom and Hyper acquisitions for a combined $90M net of cash.

For Q2, management guided to approximately 8.5% sales growth and non-GAAP EPS of $3.82 to $3.88.

Full-year non-GAAP EPS guidance was raised to $16.87 to $16.99, up from the prior range of $16.70 to $16.85.

Motorola Solutions Stock: What the Income Statement Shows

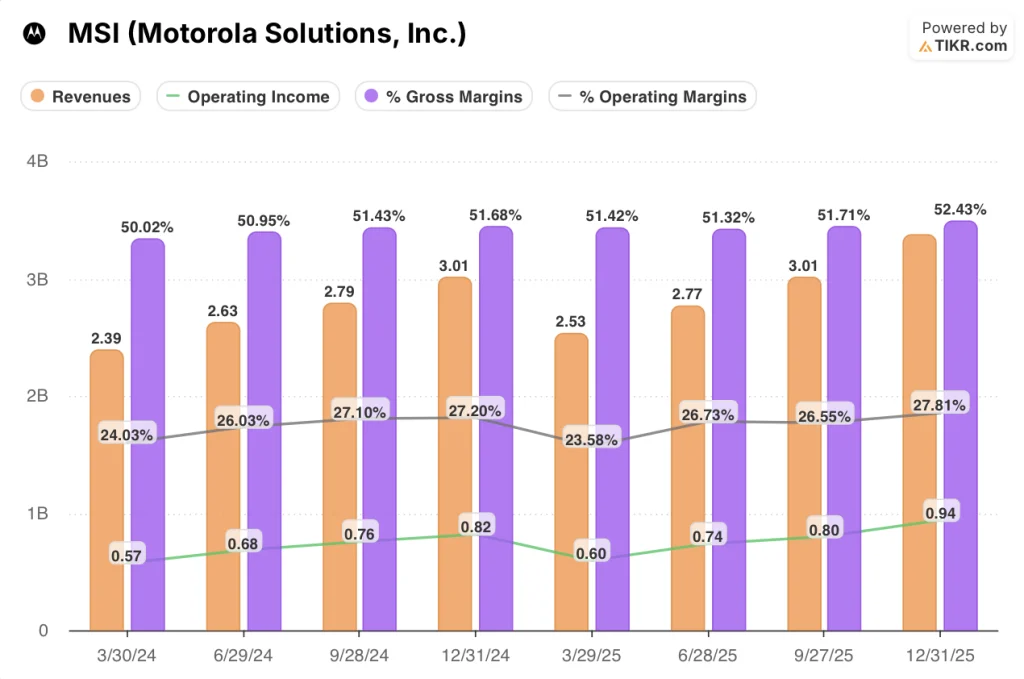

Motorola stock is executing a steady margin expansion story, with operating income growing year over year across each of the last eight quarters visible in the income statement despite elevated cost pressures.

Revenue growth has ranged from 5.2% to 12.3% YoY across the eight quarters shown, putting Q1 2026’s 7% growth squarely within the established band rather than signaling any deceleration.

Gross margin has held in a tight band, moving from 50.0% in Q1 2024 to 51.4% in Q1 2025, reflecting consistent cost management through the period.

Operating margin in Q1 2025 compressed to 23.6%, the lowest point across the eight quarters shown, before recovering to 26.7% in Q2 2025, 26.6% in Q3 2025, and 27.8% in Q4 2025.

Operating income followed the same arc, rising from $600M in Q1 2025 to $940M in Q4 2025.

Non-GAAP operating income for Q1 2026 reached $781M, up 9% from the year-ago quarter, with non-GAAP operating margin of 28.8%, up 50 basis points, according to Winkler on the Q1 2026 earnings call.

Winkler also confirmed the 50-basis-point operating margin expansion in Q1 was achieved despite higher supply chain costs, and that management continues to project 100 basis points of full-year operating margin expansion with contribution from both segments.

What Does the Valuation Model Say?

The TIKR model prices MSI stock at a target of $602, implying approximately 39% total return potential from the current price of $433 over the next 4.6 years, with an annualized return of 7.3%.

The mid-case assumptions build in a revenue CAGR of 4.8% and a net income margin of 23.1%, with EPS growing at a 5.3% CAGR through 2035.

The Q1 results improve the near-term risk/reward picture: a record backlog, two raised guidance lines, and a fifth consecutive quarter of operating margin expansion all reduce the probability of the low-case scenario playing out.

At current prices, the TIKR model suggests Motorola Solutions stock is offering a below-market annualized return in the mid case, meaning the investment thesis depends on execution against the high-case assumptions rather than simply maintaining current trajectory.

The investment question for Motorola Solutions stock is whether the Silvus-driven demand surge and Software and Services momentum are durable enough to support the high-case scenario, or whether rising memory costs and post-acquisition integration drag anchor returns near the mid case.

Growth Case

- Software and Services revenue grew 18% in Q1 2026, with management noting the segment is the proxy for recurring revenue; sustained growth here directly lifts the net income margin assumption in the model toward the 24% high-case figure

- Silvus revenue guidance raised to $750M for full-year 2026, up from $675M, with EBITDA margins running near 45%, according to Brown on the Q1 2026 earnings call

- Record Q1 orders up 38% and a $15.7B ending backlog, up 11% year over year, give multi-quarter revenue visibility well beyond what the income statement currently captures

- Command Center growing 27% in Q1 and Video growing 16% suggest both technologies are accelerating, broadening the growth profile beyond any single segment

Margin Case

- Memory costs expected to more than double in 2026 to over $100M, with management pursuing mitigation strategies that include “surgical price adjustments,” a signal that full cost recovery is not guaranteed

- Products and SI operating margin fell to 24.8% in Q1 2026 from 28.1% a year ago, driven by unfavorable mix and higher supply chain costs, and this segment’s margin drag could limit the 100-basis-point full-year expansion to back-half reliance

- GAAP EPS fell to $2.18 in Q1 2026 from $2.53 in Q1 2025, driven by a $75M noncash Silvus earnout charge, with the earnout now expected to pay out just over $100M total, adding a known near-term earnings headwind

- The TIKR model’s mid-case IRR of 5.9% per year through 2030 sits below the historical 10-year IRR of 19.9%, meaning the model is already pricing in a significant deceleration from Motorola Solutions stock’s historical compounding rate

Should You Invest in Motorola Solutions, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Motorola Solutions stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Motorola Solutions, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze MSI stock on TIKR for Free →