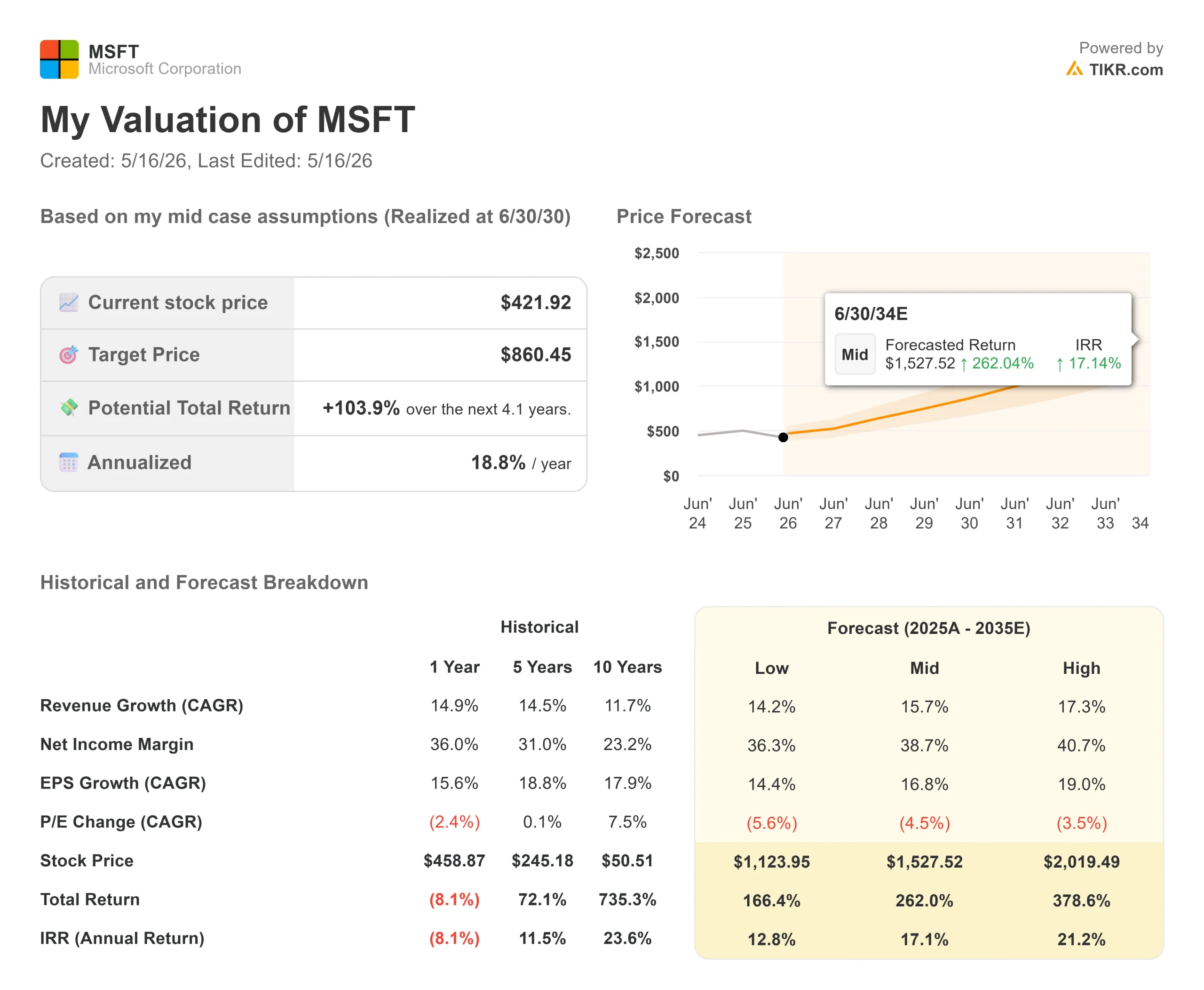

Key Stats for Microsoft Stock

- Current Price: $421.92

- Target Price (Mid): ~$860

- Street Target: ~$562

- Potential Total Return: ~104%

- Annualized IRR: ~19% / year

- Earnings Reaction: -3.93% (April 29, 2026)

- Max Drawdown: -34.18% (March 27, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Microsoft Corporation (MSFT) reported one of its cleanest quarters in years on April 29, and the stock fell anyway. Revenue of $82.9 billion beat consensus. EPS of $4.27 beat the $4.06 analyst estimate, per TIKR’s Beats & Misses data. Azure grew 40%. The annual recurring revenue from the AI business crossed $37 billion, up 123% year-over-year. The stock still dropped 3.93% because CFO Amy Hood guided for roughly $190 billion in calendar-year 2026 capital expenditures.

That reaction is understandable. It is also likely wrong about what matters most.

The bigger story from the April 29 call is not the size of the infrastructure bill. It is the architecture of how Microsoft gets paid. CEO Satya Nadella said it plainly on the call: “Any per-user business of ours, whether it’s productivity, coding, security, will become a per-user and usage business.” That is a structural change to Microsoft’s revenue ceiling, and it received almost no attention in the post-earnings coverage.

See historical and forward estimates for Microsoft stock (It’s free!) >>>

The Seat Ceiling Is Disappearing Across Three Categories

For most of Microsoft’s history, commercial software revenue was capped by headcount. More employees meant more seats. Fewer meant fewer. Predictable and sticky, but structurally limited.

That model is now being dismantled across three product lines at once.

GitHub Copilot, used by nearly 140,000 organizations, moved to full consumption-based pricing on June 1, 2026. Enterprise subscribers nearly tripled year-over-year, per Nadella’s prepared remarks. As developers use it more intensely, Microsoft earns more from the same customer with no new contract required.

In customer service, nearly 60% of Dynamics 365 service customers are already purchasing usage-based credits on top of their seats. Nadella cited HSBC as a live example: the bank deployed Dynamics 365 agents to manage customer inquiries and reduce issue resolution time by more than 30%.

In productivity, the Copilot credit consumptive offer, which lets companies build custom agents on top of Microsoft 365 Copilot, grew nearly 2x quarter-over-quarter. Paid M365 Copilot seats crossed 20 million, and customers like Accenture (740,000 seats), Bayer, Johnson & Johnson, Mercedes, and Roche (each committing to 90,000 or more seats) are not at the start of their usage curve. Nadella noted that weekly Copilot engagement is now at the same level as Outlook.

A pure seat model caps revenue at price times headcount. A seat-plus-consumption model expands revenue per customer as usage grows, with no new sales needed. That difference is what the capex debate keeps obscuring.

The OpenAI Restructure Removed a Hidden Drag

On May 13, 2026, Microsoft and OpenAI amended their partnership. The headline that OpenAI can now distribute its models through rival cloud providers was read as a loss of exclusivity. The actual structure is more favorable for Microsoft.

Under the prior arrangement, Microsoft shared Azure-generated revenue with OpenAI each time it licensed OpenAI models to cloud customers. The revised deal eliminates that revenue share on Azure sales, improving the margin on every AI workload Microsoft serves. Wedbush analyst Daniel Ives, who raised his MSFT price target to $575 with an Outperform rating following the announcement, called this the removal of a “meaningful drag” on Azure’s AI monetization. Wedbush also reported that Microsoft is set to receive approximately $6 billion from OpenAI in 2026, up from a prior estimate of roughly $4 billion, as the new structure accelerates payment timing.

Microsoft also locked in royalty-free access to OpenAI’s IP through 2032 and retained its equity stake. CFO Amy Hood confirmed on the earnings call that the revenue share from OpenAI continues through 2030. The exclusivity Microsoft gave up was largely theoretical. The margin improvement is immediate.

What the Valuation Multiples Show

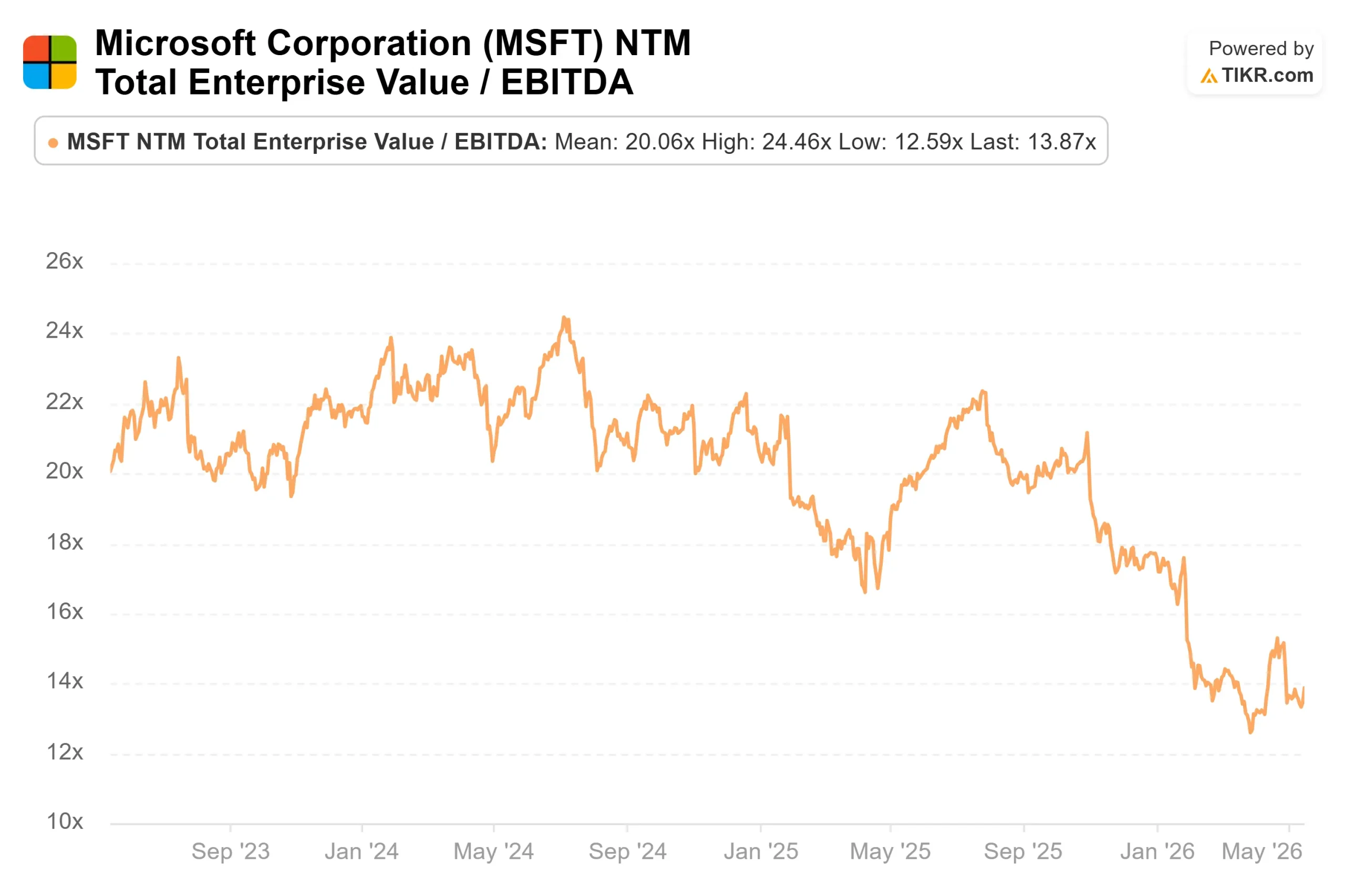

Microsoft trades at 13.87x NTM EV/EBITDA, per TIKR’s Competitors data as of May 15, 2026. For context, Salesforce trades at 8.25x with a narrower AI revenue base, and ServiceNow trades at 14.74x. Palo Alto Networks, priced for pure-play AI security growth, trades at 49.75x. Microsoft’s 13.87x sits below its own recent history; the NTM P/E ratio of 22.80x is well below the 27.18x the stock carried in March 2025, per TIKR Multiples data and prices in almost none of the consumption revenue layer now building across its three largest categories.

See how Microsoft performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $421.92

- Target Price (Mid): ~$860

- Potential Total Return: ~104%

- Annualized IRR: ~19% / year

See analysts’ growth forecasts and price targets for Microsoft stock (It’s free!) >>>

The mid-case uses a revenue CAGR of around 16%, driven by two engines: Azure capturing enterprise cloud market share as AI workloads scale, and Microsoft 365 Copilot deepening monetization as the seat-plus-consumption model matures across its 20 million paid seat base. The margin driver is operating leverage in the Productivity and Business Processes segment, where net income margins are expected to expand to around 39% from 36% today as the infrastructure cycle peaks. TIKR’s consensus estimates show revenue reaching approximately $607 billion by fiscal 2030, up from $282 billion in fiscal 2025. LTM ROIC sits at 27.4%, compressed by the current capex cycle. As new capacity converts to productive revenue, that figure should recover.

The upside case is a company with $627 billion in commercial remaining performance obligations, $37 billion in AI ARR growing at 123%, and consumption revenue just beginning to layer on top of 20 million Copilot seats. The primary risk is timing. Hood confirmed supply will remain constrained through at least the end of calendar 2026. If consumption adoption stalls before usage credits scale meaningfully, the multiple stays compressed.

Conclusion

The number worth tracking at Q4 FY2026 earnings, expected around July 29, 2026, is not Azure’s growth rate; every analyst already has that modeled. The signal that matters is whether ARPU in M365 Commercial Cloud shows acceleration beyond the E5 seat upgrades that have driven it so far. If usage credits begin contributing meaningfully to ARPU in Q4, the consumption model is converting on schedule. If ARPU is flat despite seat adds, the structural thesis has not yet proven itself. That distinction will not appear in the revenue headline. It lives one level deeper in the segment disclosures, and that is where this story gets resolved.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Microsoft?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Microsoft, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Microsoft alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Microsoft on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!