Key Stats for Pool Corporation Stock

- 52-Week Range: $170.88 to $301.92

- Current Price: $190.44

- TIKR Target Price (Mid): ~$276

- TIKR Annualized IRR (Mid): ~8% per year

- Full Year 2026 EPS Guidance: $10.87 to $11.17

Value your favorite stocks like POOL with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

A Quiet Beat in a Business Most Investors Have Written Off

Pool Corporation (POOL) is the largest wholesale distributor of swimming pool supplies in the United States, serving roughly 125,000 wholesale customers through a network of over 400 sales centers. It’s important to clarify that Pool does not actually build pools, it distributes the chemicals, equipment, and building materials that keep the country’s six million in-ground pools running year after year.

That distinction matters a lot right now as new pool construction has been stuck near 58,000 units annually, well below the peak of 75,000 to 100,000 units the industry was doing in better years.

But the maintenance side of the business is far less sensitive to housing market cycles, and that is what has kept Pool’s results more resilient than the stock price would suggest.

The Q1 2026 results were the cleanest quarter Pool has had in several periods. Revenue came in at $1.14 billion, up 6% year over year and about 4% above what analysts were expecting. Non-GAAP EPS of $1.43 beat consensus by around 6%, and EBITDA of $101 million came in ahead of the $98 million estimate.

CEO Peter Arvan acknowledged the difficult consumer environment on the call but confirmed full-year 2026 EPS guidance of $10.87 to $11.17 per diluted share, which was notable given how cautious the setup had been heading into the print.

See analysts’ growth forecasts and price targets for POOL stock (It’s free!) >>>

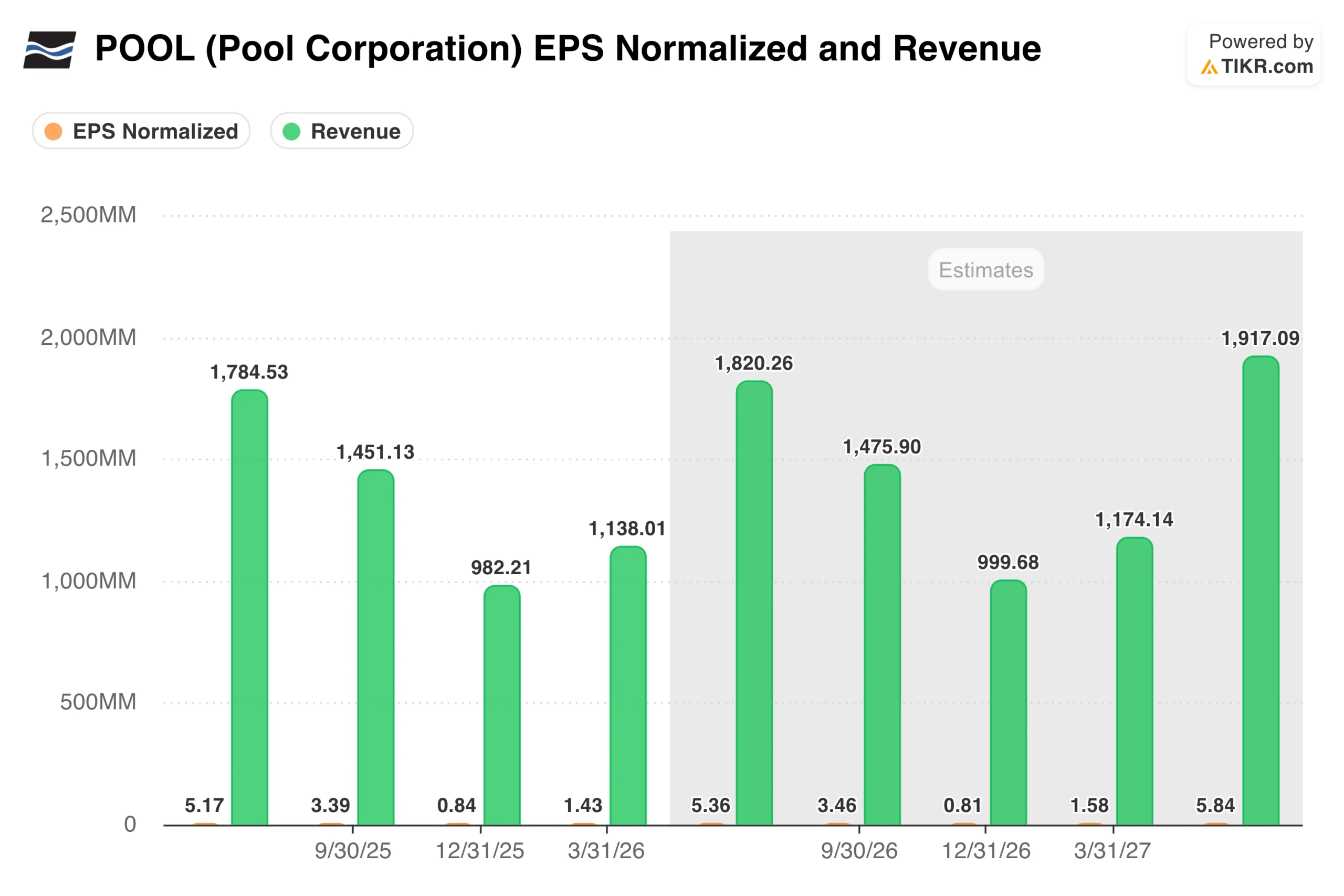

What the Seasonal Revenue Pattern Tells You About This Business

The EPS and revenue chart makes something immediately clear about Pool that gets overlooked in a single-quarter snapshot: this is one of the most seasonal businesses in the market.

The June quarter generates more earnings than the other three quarters combined, because that is when pool season peaks across the Sun Belt and the rest of the country. Understanding that rhythm is essential before drawing any conclusions from a single quarterly print.

What the chart also shows is that consensus is modeling a modest step-up from last year. Analysts estimate Q2 2026 revenue of around $1.82 billion against $1.78 billion a year prior, and full-year EPS in the $11 range. That is not an exciting growth story, but it is a stable one, and at the current valuation, it may not need to be exciting to generate a reasonable return.

Pool360, the company’s digital B2B ordering platform, is worth keeping an eye on as a margin driver. It now represents about 13% of total net sales, up from 12.5% a year ago, and the shift toward higher-margin private-label chemicals is gradually improving the quality of earnings even as volumes remain relatively flat.

Value POOL instantly (Free with TIKR) >>>

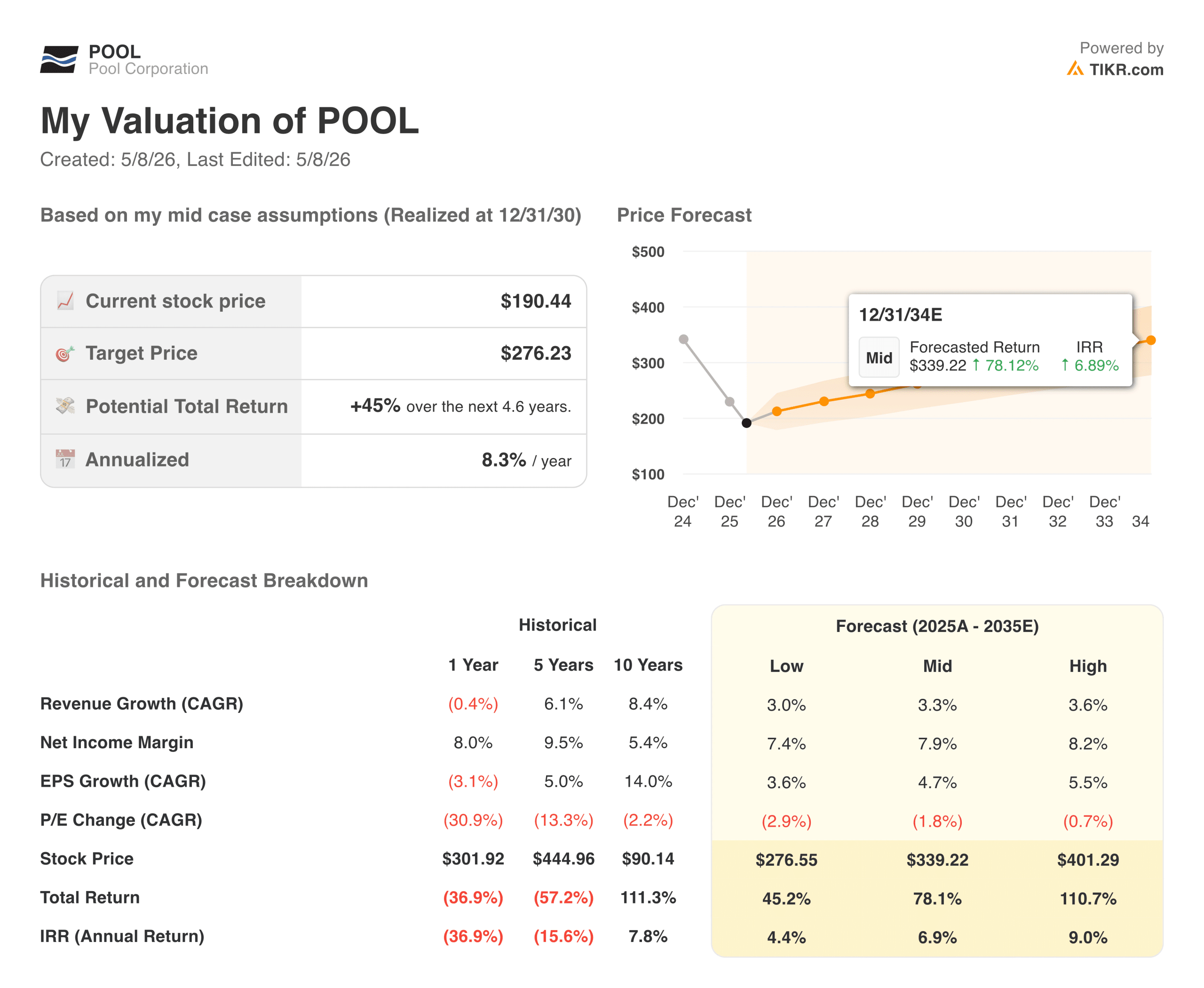

Modest Upside in the Base Case, but the Setup Is Better Than It Looks

TIKR’s model targets around $276 in the mid case, implying a total return of about 45% from current levels over roughly 4.6 years, or about 8% annualized. The model assumes revenue growth of around 3% annually and net income margins recovering gradually toward 8%. Neither number requires a heroic assumption.

The bull and bear cases here are really just two versions of the same question: how quickly does the housing market recover, and what does new pool construction look like on the other side of it.

Bulls: What Has to Go Right

- Housing eventually normalizes. New pool construction has been running near 58,000 units annually, well below the historical peak of 75,000 to 100,000 units. Pool does not need a full recovery to benefit. Even a gradual move back toward 65,000 to 70,000 units would add meaningful volume to a distribution network that is already built and largely fixed-cost. When that inflection comes, earnings leverage will be significant.

- The maintenance business keeps the floor in place. Roughly 80% of Pool’s revenue comes from the existing installed base of pools that need chemicals, equipment, and service every year, regardless of what mortgage rates do. That recurring demand cushions earnings during slow construction cycles and gives management the visibility to guide with confidence even in a difficult environment.

- Private label and Pool360 are quietly improving margins. The shift toward higher-margin private-label chemicals is underway in the background without much fanfare, and Pool360, the company’s digital B2B ordering platform, has grown to about 13% of total net sales. Neither is a headline catalyst, but both are improving the quality of earnings over time in ways that compound.

- The valuation is the most attractive it has been in years. At around $190, the stock is trading near a decade-low multiple. Investors are pricing in a prolonged construction downturn, which means even a modest improvement in the macro backdrop could drive a meaningful re-rating without requiring the underlying business to do anything extraordinary.

Bears: What Could Keep the Stock Rangebound

- New construction may stay depressed longer than expected. With mortgage rates still elevated and housing turnover subdued, there is no obvious near-term catalyst to push new pool builds materially above current levels. The model’s 3% revenue growth assumption is achievable, but it leaves very little cushion if discretionary remodeling spend weakens further alongside a softer consumer.

- The debt load limits flexibility. Pool took on meaningful leverage during its acquisition years, and while the business generates enough cash to service it comfortably, the balance sheet does reduce the company’s ability to be aggressive on buybacks or acquisitions if conditions deteriorate.

- Discretionary categories remain soft. While demand for maintenance is resilient, the higher-ticket remodeling and equipment-replacement categories are more sensitive to consumer confidence. If the macro environment weakens further, those categories are the first to see pullbacks, and they carry above-average margins.

- The re-rating requires patience, the market may not have. The bull case here is fundamentally a waiting game, and the catalyst, a housing recovery, is entirely outside of management’s control. Investors who buy today need to be comfortable holding through a period when results are steady but unspectacular, with no clear timeline for when the bigger growth story resumes.

Should You Invest in Pool Corporation

Pool is not a story about what is happening this year. It is a story about what happens when housing eventually normalizes and new construction returns to historical levels. If you believe that is a matter of when rather than if, the current price at around $190 is offering a reasonably attractive entry point into a business with durable competitive advantages and a 25-year track record of compounding.

The near-term setup is actually more constructive than it has been in several quarters. The Q1 beat was clean, guidance was confirmed, and the maintenance business is holding up. The patience required here is measured in years, not quarters, but that is precisely the kind of setup that tends to reward investors who are willing to look past the noise.

See analysts’ growth forecasts and price targets for POOL stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!