Key Stats

- Current price: ~$8 (as of May 15, 2026)

- Q1 2026 revenue: $1.1B, +11.1% reported YoY; +5.1% organic constant currency

- Q1 2026 adjusted EPS: $0.15 vs. $0.10 guidance and consensus

- Q1 2026 adjusted EBITDA: $225M, +19.1% YoY; margin expanded 150 bps to 21%

- Full-year 2026 revenue guidance: ~6.4% to 6.7% reported growth (revised up)

- Full-year 2026 adjusted EPS guidance: $0.95 to $0.99

- Full-year 2026 adjusted EBITDA guidance: +14% to 16%; margin of 23.5% to 23.8%

- TIKR model price target: ~$13 (mid case, realized 12/31/31)

- Implied upside: ~63% over 5 and a half years (11% annualized)

NIQ Global Intelligence Stock Q1 2026: Earnings Breakdown

NIQ Global Intelligence stock (NIQ) opened its post-IPO earnings history with a Q1 beat: adjusted EPS came in at $0.15 against guidance and consensus of $0.10, while revenue reached $1.1B, growing 11.1% on a reported basis and 5.1% on an organic constant currency basis, exceeding the top end of the company’s guidance range.

The Americas segment led growth, posting 9.3% organic constant currency revenue expansion driven by both Intelligence and Activation.

Americas adjusted EBITDA reached $123M, though margins held flat year over year, with management attributing the mismatch to timing-related expense allocations expected to normalize through the rest of 2026.

EMEA delivered 4.6% organic constant currency revenue growth and was the margin standout for the quarter: adjusted EBITDA grew 24% to $155M, with margins expanding 270 basis points to 32%.

APAC remained a work in progress, declining 3.6% on an organic constant currency basis, though management noted early traction from retailer partnership investments in China and Japan, and adjusted EBITDA still grew 10.1% to $35M, with margins expanding 230 basis points to 23%.

eCommerce revenue accelerated to 33% growth in Q1, which CFO Mike Burwell cited on the call as a meaningful contribution to the overall revenue algorithm alongside value-based pricing and cross-sell.

Annualized Intelligence subscription revenue reached $2.9B, growing 5.9%, with net dollar retention at 104% and gross dollar retention improving to 99%.

Management reported closing 17 seven-figure wins in Q1 averaging three years in duration, including win-backs of a major global beverage manufacturer in both Americas and Southern Europe.

CEO Jim Peck disclosed that a leading global management consulting firm renewed its NIQ relationship at a 50% price increase, which he cited as reflecting the mission-critical role NIQ’s data plays in client workflows.

More than 70 clients have embedded NIQ’s AI-native solutions, BASES AI Screener and Product Developer, into their workflows since launch less than a year ago, with more than 2,300 product concepts tested across 27 countries.

The 2026 cost restructuring program generated approximately $80M in one-time charges in Q1, of which $55M was tied to the restructuring initiative announced in February; management now expects $70M to $80M in annualized run-rate savings.

Full-year 2026 guidance was revised upward for reported revenue and adjusted EBITDA, primarily on favorable foreign exchange movements, while organic constant currency guidance of 5.0% to 5.3% remained unchanged.

Q2 guidance calls for organic constant currency growth of 4.9% to 5.2% and adjusted EPS of $0.19 to $0.21, with management noting that April organic constant currency growth was already running ahead of Q1.

NIQ Stock Financials: Operating Leverage Arriving from a Low Base

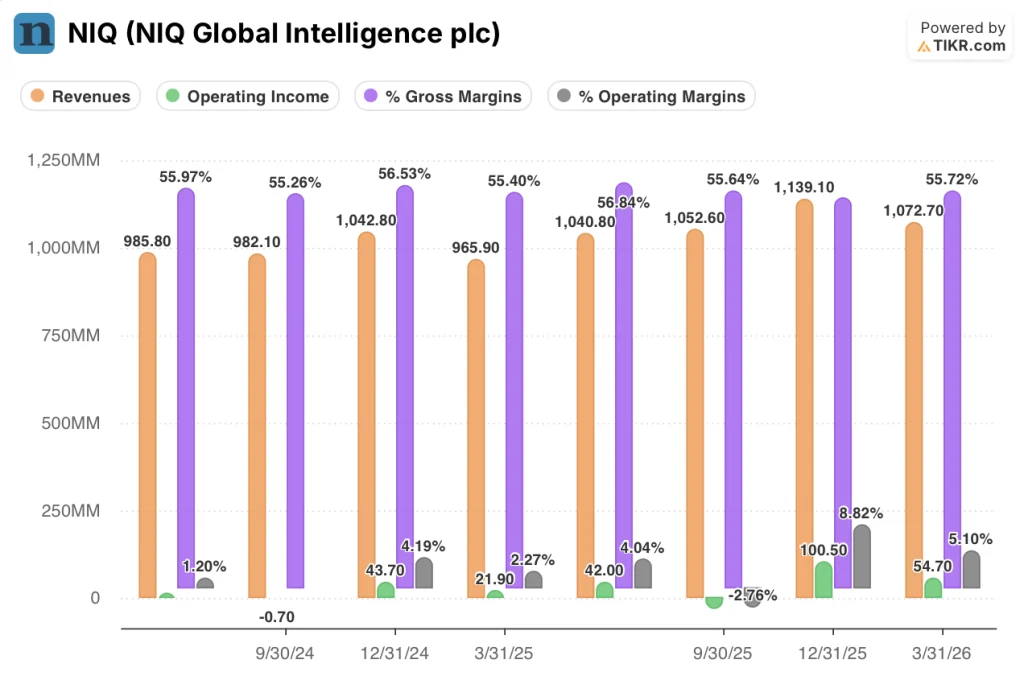

The NIQ Global Intelligence income statement tells a recovery story: operating income has swung from near zero in mid-2024 to meaningful positive territory by Q1 2026, even if the trajectory remains uneven.

Revenue grew consistently across the eight quarters shown: from $986M in Q2 2024 to $1.1B in Q1 2026, with the YoY growth rate accelerating from 0.4% in Q1 2025 to 11.1% in Q1 2026.

Gross margin has been stable throughout, ranging between 55% and 57% across all eight quarters, settling at 56% in Q1 2026.

The operating margin story is where the leverage has started to show: operating income was essentially flat in Q2 and Q3 2024, turned negative briefly in Q3 2024 at (0.1%), and recovered to 4.2% by Q4 2024.

The quarterly swing has continued in 2025 and into 2026: Q1 2025 operating margin was 2.3%, Q2 2025 reached 4.0%, Q3 2025 fell back to (2.8%) on restructuring charges, and Q4 2025 expanded to 8.8% as the cost program began taking effect.

Q1 2026 operating income landed at $55M with a 5.1% margin, down sequentially from Q4 2025’s 8.8% but 150 basis points above the prior year’s Q1 2025 level of 2.3%.

Management attributed adjusted EBITDA margin expansion of 150 basis points in Q1 to disciplined cost management, operating leverage, and early benefits from AI-enabled automation within the 2026 productivity initiatives.

What Does the Valuation Model Say?

The TIKR model prices NIQ Global Intelligence stock at ~$13 in the mid case, realized by December 2031, implying approximately 63% total upside from the current price of ~$8, or 11% annualized.

The mid case assumes a revenue CAGR of 5.3%, a net income margin of 8.8%, and EPS growth of 26%, with a P/E multiple compressing at a CAGR of (12.2%) over the forecast period.

That compression assumption is the tension at the center of the model: NIQ stock is priced for meaningful multiple contraction even in the scenario that reaches $13, which reflects how much of the upside depends on earnings growth rather than any re-rating.

Q1’s EPS beat (50% above guidance) and the trajectory of APAC’s turnaround both reduce downside risk near term, but the APAC drag and restructuring noise still make the path to sustained mid-20s EBITDA margins the key variable separating the mid and low cases.

The investment case for NIQ stock is incrementally stronger after Q1, not because the model changed, but because the company delivered ahead of expectations in its first quarter as a public company.

NIQ stock’s investment thesis hinges on whether the margin expansion already underway continues without being derailed by macro pressure on client budgets or APAC execution risk.

What Has to Go Right

- EBITDA margin must reach 23.5% to 23.8% for full-year 2026, as guided, requiring continued cost discipline after $80M in Q1 restructuring charges and $55M attributable to the 2026 program

- APAC must stabilize and contribute positively by H2 2026; management cited early retailer partnership wins in China and Japan but the region still declined 3.6% in Q1

- Subscription revenue growth of 5.9% annualized and 104% net dollar retention must hold as clients navigate tariff and macro uncertainty, particularly in EMEA and the Middle East

- Usage-based monetization from AI-native products (BASES AI Screener, Arthur AI Analyst) must begin contributing incremental revenue beyond current subscription layers

What Could Still Go Wrong

- The 2026 restructuring program now carries $65M to $75M in full-year charges, with incremental AI integration costs pushed into Q2, creating continued cash flow pressure at the seasonal low

- APAC continues to be a margin drag even as it recovers: a 3.6% organic constant currency decline represents a meaningful portion of NIQ’s global revenue base

- Americas adjusted EBITDA margins held flat year over year despite 9.3% organic revenue growth, with management citing timing-related expense allocations that have not yet resolved

- Net leverage of 3.4x remains elevated, and the company carries no share repurchase authorization while management acknowledges dissatisfaction with the stock’s current valuation

Should You Invest in NIQ Global Intelligence plc?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up NIQ Global Intelligence plc stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track NIQ Global Intelligence plc alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze NIQ stock on TIKR for Free →