Key Takeaways:

- IDEXX Laboratories delivered Q1 FY26 diluted earnings per share of $3.47, up 17% year over year, with revenue rising 14% to $1.14 billion, and raised its full-year 2026 guidance.

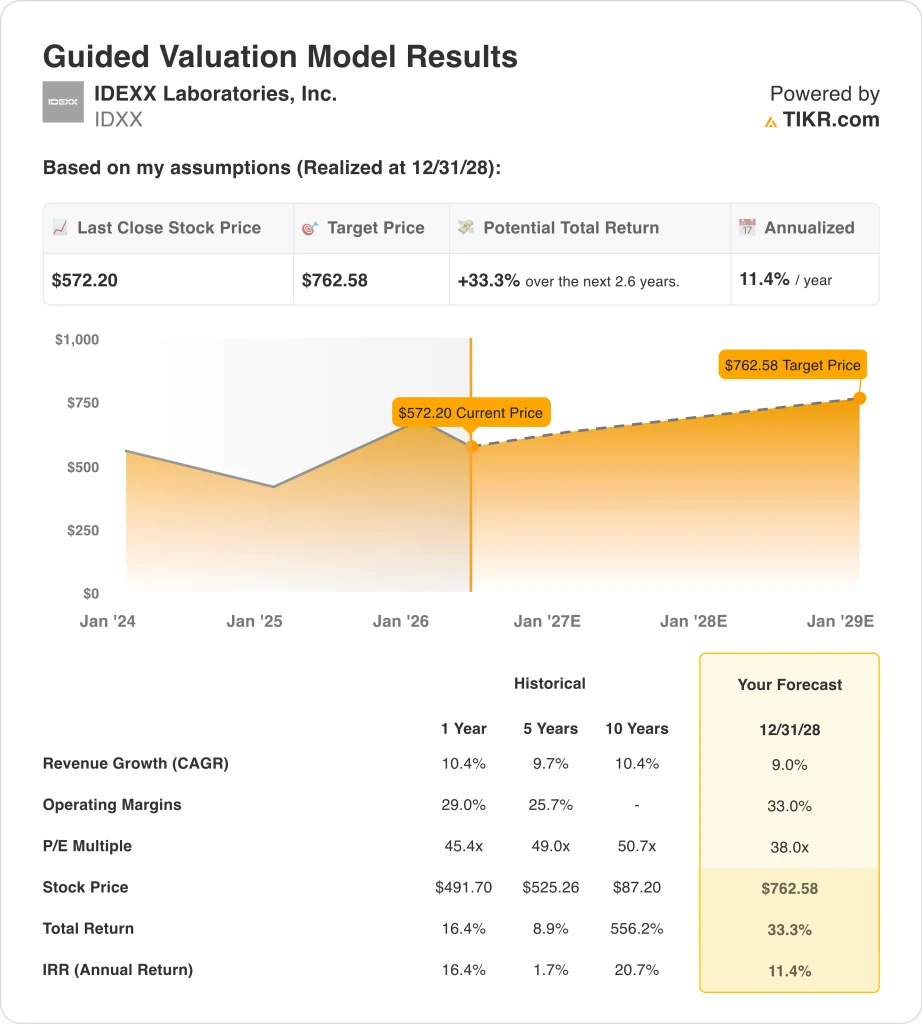

- IDXX stock trades at $572, well below its 52-week high of $770, and the analyst consensus target price stands at $713. Based on our valuation assumptions, IDXX stock could rise from $572 to around $763 per share by December 2028.

- This implies a total return of around 33% and an annualized return of around 11% over the next 2.6 years.

What Happened?

IDEXX Laboratories, Inc. (IDXX) delivered strong first-quarter 2026 results and raised its full-year guidance. Revenue climbed 14% year over year to $1.14 billion, beating analyst estimates. Diluted earnings per share rose 17% to $3.47. The results confirmed that companion animal diagnostic spending remains resilient despite broader macroeconomic uncertainty.

IDEXX develops and markets diagnostic products and services primarily for companion animals like dogs and cats. Its business includes in-clinic analyzers that run blood tests, rapid assay tests for specific diseases, and reference laboratory services for complex diagnostics. The company also serves water quality testing and food safety markets. But companion animal diagnostics make up the vast majority of revenue and earnings.

The company announced a CEO transition in January 2026. Jonathan Jay Mazelsky became President and CEO, succeeding the prior leadership team. IDEXX also named April 2026 as the exit date for EVP Nimrata Hunt. These leadership changes are part of a planned succession process rather than any operational disruption. Investor reaction has been measured, with the stock down around 15% year to date despite strong earnings.

Pet healthcare spending is a long-term secular growth trend. Vet visits, testing frequency, and spending per visit continue to rise as pet owners treat companion animals as family members. IDEXX benefits from this trend through recurring consumable revenues from its installed base of diagnostic analyzers.

Here’s why IDEXX stock could offer double-digit returns through 2028 for investors who believe in the companion animal health megatrend.

What the Model Says for IDXX Stock

We analyzed the upside potential for IDEXX Laboratories stock based on its expanding installed base of diagnostic instruments, recurring consumable revenues from companion animal testing, and durable pricing power in veterinary diagnostics.

Based on estimates of around 9% annual revenue growth, around 33% operating margins, and a normalized P/E multiple of 38.0x, the model projects IDEXX Laboratories’ stock could rise from $572 to around $763 per share.

That would be a total return of around 33%, or an annualized return of around 11% over the next 2.6 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for IDXX stock:

1. Revenue Growth: 9%

IDEXX grew revenue at around 10.4% over the past year and at around 9.7% annually over the past five years. Q1 FY26’s 14% growth beat expectations and showed accelerating momentum. The company raised its full-year 2026 guidance after the strong quarter, adding credibility to the near term outlook.

IDEXX’s revenue model is highly recurring. Instruments are placed in veterinary clinics, and consumable reagents and test kits generate ongoing revenue from that installed base. Each new clinic relationship adds years of predictable consumable revenue. This compounding base makes revenue highly visible and durable.

Based on analysts’ consensus estimates, we used a forecast of around 9% annual revenue growth. This reflects IDEXX’s ability to grow its installed base and benefit from higher testing frequency and vet visit volumes across the companion animal market.

2. Operating Margins: 33%

IDEXX’s trailing annual operating profit margin is approximately 29%, and the gross margin is 62.1%. These strong margins reflect the proprietary nature of IDEXX’s diagnostic platform and the recurring consumable revenue model. Competitors cannot easily replicate the depth of IDEXX’s product portfolio or its laboratory network.

The company also benefits from operational leverage as its installed base grows. Consumable revenue grows without proportional increases in manufacturing cost. And reference laboratory services carry high incremental margins as volume scales.

Based on analysts’ consensus estimates, we used an operating margin of around 33%. This reflects a moderate improvement from the current trailing level as the installed base matures and operating leverage builds across the business.

3. Exit P/E Multiple: 38x

IDEXX currently trades at a forward price to earnings ratio of around 38x. This is a premium valuation relative to most healthcare companies. But it reflects the quality of IDEXX’s business model, the predictability of its revenue, and its dominant market position in companion animal diagnostics.

The company’s trailing price to earnings ratio is 42.1x, showing that the forward multiple represents only a modest compression from current levels. J.P. Morgan noted in April 2026 that it was upbeat on animal health companies ahead of Q1 results. IDEXX delivered on that thesis with a strong beat and raised guidance.

Based on analysts’ consensus estimates, we used an exit P/E of 38.0x. This is consistent with the current forward multiple and reflects the durable nature of IDEXX’s competitive advantages in a specialized and growing diagnostic market.

Build your own Valuation Model to value any stock (It’s free!) >>>

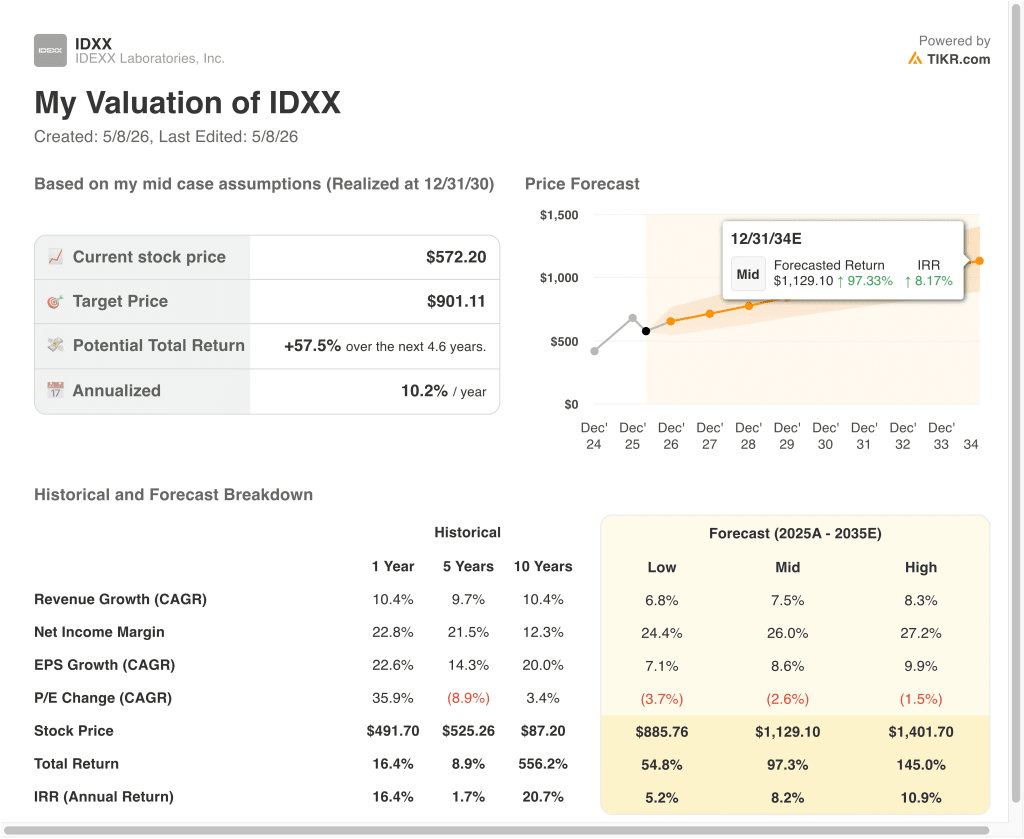

What Happens If Things Go Better or Worse?

Different scenarios for IDXX stock through 2034 show varied outcomes based on installed base growth, testing frequency trends, and companion animal healthcare spending (these are estimates, not guaranteed returns):

- Low Case: Installed base growth slows and vet visit volumes moderate → around 5% annual returns

- Mid Case: Steady base expansion and consumable growth deliver on consensus → around 8% annual returns

- High Case: Accelerating diagnostics adoption and international expansion drive outperformance → around 11% annual returns

Going forward, IDEXX’s Q1 results and raised guidance confirm that the companion animal diagnostics market continues to grow despite macroeconomic pressure.

The near-term model’s 11% annualized return reflects a favorable current entry point relative to historical valuations for this business. Investors seeking a high-quality healthcare compounder at a meaningful discount to the 52-week high may find the current setup worth evaluating carefully.

See what analysts think about IDXX stock right now (Free with TIKR) >>>

Should You Invest in Idexx?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up IDXX, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track IDXX alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze the stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!