Key Stats

- Current Price: $87.31 (May 7, 2026)

- Q1 2026 Revenue: $2.3B, +2% reported, flat organic

- Q1 2026 Adjusted EPS: $1.53, +3% YoY

- Full-Year Revenue Guidance: $9.68B to $9.96B (2% to 5% growth)

- Full-Year Adjusted EPS Guidance: $6.85 to $7.00

- TIKR Model Price Target: $123

- Implied Upside: ~41%

Zoetis Stock Slips as Companion Animal Pressure Overshadows Livestock Strength

Zoetis stock fell more than 21% on May 7 after the company reported Q1 2026 revenue of $2.3B, flat on an organic operational basis, against a backdrop of intensifying competition and weakening pet owner spending that caught management off guard.

Adjusted diluted EPS came in at $1.53, up 3% year over year, supported by share repurchases rather than operating momentum.

The companion animal segment drove the miss, posting $1.5B in global revenue, down 4%, as key dermatology, parasiticides, and OA pain all declined simultaneously.

Key dermatology recorded $347M in revenue, down 11%, with Apoquel facing price-driven competitive pressure and Cytopoint hit by lower clinic traffic rather than direct competition.

The Simparica franchise contributed $385M globally, declining 1%, with Simparica Trio at $297M and Simparica at $88M, both slipping modestly as fewer vet visits weighed on new patient starts.

OA pain mAbs Librela and Solensia combined for $140M, down 8%, though U.S. Librela revenue increased sequentially for the first time in six quarters, which management cited as a stabilization signal.

CEO Kristin Peck pointed to four converging pressures: sustained price increases in veterinary clinics, increased pet owner price sensitivity, intensified competition across dermatology and parasiticides, and the fact that new competitive entrants have not yet expanded the overall market, removing the cushion Zoetis historically relied on.

Livestock was the clear counterweight, posting $720M in global revenue, growing 12%, with broad-based gains across cattle, poultry, swine, and fish driven by favorable producer economics and disease outbreak-related vaccine demand.

Zoetis cut its full-year revenue guidance to $9.68B to $9.96B from a prior range that embedded better U.S. companion animal performance, now reflecting 2% to 5% organic operational growth, while adjusted EPS guidance of $6.85 to $7.00 incorporates a cost and productivity program launched in response to the Q1 environment.

Zoetis Stock and the Income Statement: Margin Pressure Building Beneath the Surface

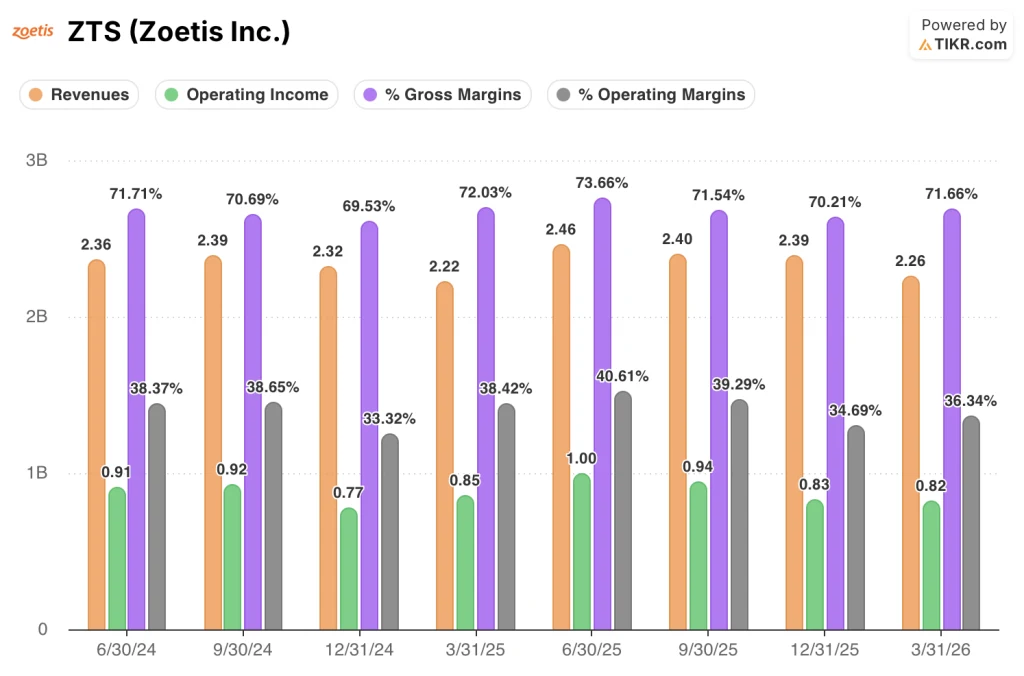

Zoetis stock entered Q1 with gross margins that had held up reasonably well, but the income statement now shows operating leverage moving in the wrong direction.

Revenue has decelerated for four consecutive quarters, falling from $2.46B in Q2 2025 to $2.40B in Q3, $2.39B in Q4, and $2.26B in Q1 2026, the lowest quarterly figure in the trailing eight periods shown.

Gross margin came in at 71.7% in Q1 2026, essentially flat with the 72.0% posted in Q1 2025 and recovering from the 70.2% trough in Q4 2025.

Operating income was $820M in Q1 2026, down 4% year over year from $850M in Q1 2025, with operating margin at 36.3% versus 38.4% in the prior-year quarter.

That 210-basis-point operating margin compression reflects the revenue mix shift toward lower-margin livestock and away from the premium companion animal products where Zoetis historically earns its highest returns.

The sequential trend adds context: operating margin peaked at 40.6% in Q2 2025, then fell to 39.3% in Q3, compressed further to 34.7% in Q4, and now sits at 36.3%, suggesting the business has not yet found a stable floor.

CFO Wetteny Joseph noted that excluding foreign exchange, gross margins actually improved approximately 140 basis points in the quarter, attributing the underlying improvement to pricing and lower manufacturing costs, partially offset by product and geographic mix.

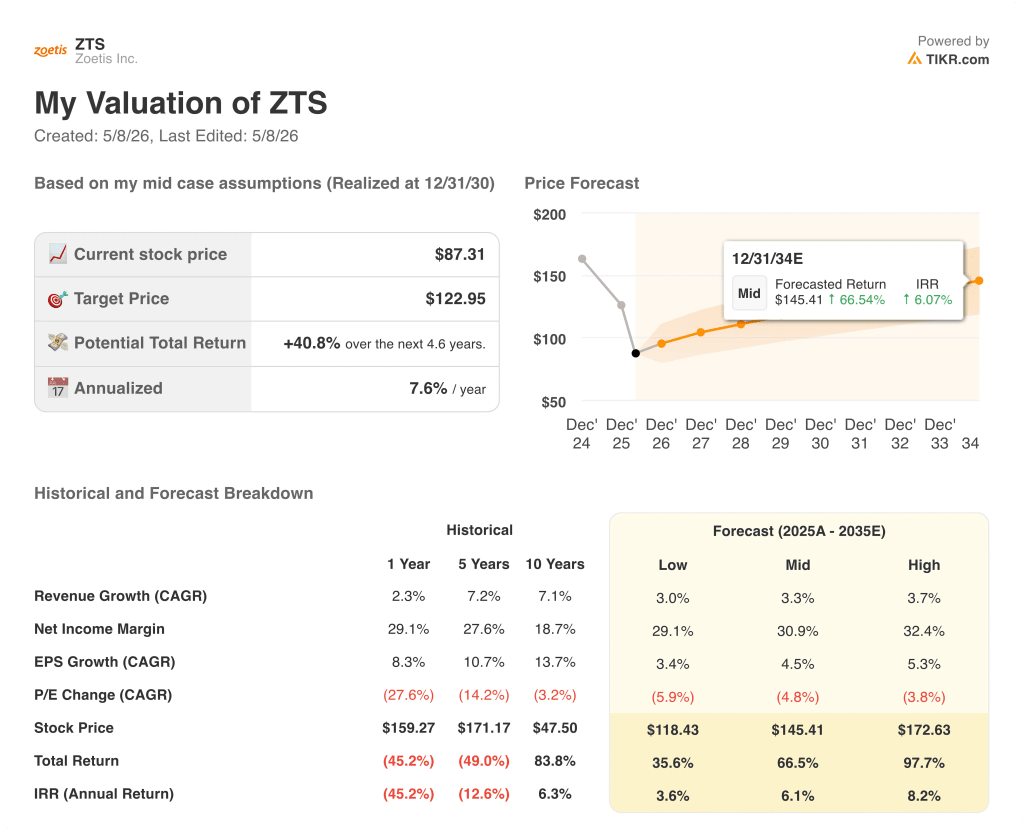

What Does the Valuation Model Say?

TIKR’s model puts a price target of $123 on ZTS stock, implying roughly 41% upside from the current $87 close.

The mid-case assumptions driving that target are a revenue CAGR of 3.3% through 2035 and a net income margin of 31%, both modest by Zoetis’ historical standards given the company’s 10-year revenue CAGR of 7.1% and a 29% net income margin over the past year.

The Q1 report does not invalidate the model, but it shifts more of the expected return toward the back half of the forecast period, when Zoetis’ next innovation cycle, with 12 potential blockbusters and more than $7B in additional market opportunity, is supposed to begin delivering according to management commentary on the call.

With the stock down 21% in a single session and the model implying a 41% recovery, Zoetis stock sits closer to fair value on the model than at any point in the past five years, but execution risk over the next six to eight quarters is now meaningfully higher than the guidance range suggests.

Companion animal posted its worst organic quarter in recent memory, but the model’s 41% upside only works if Zoetis can bridge two to three years of transition without sustained market share erosion in its core franchises.

What Has to Go Right

- U.S. Librela revenue increased sequentially for the first time in six quarters in Q1 2026, and management expects the OA pain franchise to return to growth as the year progresses, supported by long-acting mAb launches in select EU markets and Canada

- The Simparica franchise exited Q1 with share levels nearing prior year, after competitive launch promotions compressed share in the second half of 2025, suggesting stabilization rather than structural deterioration

- Livestock, now generating $720M per quarter at 12% organic growth, provides a durable buffer while companion animal recovers and diversifies the revenue base in a way that was not available to Zoetis a decade ago

- The cost and productivity program launched in Q1 delivered adjusted net income growth of 1% despite flat organic revenue, demonstrating P&L leverage that management expects to sustain through 2026

What Could Still Go Wrong

- Excluding the $100M in sales that shifted from Q4 2025 into Q1 2026 due to fiscal year alignment, underlying Q1 organic growth was approximately negative 5%, meaning the reported flat organic number overstates the true exit rate

- Key dermatology is down 11% globally with Apoquel losing share on price in a market where clinic visit volumes are also falling, creating a dual headwind with no near-term catalyst until long-acting Cytopoint launches

- Management guided for 2% to 5% full-year organic growth from a Q1 base that CFO Joseph confirmed reflects ongoing competitive and macro headwinds through the remainder of 2026, not a V-shaped recovery assumption

- Generic competition is now active in both Convenia and Cerenia, two blockbuster products, and represents the first meaningful generic pressure Zoetis has faced in its companion animal franchise

Should You Invest in Zoetis Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Zoetis stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Zoetis Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ZTS stock on TIKR for Free →