Key Stats for Charter Communications Stock

- 52-Week Performance: -2.4%

- 52-Week Range: $140.00 to $404.41

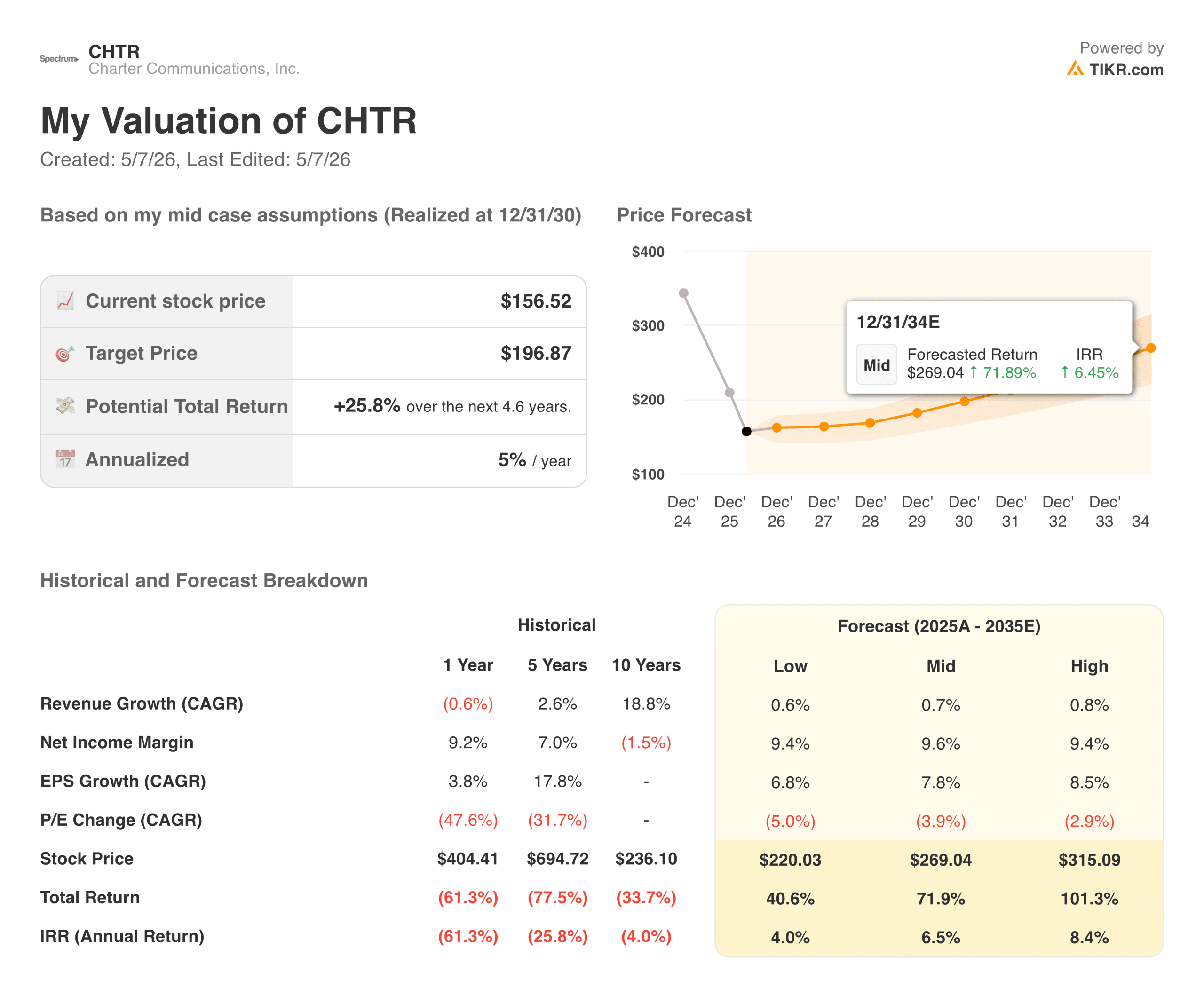

- Current Price: $156.52

- TIKR Target Price (Mid): ~$197

- TIKR Annualized IRR (Mid): ~5% per year

- Q1 2026 Earnings Reporting Date: 4/24/26

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

The Numbers Were Fine, the Subscribers Were Not

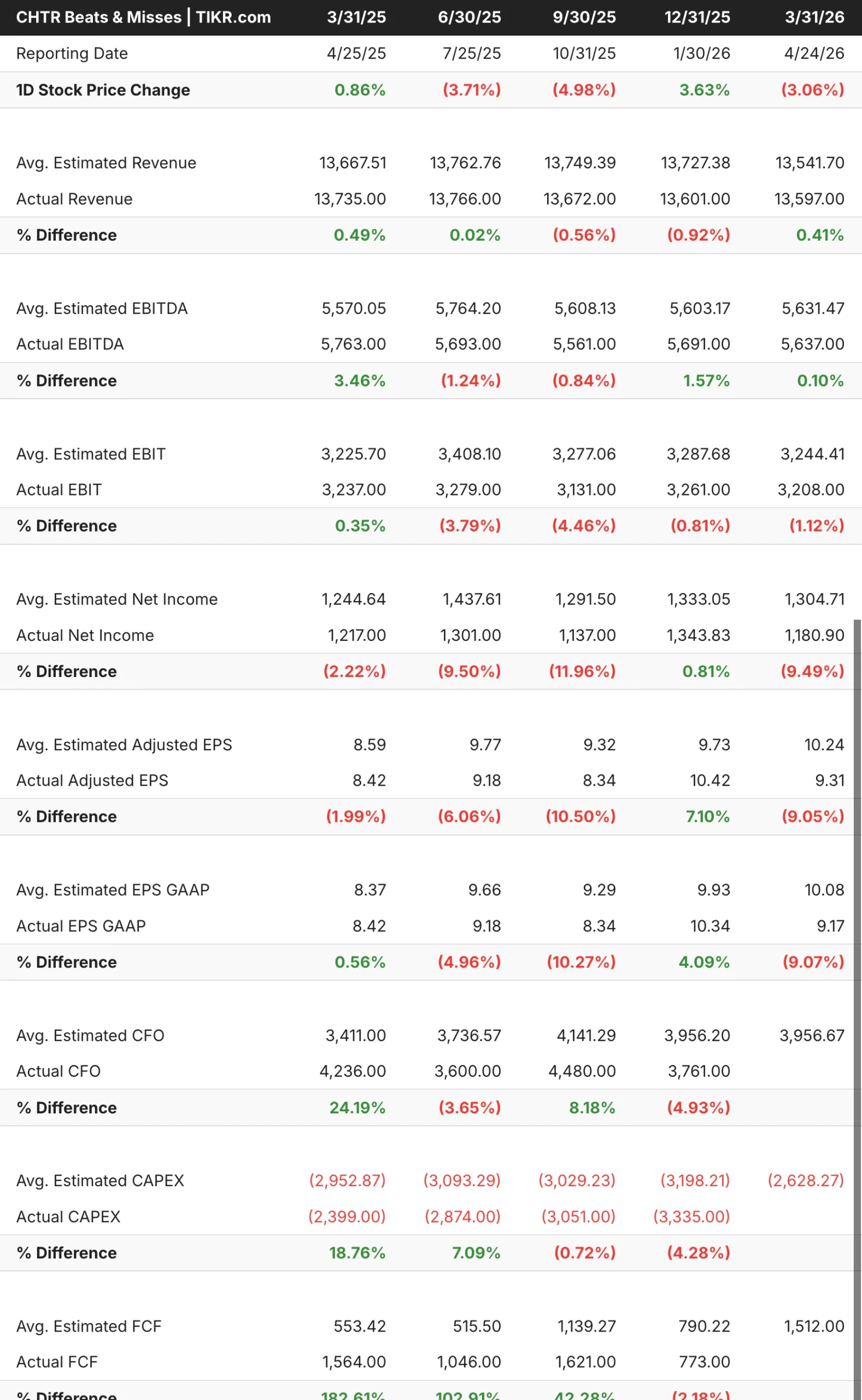

Charter (CHTR) reported Q1 2026 results on April 24th, and the headline numbers were mixed in a familiar way. Revenue came in at $13.6 billion, down about 1% year over year, with a small top-line beat and EBITDA essentially in line with expectations. The EPS miss was more pronounced, with reported earnings of $9.17 versus a consensus of around $10, a gap of about 9%.

The subscriber picture is what investors were really watching. Charter lost 120,000 internet customers in the quarter, worse than the roughly 72,000 it lost in the same period a year prior. Mobile was the counterweight, adding 368,000 lines to bring the total to 12.1 million, with residential mobile revenue up about 15% year over year. Video losses, a persistent drag, actually slowed dramatically to just 60,000 for the quarter.

CEO Chris Winfrey described the internet weakness as a top-of-funnel issue, pointing to lower gross additions in the low-income segment and a sluggish housing market. Management struck a confident tone on the call, citing improving churn, a fuller product portfolio, and the pending Cox transaction as pillars of the long-term thesis.

See historical and forward estimates for Charter Communications stock (It’s free!) >>>

Revenue Has Flatlined, the Margin Story Hasn’t

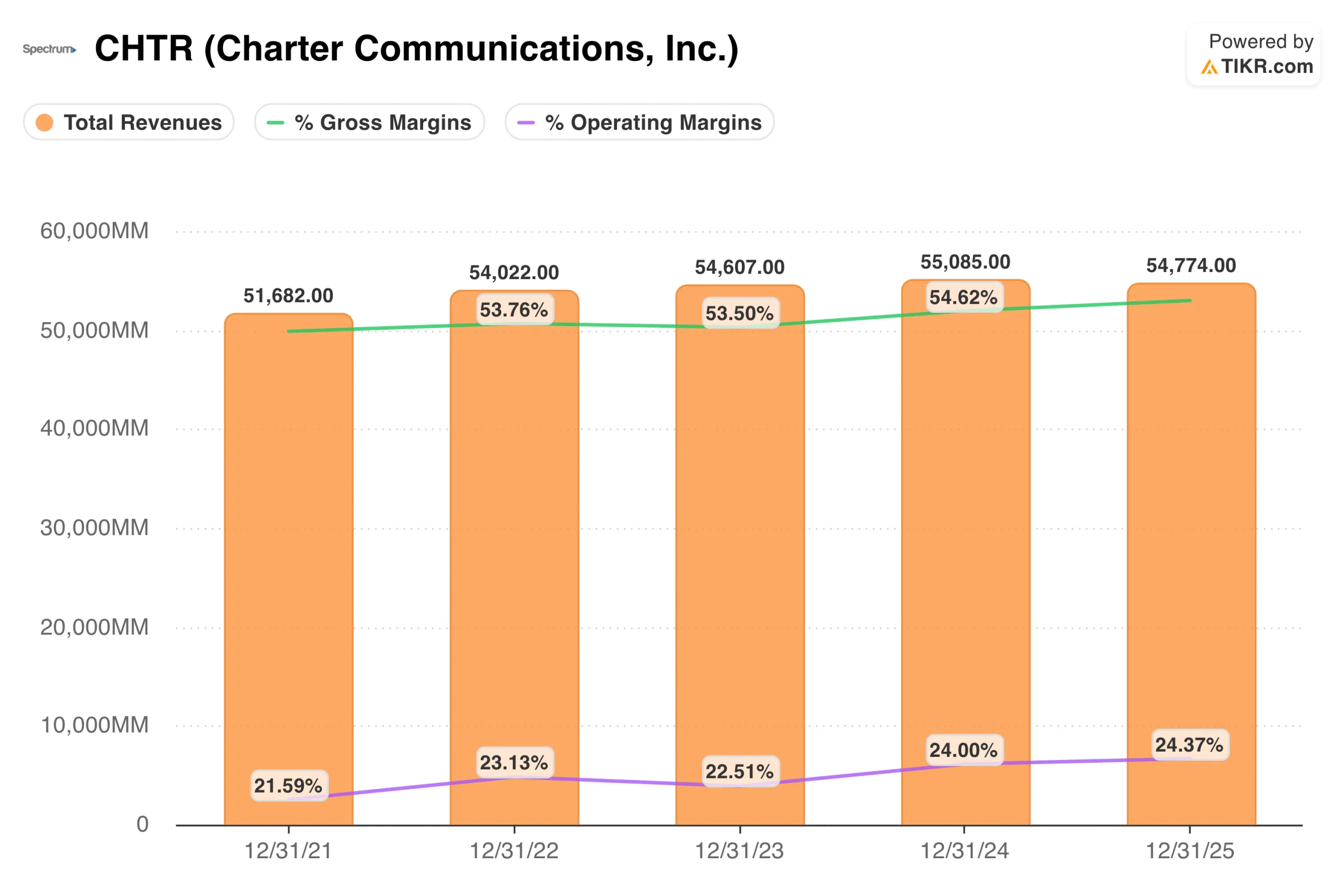

The revenue chart captures what Charter has become: a $54 billion business that has been essentially flat for four years. Revenue rose from $51.7 billion in 2021 to $54.8 billion in 2025, representing nominal growth, but far from what investors expected when the stock was trading at multiples of today’s price.

What is holding up the fundamental case is the margin structure. Operating margins have improved from around 22% in 2021 to around 24% in 2025, reflecting the natural exit from the high-cost video business and increasing efficiency in broadband and mobile operations. Charter is generating real cash despite subscriber headwinds, and the video cost curve is moving in the right direction.

The Cox acquisition is the single biggest variable in the near-term story. The deal, valued at $34.5 billion, would bring Cox’s roughly 6.5 million customers under the Spectrum brand and push Charter’s total passings to over 70 million households. The FCC and DOJ have both cleared the transaction, and New York approved it in March. California’s CPUC is the last remaining hurdle, with evidentiary hearings underway and a September 15th federal deadline that management is actively trying to meet. Charter has raised the expected synergies from the deal to $800 million.

See how Charter Communications performs against its peers in TIKR (It’s free!) >>>

Modest Upside, With a Lot Riding on Cox

TIKR’s model targets around $197 for Charter stock, implying a total return of roughly 26% from current levels over about 4.6 years, or around 5% annualized. The model assumes revenue growth of well under 1% annually, consistent with what Charter has actually delivered, with EPS growth closer to 8% in the mid case, driven by buybacks and operating leverage rather than top-line acceleration.

The bull case rests on a few things going right:

- Cox closes before the September 15th federal deadline, adding roughly 6.5 million customers to a network already built to serve them and unlocking $800 million in identified synergies

- Broadband subscriber losses stabilize as Charter’s network evolution improves its competitive position against fixed wireless providers

- Mobile continues compounding, with 12.1 million lines already and residential mobile revenue growing around 15% year over year

The bear case does not require a disaster:

- Internet losses accelerate further, overwhelming the mobile growth story and pressuring free cash flow at a time when the balance sheet carries significant leverage

- California delays Cox approval past the September deadline, forcing a reset of the federal review process and pushing the deal timeline into 2027

- Capital expenditures remain elevated longer than expected, limiting the buyback program that is central to the per-share earnings growth story

At around $157 against a target of around $197, the model says there is upside here. How much of it you believe depends almost entirely on which of those scenarios you find more plausible.

Should You Invest in Charter Communications

Charter is a business that generates substantial cash despite losing customers, and that nuance is what makes the stock genuinely interesting at current levels. The stock is near multi-year lows, the valuation is undemanding, and the Cox deal could be a real catalyst if California signs off before the September deadline.

The core risk is not that Charter disappears. It is that broadband subscriber losses continue at a pace that overwhelms the mobile growth story and limits the company’s ability to keep buying back stock at this rate. The network upgrade initiative underway is designed to close the competitive gap with fixed wireless providers like T-Mobile and Verizon, but that investment is also what is weighing on free cash flow in the near term.

At around $157 per share against a TIKR target of around $197, the implied return is real but not particularly urgent. The Cox close is the catalyst worth watching most closely. If California clears it before September, Charter exits 2026 as a materially larger business with a clearer path to the kind of subscriber and revenue growth the model is counting on.

Access Professional Tools to Analyze CHTR stock on TIKR for Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!