Key Stats

- Current Price: $189 (May 7, 2026)

- Q1 2026 Revenue: $1.01B, up 32% YoY

- Q1 2026 Adjusted EPS: $0.60, up 30% YoY

- Q2 2026 Revenue Guidance: $1.07B to $1.08B (29% to 31% YoY growth)

- Q2 2026 Non-GAAP EPS Guidance: $0.57 to $0.59

- FY2026 Revenue Guidance: $4.3B to $4.34B (25% to 27% YoY growth)

- FY2026 Non-GAAP EPS Guidance: $2.36 to $2.44

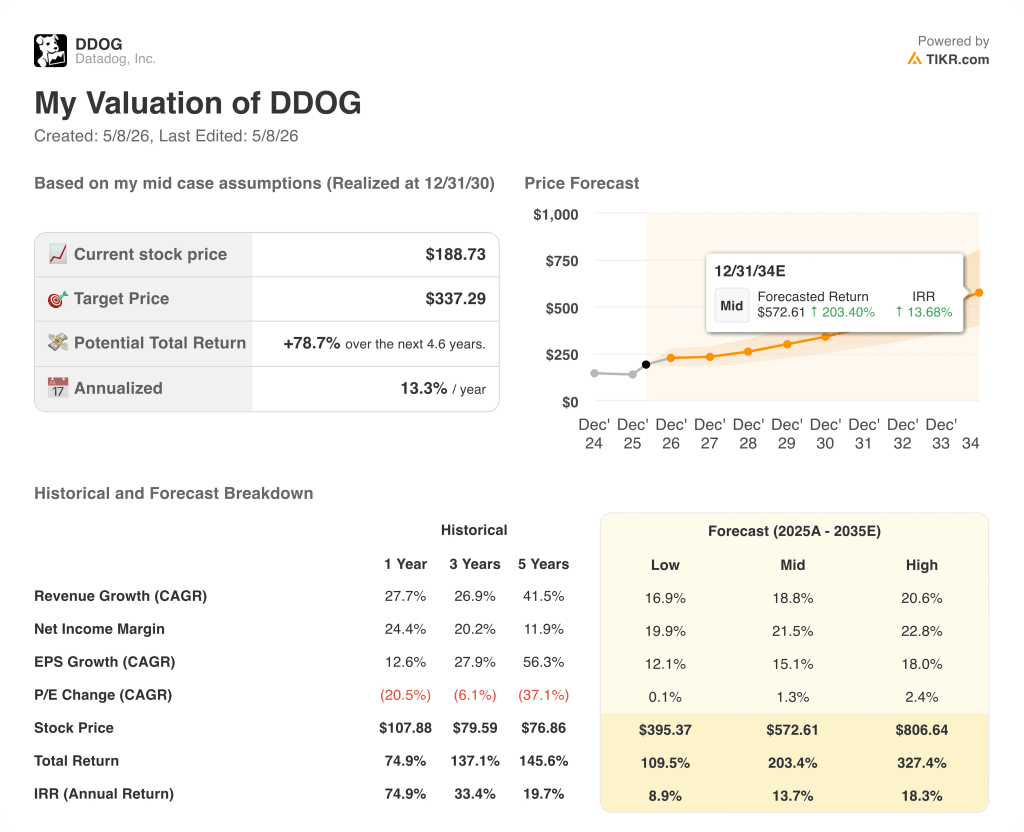

- TIKR Model Price Target: $337 (mid case, realized 12/31/30)

- Implied Upside: ~79%

Datadog Stock Breaks $1B in Quarterly Revenue as AI Demand Accelerates

Datadog stock (DDOG) surged more than 31% on May 7, 2026, after the company reported Q1 revenue of $1.01 billion, up 32% year-over-year and above the high end of guidance, marking the first time quarterly revenue has crossed the $1 billion threshold in the company’s history.

Adjusted EPS came in at $0.60, up from $0.46 in the year-ago quarter and above the $0.51 Street estimates.

The acceleration was broad-based, according to CEO Olivier Pomel on the Q1 2026 earnings call, with revenue growth rising from 29% last quarter and 25% in the year-ago quarter, driven by strength across both AI-native and non-AI customers.

Non-AI customer revenue growth accelerated to mid-20s percent year-over-year, up from 23% the prior quarter and 19% in the year-ago quarter, a signal that Datadog stock is not solely a beneficiary of AI tailwinds but also of continued cloud migration and platform consolidation.

The quarter produced an all-time record for sequential ARR added, with ARR growth accelerating in each month of Q1 and continuing into April, according to CFO David Obstler on the call.

New logo annualized bookings set a new all-time record by a significant margin and more than doubled versus a year ago, with new logo average land size also more than doubling year-over-year.

Two of the highest-profile wins were 7-figure and 8-figure annualized deals with the AI research divisions at two of the world’s largest technology companies, both deploying Datadog to optimize hyperscale AI training workloads and GPU monitoring on large parallel GPU grids.

The company’s total ARR now exceeds $4 billion, and AI-related usage metrics accelerated sharply within the quarter: Bits AI SRE agent investigations more than doubled from December to March, LLM observability spans nearly tripled quarter-over-quarter, MCP server tool calls quadrupled quarter-over-quarter, and Bits Assistant messages increased by a factor of 12 in the same period.

Platform adoption metrics also strengthened, with 35% of customers now using 6 or more products, up from 28% a year ago, and 20% using 8 or more products, up from 13%.

In March, the company launched its MCP server for general availability, enabling developers to access live production data to debug applications directly in AI coding agents or IDEs.

The company also received FedRAMP High certification from the U.S. federal government, opening access to federal agency customers with the most sensitive workloads, and announced plans to launch its next data center in the U.K.

For Q2 2026, management guided revenue to $1.07 billion to $1.08 billion, representing 29% to 31% year-over-year growth, with non-GAAP operating income of $225 million to $235 million, a 21% to 22% operating margin, and non-GAAP EPS of $0.57 to $0.59.

The Q2 guidance reflects approximately $15 million in costs associated with the company’s DASH user conference scheduled for June 9 and 10 in New York City.

For the full year, Datadog guided revenue to $4.3 billion to $4.34 billion, representing 25% to 27% growth, with non-GAAP operating income of $940 million to $980 million and non-GAAP EPS of $2.36 to $2.44.

Free cash flow in Q1 was $289 million, with a 29% free cash flow margin, and the company ended the quarter with $4.8 billion in cash, cash equivalents, and marketable securities, according to Obstler on the call.

Datadog Stock Valuation Model Results (TIKR)

The TIKR model prices Datadog stock at $337 under mid-case assumptions realized through December 31, 2030, implying approximately 79% upside from the current price of $189.

The mid-case assumes a revenue CAGR of 18.8% and a net income margin of 21.5%, with EPS compounding at 15.1% annually through the forecast period.

A quarter that crossed $1 billion in revenue for the first time, held a 29% free cash flow margin, and produced an all-time record for sequential ARR added makes those assumptions look more credible today than they did 90 days ago.

After a 31% single-day move, Datadog stock is no longer priced for the base case. The argument now is about whether the new demand vectors disclosed this quarter can sustain the acceleration.

The near-term picture is as clean as it has been in years.

Non-AI customer revenue growth accelerated to mid-20s percent year-over-year, up from 19% a year ago, demonstrating that the platform’s growth is not solely a function of AI infrastructure spend.

New logo bookings more than doubled year-over-year and set an all-time record, with average land size also more than doubling, a combination that implies stronger future expansion revenue rather than just volume.

RPO reached $3.48 billion, up 51% year-over-year, with current RPO growing in the mid-40s percent range as multiyear deals increased in mix.

Q2 guidance implies sequential revenue growth of $64 million to $74 million, the largest in the company’s history.

The long-term thesis asks more of the business than Q1 alone can answer.

The hyperscaler and training workload wins are significant but early. Pomel acknowledged on the call that training as a market for Datadog is a recent development, noting the company “didn’t see a lot of it last year.”

GPU monitoring is a new product, and the 7-figure and 8-figure deals signed this quarter are the first proof points, not a proven cycle.

Management also disclosed it applied a higher degree of conservatism specifically to its largest customer in Q2 guidance, a signal that concentration at the top of the customer base remains a variable.

FedRAMP High certification and the U.K. data center expansion both represent real growth optionality, but both are early-stage investments with timelines that extend well beyond 2026.

The TIKR high-case scenario requires a 20.6% revenue CAGR and 22.8% net income margin sustained through 2035, with a P/E CAGR that has contracted 20.5% over the past year as a reminder that multiple expansion is not a given even when the fundamentals cooperate.

Should You Invest in Datadog, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Datadog stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Datadog, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze DDOG stock on TIKR for Free →