Key Takeaways:

- Expedia beat Q1 2026 earnings significantly, with adjusted EPS of $1.96 versus the $1.38 consensus estimate.

- Revenue rose 15% year-over-year to $3.43B, and adjusted EBITDA surged 83% to $542M.

- EXPE stock trades at around $253, up 53% over the past year, with a 52-week range of $149 to $304.

- That implies a 10% total return, or a 4% annualized return over the next 2.6 years.

What Happened?

Expedia Group (EXPE) delivered a strong first quarter in fiscal 2026, beating expectations across key metrics. Adjusted EPS of $1.96 cleared the $1.38 consensus by a wide margin, and revenue grew 15% to $3.43B. Adjusted EBITDA surged 83% to $542M, reflecting exceptional operating leverage in the online travel business. But the stock’s near-term reaction was tempered by one key headwind flagged on the earnings call.

Expedia reported that the ongoing Middle East conflict is weighing on international bookings. Airbnb cited the same impact in its own earnings update, so this is a sector-wide concern rather than a company-specific issue. And management guided forward bookings conservatively, reflecting caution around geopolitical uncertainty. So investors are watching to see whether this booking softness is temporary or extends further.

On the strategic front, Uber struck a deal with Expedia to add hotel bookings through the Uber super app. This partnership extends Expedia’s distribution reach into a high-traffic platform used by tens of millions of consumers.

Expedia also named Derek Andersen, formerly CFO at Snap, as its new finance chief effective May 11, 2026. A new CFO often signals a renewed focus on capital efficiency and shareholder returns.

Here’s why Expedia stock could deliver meaningful long-term returns through 2028 and beyond as new distribution channels and margin improvement offset geopolitical booking headwinds.

What the Model Says for EXPE Stock

We analyzed the upside potential for Expedia stock based on its diversified online travel platform, growing hotel and vacation rental inventory through brands like Hotels.com and Vrbo, and new consumer distribution partnerships with platforms like Uber.

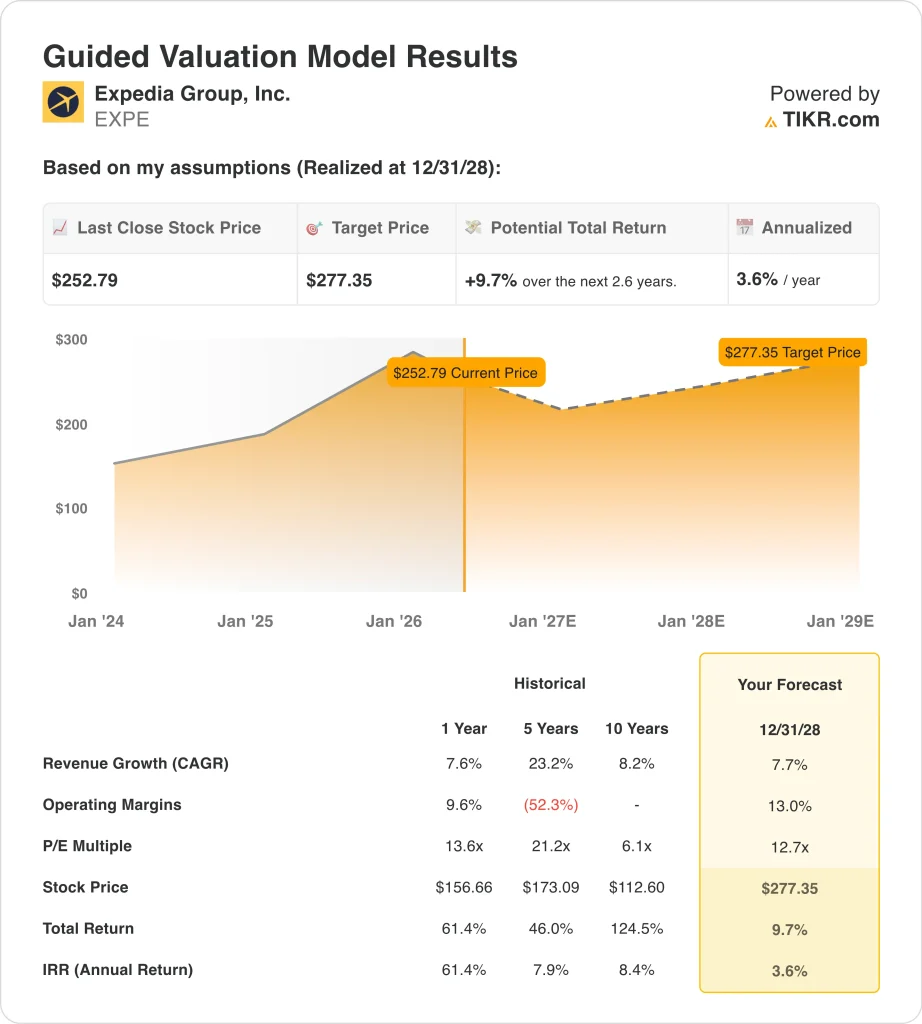

Based on estimates of around 8% annual revenue growth, around 13% operating margins, and a normalized P/E multiple of 12.7x, the model projects Expedia stock could rise from $253 to around $277 per share.

That would be a 10% total return, or a 4% annualized return over the next 2.6 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for EXPE stock:

1. Revenue Growth: 8%

Expedia delivered 15% revenue growth in Q1 2026, well above its 1-year historical CAGR of 7.6%. The Q1 beat was driven by strong booked room nights across the US, EMEA, and global markets. But the Middle East conflict is expected to create a near-term drag on forward booking volumes.

The Uber partnership adds meaningful upside to this assumption. Embedding hotel bookings inside a high-traffic consumer platform could drive incremental demand beyond what standalone marketing achieves.

Based on analysts’ consensus estimates, we used around 8% annual revenue growth. This reflects continued global travel demand recovery, partially offset by geopolitical headwinds and ongoing competition from Airbnb and direct hotel booking channels.

2. Operating Margins: 13%

Expedia’s last 12-month EBIT margin stands at 14.7%, and the gross margin is an exceptional 90.1%. These metrics reflect the asset-light, platform-based nature of the online travel agency model. But marketing and technology investments keep operating margins meaningfully below gross margins.

The new CFO appointment could bring renewed focus on cost discipline and shareholder return optimization. And technology infrastructure scale tends to improve operating margins as volumes grow.

Based on analysts’ consensus estimates, we used around 13% operating margins. This is slightly below the current LTM level and reflects a conservative assumption around continued platform investment and near-term pressure from geopolitical booking headwinds.

3. Exit P/E Multiple: 12.7x

Expedia currently trades at an NTM P/E of about 12.7x, which is modest for an online travel platform generating 90.1% gross margins. This discount reflects near-term concerns about Middle East bookings and macro uncertainty around international travel.

But Expedia’s 3-year EPS CAGR of 32.7% demonstrates strong underlying earnings power. And as earnings grow, the compressed multiple could expand materially over a multi-year horizon.

Based on analysts’ consensus estimates, we maintained a 12.7x exit P/E multiple. This reflects a stable and conservative valuation for a business generating strong operating leverage and meaningful free cash flow from its travel platform.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for EXPE stock through 2034 show varied outcomes based on global travel demand recovery and operating margin expansion (these are estimates, not guaranteed returns):

- Low Case: Middle East conflict broadens, and global travel demand softens → 9% annual returns

- Mid Case: Travel demand recovers steadily, and the Uber partnership drives consistent booking growth → 13% annual returns

- High Case: Global travel booms and operating margins expand significantly beyond current levels → 16% annual returns

Going forward, Expedia’s stock performance depends on global travel demand trends and its ability to execute on new distribution partnerships like the Uber deal.

The near-term guided model suggests a modest 4% annualized return through 2028, but the longer-term scenario framework is considerably more compelling, pointing to around 13% annualized returns in the mid case through 2034.

Investors willing to look past geopolitical noise may find the long-term setup attractive relative to the current valuation.

See what analysts think about EXPE stock right now (Free with TIKR) >>>

Should You Invest in Expedia?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up EXPE, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track EXPE alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Expedia stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!