Key Stats

- Current Price: $85 (May 15, 2026)

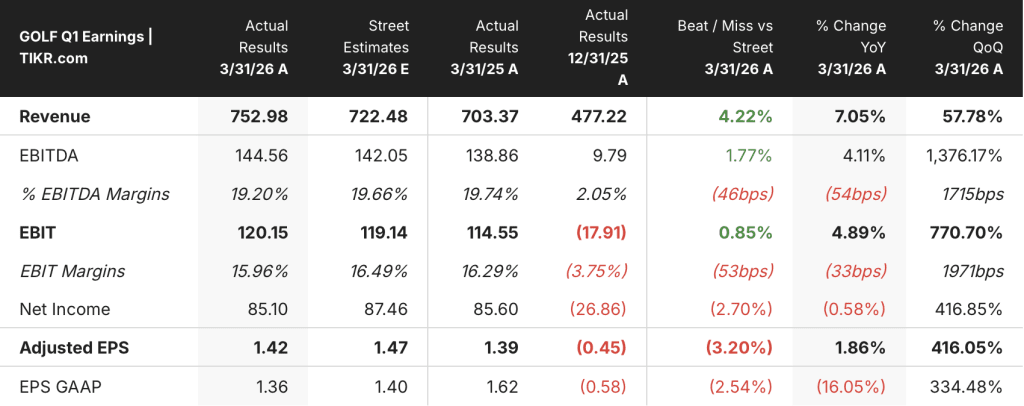

- Q1 2026 Revenue: $753M, +7% YoY (reported); +5% constant currency

- Q1 2026 Adjusted EBITDA: $145M, +4% YoY

- Q1 2026 Adjusted EPS: $1.42, +$0.03 YoY

- Full-Year 2026 Net Sales Guidance: $2,625M to $2,675M (maintained)

- Full-Year 2026 Adjusted EBITDA Guidance: $415M to $435M (maintained)

- TIKR Model Price Target: $116

- Implied Upside: ~35%

Acushnet Stock Delivers a Clean Q1 Beat as Titleist Momentum Holds

Acushnet Holdings (GOLF) posted Q1 2026 revenue of $753M, up 7% year over year on a reported basis and up 5% on a constant currency basis.

Adjusted EBITDA came in at $145M, a $6M increase from Q1 2025, with adjusted EPS of $1.42 versus $1.39 a year earlier.

Titleist Golf Equipment was the headline driver, with segment sales up 7% in the quarter on the strength of both balls and clubs.

Golf ball volumes increased across all regions as Acushnet launched new Pro V1x Left Dash, AVX, Tour Soft, and Velocity models, a notably strong result in an even year when modest volume declines against the prior Pro V1 launch cycle are typically expected.

Titleist Golf Clubs contributed as well, led by the Vokey SM11 wedge launch and continued demand for GT drivers and fairway metals in their second year on the market.

Golf Gear added 8% growth in the quarter, driven by higher bag volumes and double-digit gains in the U.S. and EMEA.

FootJoy posted a 1% decline, with gross margin for that segment still absorbing $17M in year-over-year tariff costs, according to CFO Sean Sullivan on the Q1 earnings call.

The most significant forward development flagged on the call: Acushnet is accelerating its Titleist GTS metals launch from the typical Q3 window into Q2, with a global market launch set for June 11.

David Maher, President and CEO, noted on the Q1 earnings call that the shift places the driver into a peak selling window of May through July, rather than the seasonally softer Q3 window the company has historically used.

Acushnet maintained its full-year 2026 net sales guidance of $2,625M to $2,675M and adjusted EBITDA guidance of $415M to $435M, and now expects first-half results to track toward the high end of the company’s previously communicated mid- to high-single-digit growth range.

Tariff exposure remains the primary cost watch item: Acushnet previously flagged a $70M full-year tariff impact, of which $17M hit gross profit in Q1, but Sullivan indicated on the call that recent developments, including the Supreme Court ruling on IEEPA tariffs, could prove favorable, though the net benefit is not yet quantifiable.

Acushnet returned $26M to shareholders in Q1 through $16M in dividends and $10M in buybacks, and the board declared a quarterly dividend of $0.255 per share payable June 22.

Acushnet Stock: What the Income Statement Shows

Acushnet stock’s income statement tells a margin-under-pressure story where the top line remains healthy but tariff-driven cost absorption is compressing profitability at the gross level.

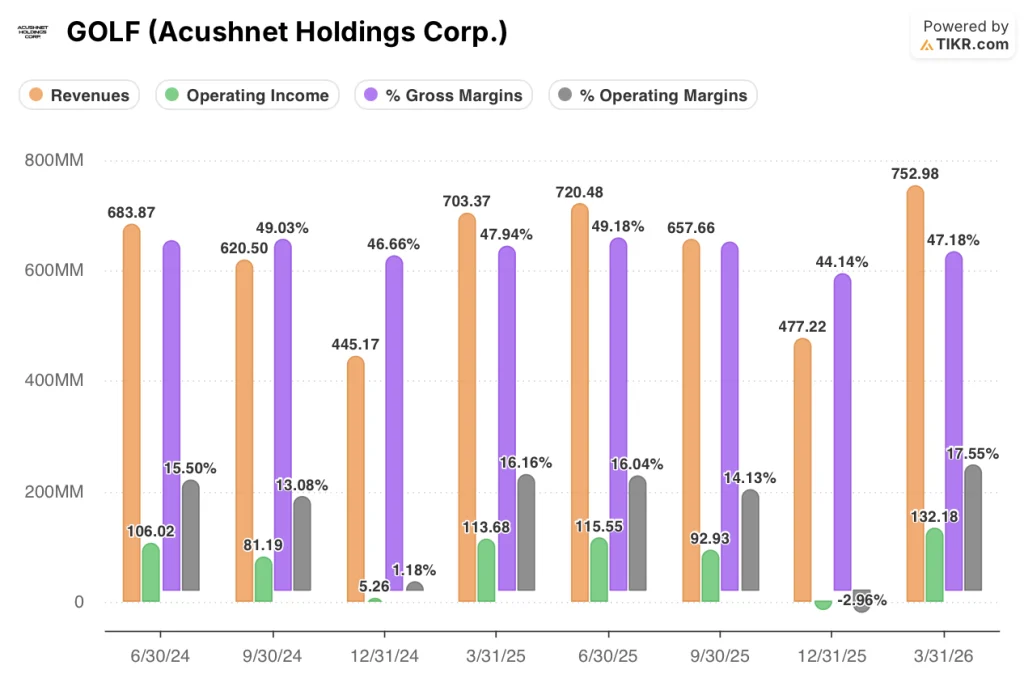

Revenue has run at $683M, $620M, $445M, $703M, $720M, $658M, $477M, and $753M across the eight quarters ending March 2026, showing the business’s pronounced seasonality with Q1 reliably the largest quarter of any calendar year.

Gross margin came in at 47% in Q1 2026, down from 48% in Q1 2025, with Sullivan attributing 220 basis points of that compression directly to tariff costs on the call.

Operating income of $132M in Q1 2026 was up 16% from $114M in Q1 2025, reflecting the leverage Acushnet generates when revenue scales in its seasonally peak quarter.

Operating margin expanded to 18% in Q1 2026 from 16% in Q1 2025, a meaningful reversal from the (3%) operating margin posted in Q4 2025, which is consistently the company’s weakest quarter due to seasonal volume lows.

The trend over the last four Q1 periods shows operating margin holding in a 15% to 18% range, with the Q1 2026 reading at the high end, suggesting that volume growth and cost discipline are partially absorbing the tariff headwind at the operating level even as gross margin compresses.

What Does the Valuation Model Say?

TIKR’s model prices Acushnet stock at $115.50 against a current price of $85.40, implying approximately 35% total upside over the next 5.6 years, or 7% annualized.

The mid-case model assumes a 2.3% revenue CAGR and an 8.8% net income margin, modest assumptions that reflect the relatively defensive, slow-growth nature of the premium golf equipment market.

The model also embeds a mild P/E compression assumption of (0.3%) annually in the mid case, meaning the implied upside relies almost entirely on earnings growth rather than any multiple expansion.

This earnings report does not materially change the risk/reward picture but provides mild confirmation that the mid-case path remains intact: revenue grew 7%, EBITDA grew 4%, and full-year guidance was held without revision.

Acushnet stock’s investment case is roughly unchanged, with the GTS metals launch timing shift representing a modest near-term catalyst that the model does not yet reflect.

The real question for Acushnet stock is whether an accelerated GTS metals launch into a peak selling window delivers incremental full-year revenue, or simply redistributes what Q3 would have captured.

What Has to Go Right

- GTS metals sell-through in the June 11 launch window must exceed historical Q3 launch sell-through rates to make the pull-forward accretive to the full year rather than merely a timing shift

- Tariff relief from the IEEPA Supreme Court ruling and Section 122 changes must offset the remaining full-year tariff headwind, which was previously sized at $70M

- Golf Gear’s 8% Q1 growth must sustain into Q2 as the peak season opens across the Northeast, Midwest, and Europe, where rounds of play were up 5% in the U.S. through March

- FootJoy must recover from its 1% Q1 decline as new Pro/SL and Premier shoe launches build sell-through momentum and tariff absorption moderates in the back half

What Could Still Go Wrong

- If GTS metals sell-through in Q2 disappoints relative to historical Q3 volumes, Acushnet would face a gap in H2 revenue with no major equipment launch to fill it

- Raw material and freight cost inflation, flagged by Sullivan on the call as a partial offset to any tariff relief, could compress gross margin further below the 47% Q1 reading

- Korea was down 7% in Q1 due to launch calendar timing, and any sustained weakness in that market as the club launch cycle normalizes would weigh on international segment results

- The net leverage ratio of 2.3x at Q1 end slightly exceeds Acushnet’s 2.25x average target, limiting the pace of buyback activity from the $231M remaining under the current authorization

Should You Invest in Acushnet Holdings Corp.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Acushnet Holdings Corp. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Acushnet Holdings Corp. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze GOLF stock on TIKR for Free →