Key Takeaways:

- Pinterest beat Q1 2026 revenue estimates, reporting $1.01B versus the $966M consensus estimate.

- Revenue grew 18% year-over-year, and management guided Q2 revenue above analyst expectations.

- Elliott Management committed a $1B strategic investment, and Pinterest announced $2B in near-term share repurchases.

- PINS trades at around $22, down about 19% year-to-date, with a 52-week range of $14 to $40.

- Street analysts carry a consensus price target of around $28 per share.

What Happened?

Pinterest (PINS) delivered a standout first quarter in fiscal 2026. Revenue grew 18% year-over-year to $1.01B, beating the $966M analyst consensus by around 4%. The company swung to a $74M net loss, but non-cash items drove most of that figure. Management also guided Q2 revenue above analyst expectations, and investor sentiment improved materially.

The March 2026 announcement was even more significant for the longer-term setup. Elliott Management is an influential activist fund known for driving shareholder value creation. The fund committed a $1B strategic investment in Pinterest. The company followed that move with a $2B share repurchase program, signaling strong institutional confidence in the platform.

The digital advertising market remained resilient through Q1 2026. Pinterest’s high-intent user base continued drawing ad spend because purchase-minded browsing attracts performance advertisers. So Pinterest is capturing a specific advertiser segment that values conversion-focused targeting. Q2 guidance confirmed that advertisers are still spending actively on the platform.

Here’s why Pinterest stock could deliver meaningful returns through 2028 as it scales ad monetization and executes its buyback program.

What the Model Says for PINS Stock

We analyzed the upside potential for Pinterest stock based on its expanding digital advertising revenue, growing global user base, and improving platform monetization through shoppable content and AI-powered ad tools.

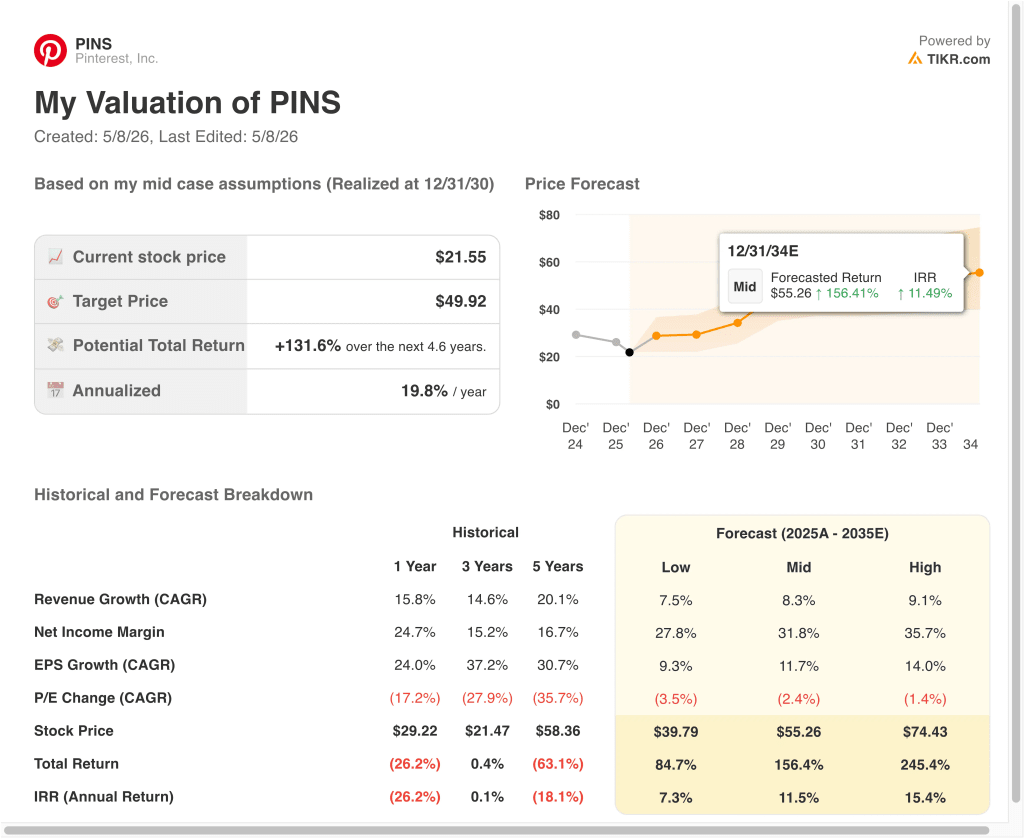

Based on estimates of around 13% annual revenue growth, around 10% operating margins, and a normalized P/E multiple of 11.4x, the model projects Pinterest stock could rise from $22 to $31 per share.

That would be a 42% total return, or a 14% annualized return over the next 2.6 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for PINS stock:

1. Revenue Growth: 13%

Pinterest delivered 18% revenue growth in Q1 2026, well above the consensus estimate. The platform’s advertiser base grew steadily, and newer ad formats around shopping and video are drawing larger advertiser budgets.

Elliott’s $1B investment and the $2B buyback program reflect institutional conviction in continued revenue momentum. The global rollout of shoppable pins and AI-powered ad personalization tools should also support further revenue expansion.

Based on analysts’ consensus estimates, we used around 13% annual revenue growth. This reflects a moderate normalization from the recent 18% pace while recognizing the platform’s strong advertiser momentum and growing international reach.

2. Operating Margins: 10%

Pinterest’s last 12-month gross margin stands at 79.9%, but the EBIT margin sits at 7.4%. The gap reflects meaningful ongoing investment in product development, marketing, and platform infrastructure.

But management has demonstrated improving profitability trends recently. Elliott’s presence typically drives stronger cost discipline and shareholder-return focus across portfolio companies.

Based on analysts’ consensus estimates, we used around 10% operating margins. This reflects a gradual improvement from the current 7.4% EBIT level, supported by operating leverage as revenue scales and investment intensity moderates.

3. Exit P/E Multiple: 11.4x

Pinterest currently trades at an NTM P/E of 11.4x, which is modest compared to many digital advertising platforms. This discount reflects near-term market skepticism about the pace of the company’s profitability ramp.

But the 79.9% gross margin and accelerating revenue growth suggest real monetization power. And Elliott’s involvement often acts as a catalyst for multiple expansions over time.

Based on analysts’ consensus estimates, we maintained an exit P/E of 11.4x. This is a conservative multiple consistent with Pinterest’s earlier stage of margin development and its current valuation level.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for PINS stock through 2034 show varied outcomes based on advertising revenue growth and operating margin execution (these are estimates, not guaranteed returns):

- Low Case: Ad spending softens and margin improvement stalls → 7% annual returns

- Mid Case: Ad monetization scales steadily and buybacks support per-share value → 12% annual returns

- High Case: AI-powered ad tools drive rapid revenue growth and margins expand ahead of plan → 15% annual returns

Going forward, Pinterest’s trajectory depends heavily on advertising market conditions and the pace of operating leverage improvement. The Elliott investment provides both financial backing and governance pressure to execute on the platform’s potential. But investors should monitor user growth, ad revenue per user, and quarterly margin trends closely before drawing longer-term conclusions.

See what analysts think about PINS stock right now (Free with TIKR) >>>

Should You Invest in Pinterest?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up PINS, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track PINS alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Pinterest stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!