Key Takeaways:

- Freshworks beat Q1 2026 revenue estimates with around $229 million in revenue, up around 16% year over year

- The company is cutting 11% of its workforce as AI reshapes the broader software industry

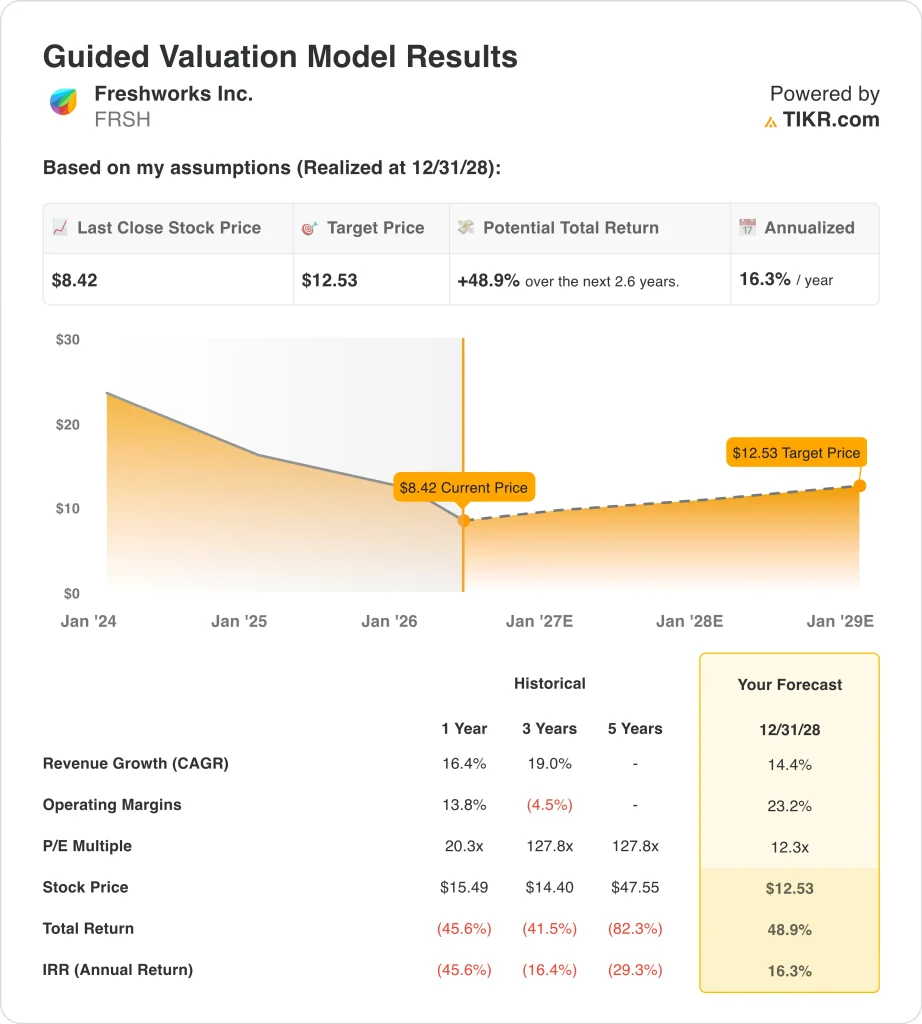

- FRSH stock trades near $8, well below its 52-week high of $16, and the analyst consensus target is near $12

- FRSH stock could rise from $8 to around $13 per share by December 2028

- That implies a total return of around 49%, or around 16% annualized over the next 2.6 years

What Happened?

Freshworks Inc. (FRSH) reported Q1 2026 results that beat estimates but came with a major restructuring announcement. Revenue reached around $229 million, up around 16% year over year. That beat analyst expectations of around $223 million. But the bigger headline was the company’s decision to cut 11% of its workforce. Management cited AI’s rapid transformation of software development as the main driver.

These job cuts reflect a broader industry trend, and Freshworks is moving quickly to adapt its cost structure for an AI-first world. The company expects a restructuring charge of $7 million to $9 million in Q2 2026 to cover these changes.

Investors are watching carefully to see whether leaner operations will lead to meaningful margin improvement in the second half of 2026. And the operating loss in Q1 narrowed to $8.1 million, which shows real progress even if profitability remains a work in progress.

CEO Dennis Woodside personally purchased 125,000 shares in March 2026, and that kind of insider buying signals leadership confidence in the stock’s value. The board authorized a $400 million share repurchase program in February 2026, so management is clearly acting on its belief that the stock is undervalued.

The stock has lost around 46% of its value over the past year, and the 52-week range runs from $7 to $16. Freshworks also appointed Ian Tickle as Chief Revenue Officer in March 2026, signaling a renewed focus on sales execution in key enterprise markets. The company hosted its Refresh 2026 product event in May, which typically drives pipeline momentum and customer engagement.

Here’s why Freshworks stock could deliver meaningful upside over the next several years as restructuring savings and AI product adoption drive profitability higher.

What the Model Says for FRSH Stock

We analyzed the upside potential for Freshworks stock based on its AI-integrated product portfolio, expected margin recovery from workforce restructuring, and sustained revenue growth in cloud-based customer support and IT service management software.

Based on estimates of 14.4% annual revenue growth, 23.2% operating margins, and a normalized P/E multiple of 12.3x, the model projects Freshworks stock could rise from $8 to around $13 per share by December 2028.

That would be a 48.9% total return, or a 16.3% annualized return over the next 2.6 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for FRSH stock:

1. Revenue Growth: 14.4%

Freshworks has beaten analyst revenue estimates consistently over recent quarters. Q1 2026 revenue of around $229 million topped estimates by about $6 million. The company grew revenue at around a 19% compound annual rate over the past 3 years, but growth is expected to moderate as the business matures and the competitive landscape intensifies.

Based on analysts’ consensus estimates, we used a 14.4% annual revenue growth rate. This reflects continued demand for AI-powered customer support and IT service management tools. It also accounts for competitive pressure from larger enterprise software vendors with deeper integration ecosystems.

The new Chief Revenue Officer and the Refresh 2026 product event both suggest management is prioritizing sales execution and innovation. Together, these factors support a mid-teens growth assumption through 2028, but consistent execution remains the most important variable.

2. Operating Margins: 23.2%

Freshworks posted an operating loss of $8.1 million in Q1 2026, but the trajectory is improving quickly. Gross margin remains strong at around 85%, which is high even by software industry standards. That high gross margin gives the company significant room to convert revenue into operating income as it scales.

Based on analysts’ consensus estimates, we used a 23.2% operating margin target. The 11% workforce reduction should materially lower operating expenses starting in the second half of 2026. AI-powered workflows are also expected to reduce support and engineering costs over time.

Reaching around 23% operating margins from a current operating loss position is ambitious. But it is consistent with the company’s improving cost structure and with what disciplined AI-driven software businesses have achieved historically.

3. Exit P/E Multiple: 12.3x

Freshworks currently trades at a next-twelve-months P/E of around 12x. That is low relative to most software peers and reflects compressed growth expectations over the past year. The multiple has contracted sharply as the market questioned the company’s path to sustained profitability.

Based on analysts’ consensus estimates, we maintained a 12.3x exit multiple. This is a conservative assumption that accounts for ongoing execution risk around the AI transition. It also reflects uncertainty about the timeline for reaching consistent profitability.

If the company delivers on its restructuring goals and re-accelerates growth, a meaningful multiple re-rating is possible. But for now, the model conservatively assumes the market will wait for proof of execution before rewarding the stock with a higher earnings multiple.

Build your own Valuation Model to value any stock (It’s free!) >>>

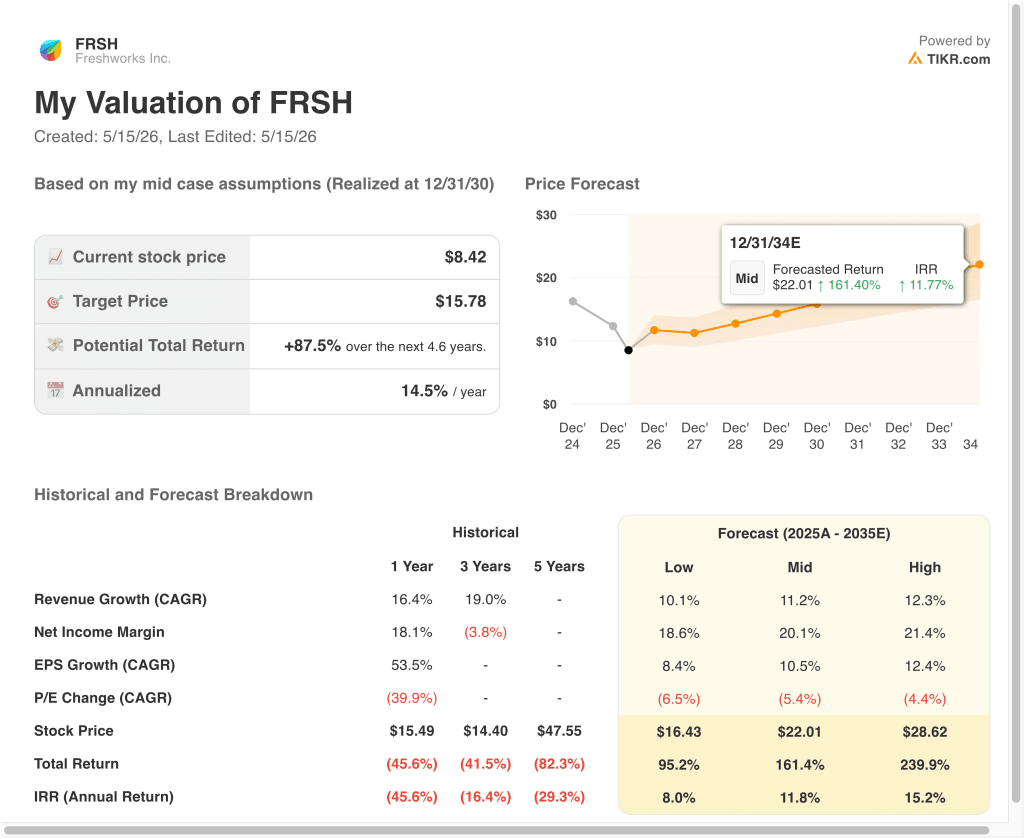

What Happens If Things Go Better or Worse?

Different scenarios for FRSH stock through 2035 show varied outcomes based on revenue growth, margin expansion, and AI product adoption (these are estimates, not guaranteed returns):

- Low Case: Revenue growth disappoints and restructuring savings materialize more slowly than expected → 8.0% annual returns

- Mid Case: AI products gain traction and margins expand as restructuring delivers savings → 11.8% annual returns

- High Case: Strong revenue growth and faster margin improvement drive a meaningful re-rating → 15.2% annual returns

Going forward, Freshworks is at a decisive turning point in its history as a company. The combination of significant insider buying, a large share repurchase program, and a new Chief Revenue Officer signals that management is serious about creating long-term shareholder value.

But the market will need to see consistent quarterly execution on profitability before rewarding the stock with a meaningfully higher multiple.

See what analysts think about FRSH stock right now (Free with TIKR) >>>

Should You Invest in Freshworks?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up FRSH, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track FRSH alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze the stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!