Key Stats for CAVA Stock

- 52-Week Range: $43 to $99

- Current Price: $76

- Street Mean Target: $90

- Street High Target: $110

- Analysts Consensus: 13 Buys / 3 Outperforms / 12 Holds / 1 Sel

- TIKR Model Target (Dec. 2030): $205

What Happened?

CAVA Group (CAVA), the Mediterranean fast-casual restaurant chain built around customizable bowls and pitas, crossed $1 billion in annual revenue for the first time in 2025 while expanding its footprint to 439 locations across 28 states.

Full-year CAVA revenue grew 22.5% year over year to surpass the billion-dollar milestone, and same-restaurant sales increased 4% for the full year, a result management called the strongest new restaurant opening class in company history.

New restaurant productivity stayed above 100% for 2025, with new unit average unit volumes trending above $3 million, a figure that signals the brand’s demand is pulling ahead of even its own internal expectations.

Brett Schulman, Co-Founder and CEO, stated on the Q4 2025 earnings call that “our momentum reflects more than just expansion — it signals that our value proposition is resonating with today’s increasingly discerning consumer,” connecting CAVA’s pricing discipline (the company has taken less than half the price increases of industry peers while underpricing CPI by over 10%) directly to a widening competitive moat.

Heading into 2026, CAVA is launching its first-ever seafood offering in pomegranate-glazed salmon, entering new Midwest markets including Cincinnati and St. Louis, and targeting at least 74 to 76 net new restaurant openings as it tracks toward its goal of reaching 1,000 locations by 2032.

Argus Research downgraded CAVA stock to hold in late February, citing valuation concerns and flagging that same-restaurant sales metrics were “priced for perfection,” a counterpoint that frames the tension investors now face as CAVA stock sits 23% below its prior $99high.

Wall Street’s Take on CAVA Stock

The Argus downgrade crystallized the debate that now defines CAVA stock: the revenue growth and unit economics are structurally strong, but the market is no longer willing to pay the premium it once did, and the question is whether the current price reflects that discipline or a genuine mispricing.

CAVA’s revenue is forecast to grow around 26% year over year in Q1 2026, building on a two-year same-restaurant sales stack that accelerated sequentially every quarter of 2025, with management confirming that Q1 comps were tracking above the 3% to 5% full-year guidance range heading into the print.

Coverage has expanded to 29 analysts with a consensus of 13 Buys / 3 Outperforms / 12 Holds / 1 Sell and a mean price target of $90, implying around 18% upside from $76.09, with the high target at $110 and the low at $63, a spread that captures how divided the Street has become after a year in which CAVA stock fell 47% before partially recovering.

The $110 high target reflects the scenario where salmon drives a sustained traffic lift, AGM operational improvements compound through the year, and same-restaurant sales hold at the top end of guidance; the $63 low reflects the Argus view that slowing metrics and stretched valuation leave little margin for error.

The structural risk is same-restaurant sales deceleration below 3% sustained: if traffic softens as the promotional restaurant environment intensifies and salmon novelty fades, the restaurant-level margin recovery toward 25% becomes harder to deliver and the revenue compounding thesis loses its central support.

Q1 2026 earnings on May 19 are the first hard read on whether the salmon launch is driving incremental traffic above the low-to-mid-single-digit comp assumption, and the specific number to watch is same-restaurant sales relative to the 3% to 5% guidance band.

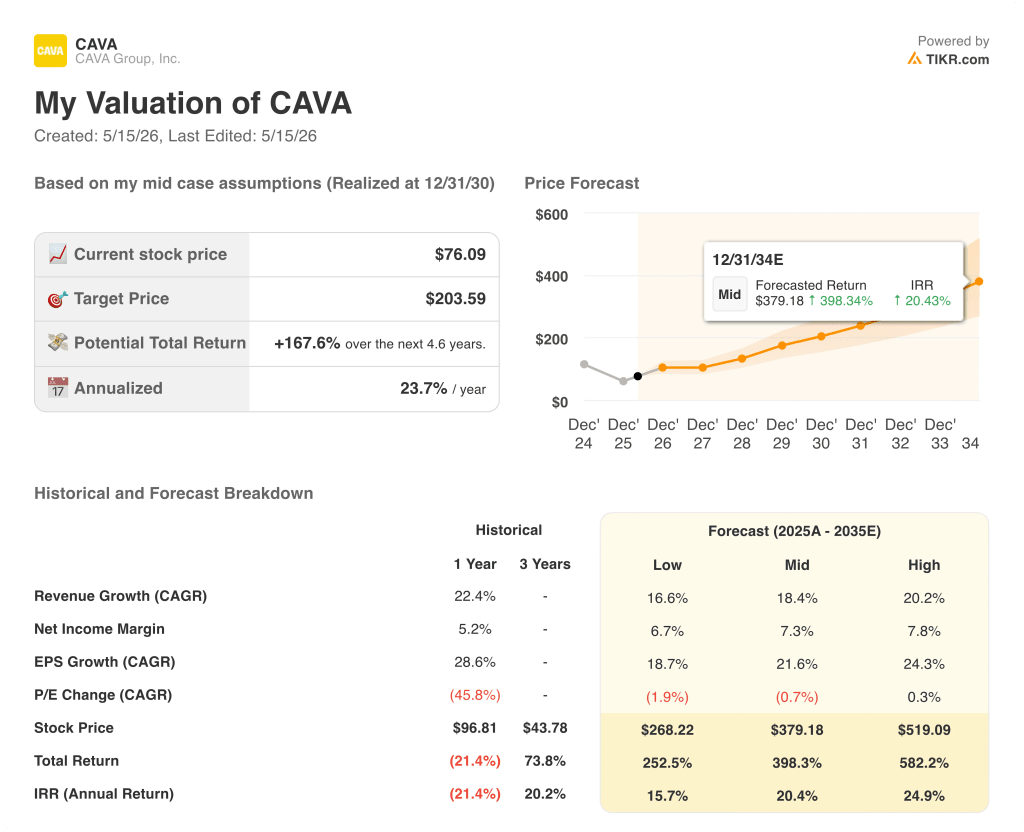

What Does the Valuation Model Say?

The TIKR mid-case model prices CAVA at $204, implying around 168% upside from $76.09, built on an 18% revenue CAGR through 2030 and net income margin expansion from 5.2% today toward 7.3% at maturity — assumptions that require the unit-growth model to execute without meaningful interruption across roughly 560 additional restaurant openings.

The argument hinges on one variable: whether CAVA’s same-restaurant sales can hold at or above 3% through 2026 while the company absorbs the operational complexity of scaling past 500 units, launching salmon, and building out a new field leadership structure simultaneously.

What Has to Go Right

- Same-restaurant sales sustain at 3% to 5% in 2026, validating the long-term algorithm in a consumer environment where peers like Chipotle have faced “slop-bowl fatigue” headwinds

- Pomegranate-glazed salmon drives incremental traffic without the margin headwind exceeding the guided 100 basis points, proving the menu platform can expand without degrading unit economics

- The AGM program (assistant general manager roles designed to deepen operational bench strength), 60% filled as of the Q4 call and targeting completion by mid-2026, supports new restaurant performance above 90% productivity

- EBITDA reaches around $180 in 2026, demonstrating operating leverage is real and that G&A investment is not fully consuming the scale benefits of 22%-plus revenue growth

- Brand awareness, which management noted grew from 55% to 62% over the past year, continues building as Midwest market entries generate new-market halo effects

What Could Go Wrong

- The Argus downgrade proves a leading indicator rather than a sentiment floor: same-restaurant sales fall below 3%, and the forward P/E CAGR of (1.9%) in the low case accelerates multiple compression toward the $63 low target

- Salmon operational complexity hits labor efficiency in ways the guided 100-basis-point margin headwind does not fully capture, compressing restaurant-level profit margins below the 23.7% guidance floor

- New restaurant productivity falls short of 90% as greenfield market entries in Columbus, Minneapolis, and St. Louis lack the brand awareness halo that drove 100%-plus productivity in established markets

- The leadership bench Brett Schulman described as “the biggest governor to our growth” cannot scale fast enough to maintain execution quality as CAVA pushes toward 100-plus annual openings beyond 2026

Should You Invest in CAVA Group, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CAVA Group, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track CAVA Group, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CAVA stock on TIKR for Free →