Key Takeaways:

- Trane Technologies beat Q1 2026 earnings, with adjusted EPS of $2.63 versus the $2.53 consensus estimate. Revenue rose 6% year-over-year to $4.97B, driven by strong commercial HVAC demand. Management raised its full-year 2026 profit outlook following the Q1 beat.

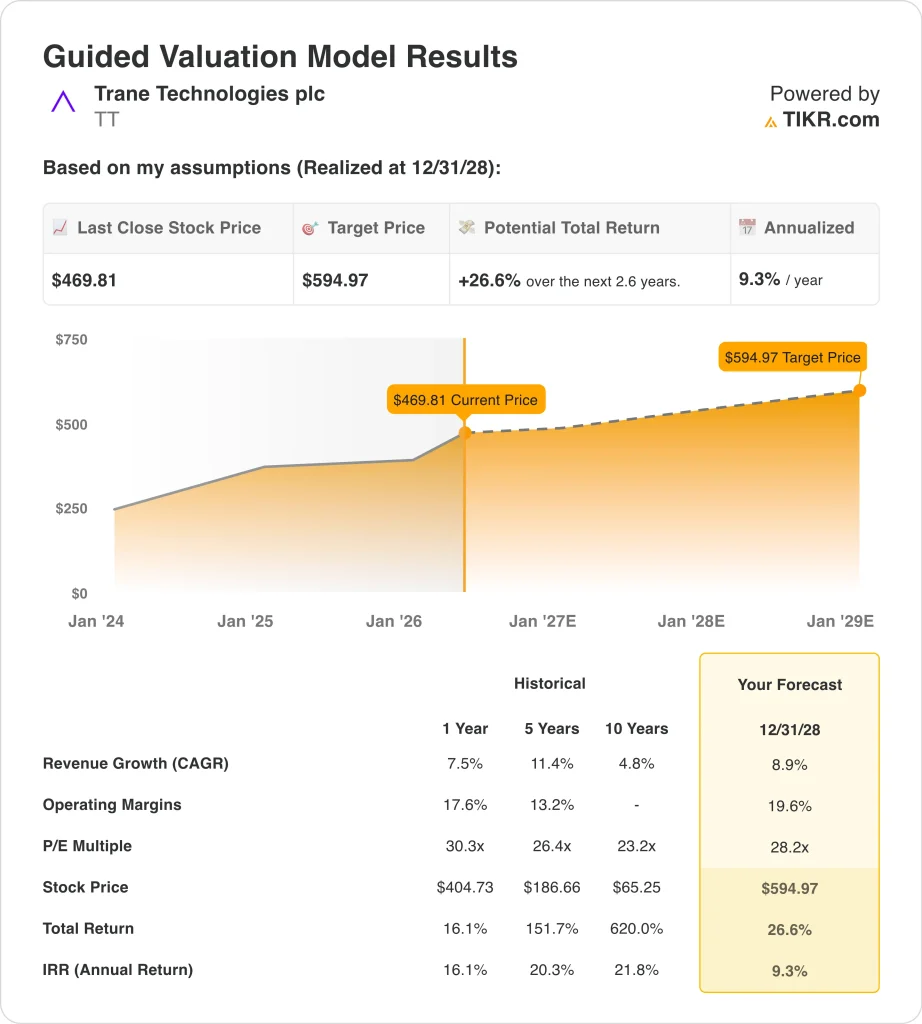

- TT stock could rise from $470 to around $595 per share by December 2028.

- That implies a 27% total return, or a 9% annualized return over the next 2.6 years.

What Happened?

Trane Technologies (TT) started fiscal 2026 with a solid earnings beat. Adjusted EPS came in at $2.63, ahead of the $2.53 consensus, and revenue grew 6% to $4.97B.

Strong commercial HVAC demand powered the performance across both the Americas and international segments. Management also raised its full-year profit forecast, adding further confidence to the outlook.

The data center cooling story is gaining momentum fast. Trane completed its acquisition of LiquidStack in March 2026. LiquidStack provides liquid cooling solutions for high-performance AI computing environments, and so this deal positions Trane directly inside the fast-growing AI infrastructure market.

Trane also completed its earlier acquisition of Stellar Energy, further strengthening its data center thermal management portfolio.

A high-profile technology partnership added to the momentum as well. Trane teamed with NVIDIA to optimize AI factory thermal management, and the collaboration improved efficiency by nearly 10% across a one-gigawatt AI factory design.

Oppenheimer raised its price target on TT in April 2026, citing a stronger order outlook. So investors increasingly see TT as a climate-plus-AI infrastructure play with two powerful growth engines.

Here’s why Trane Technologies stock could deliver solid returns through 2028 as AI data center cooling and commercial HVAC demand both trend strongly higher.

What the Model Says for Trane Stock

We analyzed the upside potential for Trane Technologies stock based on its commercial HVAC leadership, expanding data center liquid cooling business, and consistent margin improvement driven by operational scale.

Based on estimates of around 9% annual revenue growth, around 20% operating margins, and a normalized P/E multiple of 28.2x, the model projects Trane Technologies’ stock could rise from $470 to around $595 per share.

That would be a 27% total return, or a 9% annualized return over the next 2.6 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for TT stock:

1. Revenue Growth: 9%

Trane’s forward 2-year revenue CAGR estimate sits at 9%, and the Q1 2026 beat supports that trajectory. Commercial HVAC demand is rebounding strongly, and the LiquidStack acquisition adds an entirely new AI cooling revenue stream.

Macro factors like tariff uncertainty and construction cycles could create near-term noise. But management’s Q1 beat and raised full-year outlook suggest these headwinds are manageable.

Based on analysts’ consensus estimates, we used around 9% annual revenue growth. This reflects the combined strength of commercial HVAC, transport refrigeration through Thermo King, and new AI data center cooling revenues from recent acquisitions.

2. Operating Margins: 20%

Trane’s last 12-month EBIT margin stands at 18%, and the company has consistently expanded margins over recent years. Pricing power in commercial HVAC markets and operating leverage in growing businesses both support further margin improvement.

The LiquidStack and Stellar Energy acquisitions bring premium-margin, contract-driven products to the portfolio. And both businesses serve customers who prioritize thermal performance over cost, supporting strong pricing discipline.

Based on analysts’ consensus estimates, we used around 20% operating margins. This reflects Trane’s disciplined cost management and its ability to extract operating leverage from its growing commercial and data center backlog.

3. Exit P/E Multiple: 28.2x

Trane currently trades at a forward P/E of around 31x, but the model uses a slightly lower 28.2x exit multiple. This reflects a modest normalization from the current premium valuation over the holding period.

The 28.2x exit multiple still assigns Trane a meaningful premium over the broader industrial sector. And that premium is justified by the company’s dual exposure to climate solutions and AI infrastructure.

Based on analysts’ consensus estimates, we used a 28.2x exit P/E multiple. This level is consistent with Trane’s historical trading range and its premium position among global industrial climate companies.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for TT stock through 2034 show varied outcomes based on commercial HVAC pricing and AI data center cooling adoption rates (these are estimates, not guaranteed returns):

- Low Case: HVAC demand softens, and AI cooling ramp is slower than expected → 4% annual returns

- Mid Case: Commercial HVAC holds strong and data center cooling scales steadily → 7% annual returns

- High Case: AI infrastructure boom accelerates, and new cooling contracts drive significant upside → 10% annual returns

Going forward, Trane’s performance will hinge on the pace of AI data center buildout and commercial HVAC market conditions globally. The LiquidStack acquisition adds meaningful optionality in a segment that is growing rapidly as AI workloads expand.

But the mid-case annual return of around 7% over the longer term suggests investors should weigh the current premium valuation carefully against the growth opportunity ahead.

See what analysts think about TT stock right now (Free with TIKR) >>>

Should You Invest in Trane?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up TT, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track TT alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze the stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!