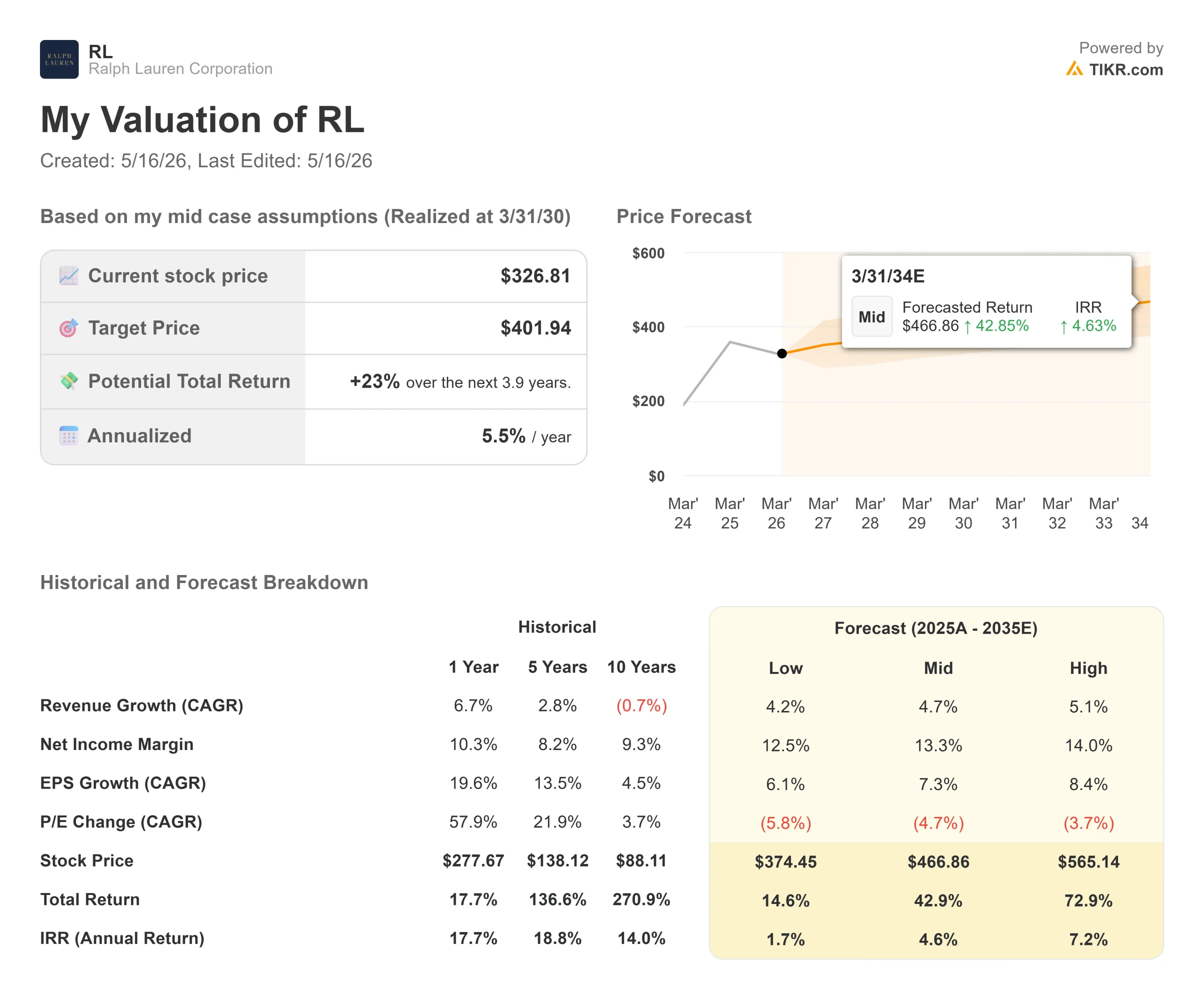

Key Stats for Ralph Lauren Stock

- Current Price: $326.81

- Target Price (Mid): ~$402

- Street Target: ~$414

- Potential Total Return: ~23%

- Annualized IRR: ~6% / year

- Earnings Reaction: +1.25% (February 5, 2026)

- Max Drawdown: -16.10% (5/15/26)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Ralph Lauren Corporation (RL) has been one of the strongest brand momentum stories in global apparel over the past three years. Then the stock hit a wall. Shares have fallen 16.10% from their 52-week high of $393.41 to $326.81, crossing below the 200-day moving average this week even as the company delivered its strongest holiday quarter in years, raised full-year guidance twice, and landed a cultural milestone few fashion brands ever achieve. This week, the U.S. Postal Service named Ralph Lauren to curate its American Icons stamp collection, honoring America’s 250th anniversary, the first time in USPS history that a single individual has overseen a complete official stamp issuance.

The market’s response? The stock kept falling.

That disconnect is the central question heading into Q4 FY2026 earnings on May 21. Citi upgraded RL to Buy in late March, calling the year-to-date selloff an “attractive buying opportunity” with a $400 target. BTIG raised its target to $450 in May. BofA moved to $450 in April. UBS sits at $480. Per TIKR, the Street’s mean target sits at $414.26, roughly 27% above the current price.

So is the fear rational, or is this a buying opportunity?

What the Selloff Is About

The concern is specific: tariffs and near-term margin compression.

On the February 5 Q3 earnings call, CFO Justin Picicci was direct. Tariffs are expected to be “a meaningful gross margin headwind through the first half of next fiscal year” until the company laps the higher cost base. For Q4 FY2026, management guided operating margin to contract 80 to 120 basis points in constant currency, driven by higher U.S. tariffs, marketing spend timing for the Milan fashion show and Winter Olympics, and strategic reductions in off-price sales. That margin contraction guidance, in one of the year’s smallest revenue quarters, is what rattled investors who had priced in uninterrupted expansion.

The secondary concern is North American wholesale. Picicci acknowledged Saks has been consolidating but was explicit that Ralph Lauren’s net exposure is “minimal, reflecting our disciplined and proactive management of the account.” The company is also deliberately pulling back from off-price channels, the right long-term call, but one that creates near-term noise in the revenue line.

See historical and forward estimates for Ralph Lauren stock (It’s free!) >>>

Why Bulls Think the Selloff Is Overdone

Start with average unit retail (AUR), which measures real pricing power. In Q3, AUR grew 18%, well ahead of original high-single-digit guidance. Picicci explained the driver: “The reduction in discounting was the primary driver of that AUR growth coming in at high teens for the quarter ahead of the original expectation.” The brand did not need to discount to move product across all three regions. Picicci described this as building on what management says is more than eight years of consistent AUR growth, with runway still remaining in every region.

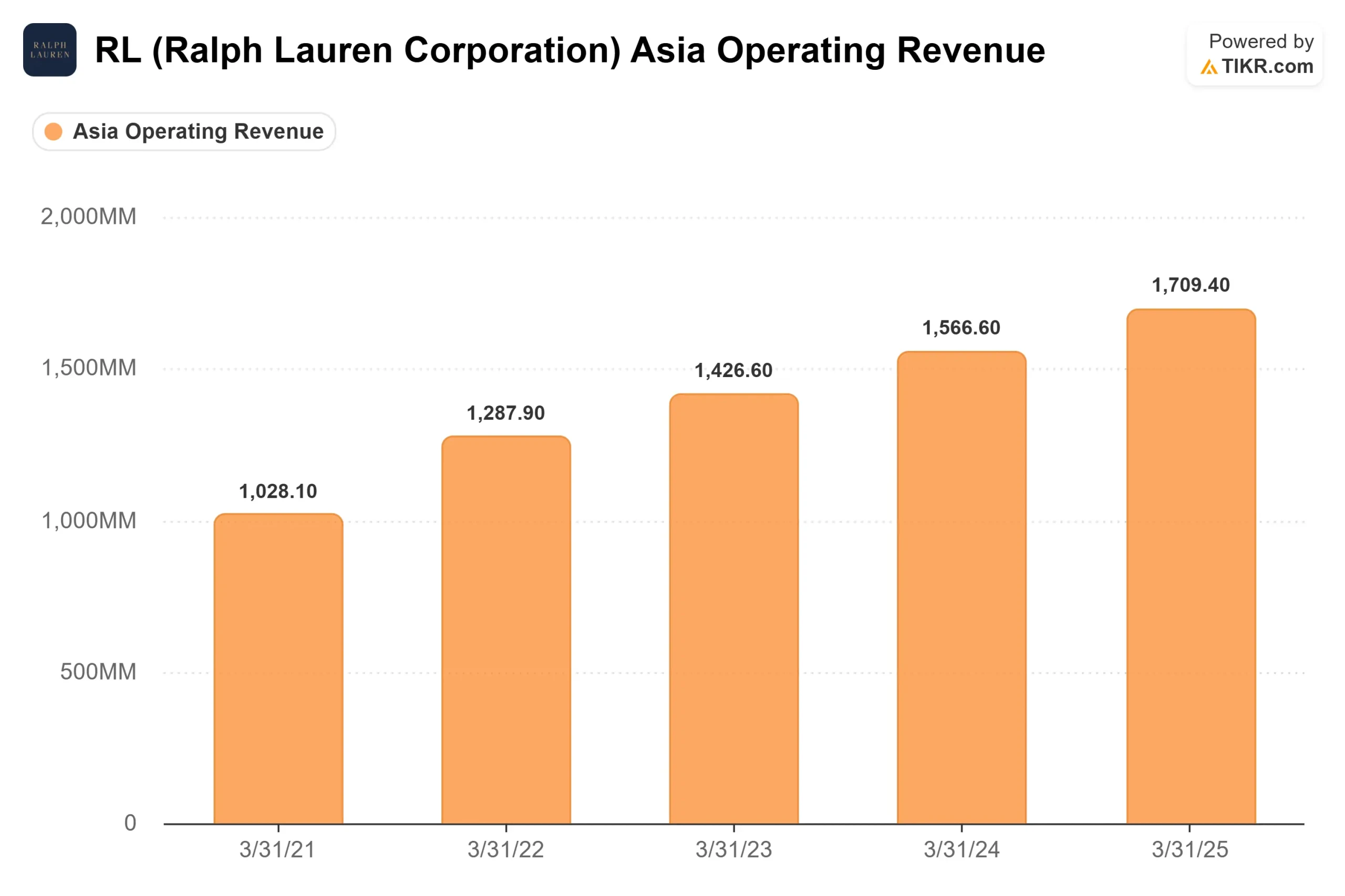

Asia is the other engine. Q3 revenue grew 22% in the region, led by China at more than 30%, ahead of management’s own outlook per the earnings call. CEO Patrice Louvet described Asia as structural rather than cyclical: “We have meaningful geographic white space, which we are developing with a thoughtful approach to our top cities.” The company added 2.1 million new direct-to-consumer (DTC) consumers in Q3, surpassing the prior year’s record of 1.9 million, led by younger shoppers and women.

Beyond the numbers, Louvet’s framing of how Ralph Lauren builds its brand matters. “Ralph is really much more like a movie director, think Martin Scorsese or Steven Spielberg, than he is a traditional designer.” The brand constructs cultural moments, Team USA at the Milan Cortina Winter Olympics, the Lando Norris Formula One partnership, and the USPS American Icons collection that sustain consumer engagement independent of any fashion trend. That cultural accumulation is increasingly difficult to replicate and compounds over time.

Competitor Context

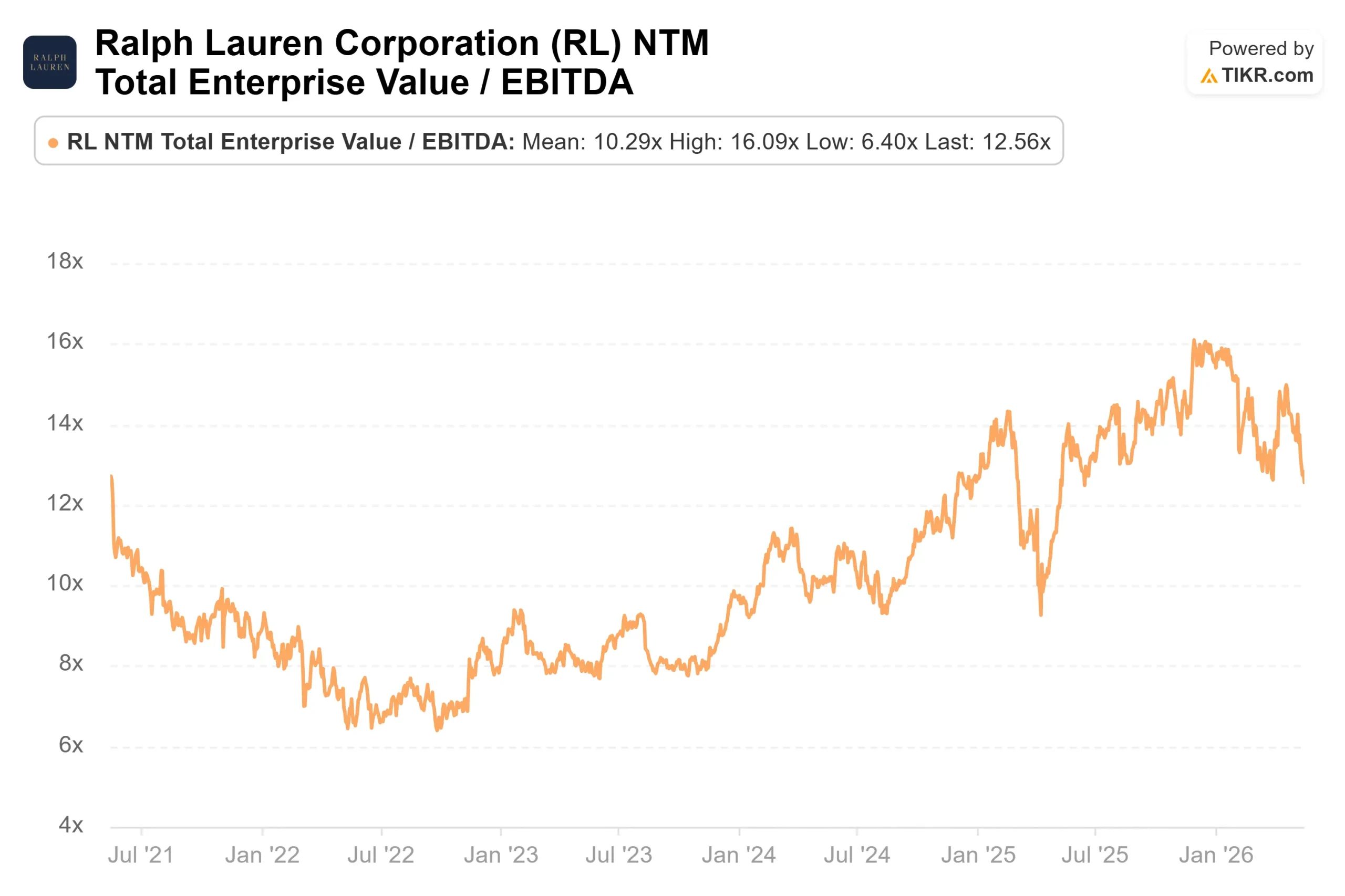

At 12.56x NTM EV/EBITDA, per TIKR, Ralph Lauren sits above Adidas at 9.08x and lululemon at 5.37x, but well below Hermès at 19.92x and Richemont at 14.87x. For a brand generating a 69.6% LTM gross margin and a DTC-led model that added 2.1 million new customers in a single quarter, the distance to true luxury house valuations looks increasingly narrow, which is exactly what the recent wave of analyst upgrades has been pricing in.

See how Ralph Lauren performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $326.81

- Target Price (Mid): ~$402

- Potential Total Return: ~23%

- Annualized IRR: ~6% / year

See analysts’ growth forecasts and price targets for Ralph Lauren stock (It’s free!) >>>

The TIKR mid-case assumes a revenue CAGR of around 5% to 3/31/30, driven by two engines: Asia expansion as the brand deepens its presence in top cities globally, and DTC mix shift as full-price digital and flagship store comps displace off-price volume that the company is deliberately shedding. The mid-case net income margin assumption is around 13%, supported by AUR gains and operating leverage from the channel mix shift.

The downside scenario matters too. If revenue growth slows to around 4% CAGR and margins stagnate near 12.5%, the TIKR model points to around $374 by 3/31/30, only about 15% total upside, which is uncompelling given the tariff and macro uncertainties required to produce that outcome.

The balance sheet offers meaningful support either way. LTM net debt to EBITDA sits at just 0.30x per TIKR, giving management the flexibility to keep investing in Asia store openings and digital infrastructure through the tariff headwind rather than pulling back.

Conclusion

The key data point arrives on May 21. Management has set a relatively low bar: mid-single-digit constant currency revenue growth and operating margin contraction of 80 to 120 basis points. Per TIKR’s Beats & Misses data, RL has beaten consensus estimates on revenue, EBITDA, and EPS in each of the past five quarters. If that pattern holds on May 21, the narrative shifts quickly from “is the selloff justified” to “why did investors sell.”

Watch two numbers: if Q4 adjusted operating margin contracts less than 80 basis points in constant currency and Asia sustains double-digit growth, the tariff story starts to look like a temporary reset. If margins come in at the worst end of guidance or below, the stock likely needs more time before the mid-case target of ~$402 becomes a realistic near-term destination.

The USPS stamp collection launches June 9. The brand’s cultural equity keeps compounding. The question is whether investors are willing to wait five days and then a few quarters to find out.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Ralph Lauren?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Ralph Lauren, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Ralph Lauren alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Ralph Lauren on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!