Key Takeaways:

- Adobe is a mature, highly profitable software company powering Photoshop, Illustrator, and digital marketing platforms worldwide. Atlassian builds project management and collaboration tools like Jira and Confluence, used daily by software development teams at some of the world’s largest companies.

- Both companies run on recurring subscription revenue with strong customer retention, making them reliable, long-term software businesses.

- Analysts expect both companies to maintain strong free cash flow (FCF) generation, with Adobe growing revenues around 9% annually and holding operating margins near 37%, while Atlassian is expected to grow revenues around 20% per year as FCF margins improve steadily.

- Based on our valuation assumptions, Adobe stock could rise from $257 to around $337 per share by late 2028, which represents a 31.6% total return or 11.3% annualized. Atlassian could climb from $92 to around $123 by mid-2028, and that would be a 33.1% total return or 14.2% annualized, giving it the edge on projected annual returns.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

What’s Happening?

Adobe Inc. (ADBE) makes the software tools that creative professionals rely on daily. Photoshop, Illustrator, Premiere Pro, and Acrobat are core Adobe products used by millions worldwide. Adobe also runs a rapidly growing digital marketing platform called Adobe Experience Cloud. It generates revenue through subscriptions, so its cash flows are highly predictable and recurring.

Atlassian Corporation (TEAM) builds the tools that software engineering teams use to get work done. Jira tracks bugs and project tasks, while Confluence serves as a shared knowledge base for teams.

Both products are deeply embedded in the workflows of many of the world’s largest companies. Atlassian recently launched AI agents inside Jira and is expanding its Rovo AI platform for enterprise customers.

Both stocks have fallen sharply in 2025 and 2026 despite strong underlying business performance. Adobe beat its Q1 FY26 revenue estimate with $6.4B in sales and announced a new $25B share buyback program. Atlassian grew revenue 32% in its latest quarter and lifted its annual growth target to around 24%.

Here’s why both of these selloffs may have created an opportunity for patient investors.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Adobe Is Highly Profitable, but Atlassian Is Catching Up Fast

Adobe grew from around $15.8B in revenue in fiscal 2021 to around $23.8B by fiscal 2025. But what is even more impressive is that operating margins stayed near 37% throughout that entire span. FCF also grew from around $6.9B to around $9.9B over those four years. So Adobe has compounded both revenue and profit at scale, which is a rare combination.

Atlassian has grown even faster, with revenue climbing from $1.85B in fiscal 2021 to $4.93B in fiscal 2025. That is a roughly 167% increase over four years, driven by cloud migrations and new product adoption.

However, Atlassian’s reported GAAP operating margins have stayed slightly negative throughout this growth phase. In fiscal 2025, its GAAP operating loss margin was 2.5%, reflecting heavy AI and enterprise investments.

Atlassian’s free cash flow, however, tells a different story than its GAAP operating loss. FCF reached $1.4B in fiscal 2025, so the business is clearly generating real cash. But Adobe’s FCF is far stronger, at nearly $9.9B on $23.8B in revenue. Both companies convert meaningful revenue into cash, but Adobe’s advantage here is substantial.

Looking ahead, Adobe’s operating margins are expected to stay near 37% while FCF continues expanding. Atlassian’s investment phase should begin paying off as the company moves toward meaningful GAAP profitability.

Consensus estimates point to around 20% annual revenue growth for Atlassian, which would push its margin profile significantly higher. Yet Adobe’s more modest 9% annual revenue growth comes with far superior margins today.

See what analysts think about ADBE and TEAM stock right now (Free with TIKR) >>>

The Selloff Has Pushed Both Stocks to Their Cheapest Valuations in Years

Adobe’s forward P/E (price to earnings) multiple now sits at around 10.7x as of early May 2026. That is a dramatic drop from 21.5x in February 2025, and it reflects how far investor sentiment has shifted.

Adobe’s EV to EBITDA multiple, which measures a company’s value relative to its operating profit, also fell from 16.2x to just 8.2x. So for a company running near 37% operating margins, these multiples reflect significant market skepticism.

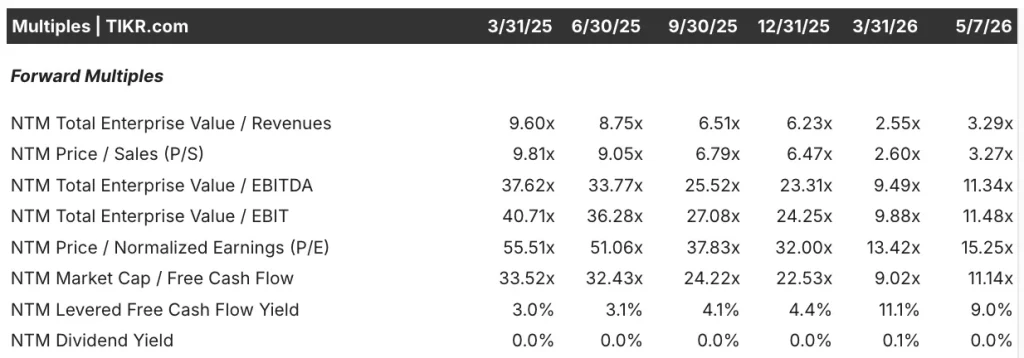

But Atlassian’s multiple compressions have been even more dramatic. In March 2025, its forward P/E stood at 55.5x, and its forward EV to EBITDA was 37.6x. Both metrics have now collapsed to roughly 15.3x and 11.3x, respectively, as of early May 2026. And yet Atlassian keeps beating revenue estimates quarter after quarter.

Also, the FCF yields on both stocks now look compelling for investors seeking income. Adobe’s forward FCF yield is around 9.9%, and Atlassian’s is around 9.0%. Both figures suggest, however, that the market is now pricing these businesses like slower, more mature companies. So the multiple compression may have gone further than the underlying fundamentals actually justify.

Atlassian’s forward EV to revenue has also dropped, from 9.6x in March 2025 to just 3.3x today. Adobe’s multiple fell from 8.0x to 3.9x, and that is a significant rerating for a company of its scale.

So both companies now trade at revenue multiples that are more aligned with their expected growth rates. And that makes current valuation levels look more reasonable than they have in years.

See analysts’ full growth forecasts and estimates for ADBE and TEAM stock (It’s free) >>>

The Valuation Models Point to Meaningful Returns for Both Stocks

We analyzed the upside potential for Adobe stock based on its AI momentum, subscription model durability, and ongoing expansion into digital marketing and experience tools.

Based on estimates of around 9% annual revenue growth, 44.5% operating margins, and a normalized P/E of around 10.7x, the model projects Adobe stock could rise from $257 to around $337 per share.

And that would be a 31.6% total return, or an 11.3% annualized return over the next 2.6 years.

We analyzed the upside potential for Atlassian stock based on its ongoing cloud transition, enterprise AI platform investments through Rovo and Jira agents, and strong revenue growth momentum.

Based on estimates of around 19% annual revenue growth, around 29% operating margins, and a normalized P/E of around 15.3x, the model projects Atlassian stock could rise from $92 to around $123 per share.

So that would be a 33.1% total return, or a 14.2% annualized return over the next 2.1 years.

Based on analysts’ consensus estimates, we see Atlassian offering higher potential annualized returns than Adobe. But the difference is 14.2% per year for Atlassian versus 11.3% for Adobe.

Adobe’s model leans on high margins and steady cash generation but assumes slower growth. Atlassian’s higher return potential comes with more execution risk and dependency on significant margin expansion.

Build your own Valuation Model to value any stock (It’s free!) >>>

Which One Do You Actually Buy?

Both companies are classic SaaS businesses with highly recurring revenue and strong customer retention. But Adobe’s edge is its margin profile. It generates around $9.9B in free cash flow annually and is actively repurchasing shares. Atlassian is growing much faster but has yet to deliver consistent GAAP profitability, which adds uncertainty for more conservative investors.

Adobe also just completed its acquisition of Semrush, adding digital marketing intelligence to its platform. It also integrated Photoshop and Acrobat directly into ChatGPT. But Mizuho recently cut its Adobe rating to neutral, citing growing competition concerns. So investors in Adobe are essentially betting that its creative software moat holds up as AI tools continue to multiply.

Atlassian is also entering an exciting growth phase with strong momentum behind it. It raised its FY26 revenue guidance to around 24% and beat Q3 estimates by over 5%. But the stock remains down sharply from its highs, and GAAP profitability is still a work in progress.

Going forward, Adobe suits investors who want steady margins and capital returns, while Atlassian suits those willing to accept more risk in exchange for faster growth.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Should You Invest in Adobe or Atlassian?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ADBE or TEAM, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track ADBE or TEAM alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Adobe and Atlassian stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!