Key Stats for Chubb Stock

- 52-Week Range: $264 to $346

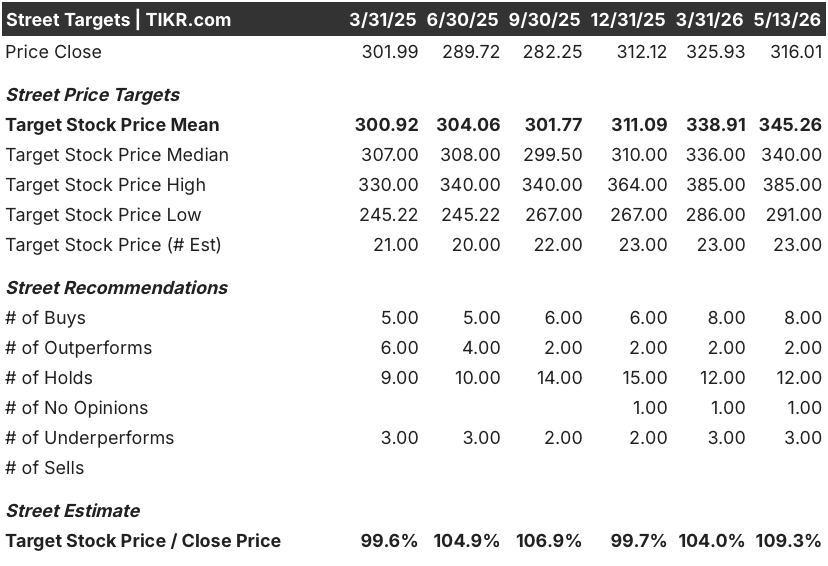

- Current Price: $316

- Street Mean Target: $345

- Street High Target: $385

- Analyst Consensus: 8 Buys / 2 Outperforms / 12 Holds / 1 No Opinion / 3 Underperforms

- TIKR Model Target (Dec. 2030): $

What Happened?

Chubb Limited (CB) is the world’s largest publicly traded property and casualty insurer, writing premiums across commercial, personal, and specialty lines in 54 countries.

The company reported Q1 2026 core operating earnings of $2.7 billion, or $6.82 per share, beating the Street estimate of $6.61 and surging 85.3% year over year as catastrophe losses collapsed from $1.64 billion in the prior-year period to $500 million.

The cat loss comparison is stark but the underlying business is the real story.

Excluding catastrophes entirely, core operating income grew 10.7% and EPS grew 13.5%, numbers that reflect genuine operational strength rather than a favorable year-over-year base.

Net premiums written rose 10.7% to $14.01 billion, with Life premiums up more than 33% and P&C growing 7.2%, driven by 14.4% growth in Overseas General and 8.3% growth in North America personal lines.

CEO Evan Greenberg described the quarter as “an excellent start to the year,” adding in the Q1 2026 earnings call that Chubb remains “confident in our ability to continue generating strong growth in operating earnings and double-digit growth in EPS and most important, tangible book value.”

That confidence is not unconditional.

Greenberg called out rapidly softening property pricing in shared and layered markets, noting that overall pricing in those segments was down about 25% in the quarter and “accelerating toward 30%,” which he described bluntly as “dumb.”

Chubb’s response was deliberate: the company non-renewed a substantial portion of large-account shared and layered property business it judged inadequately priced, shrinking that book voluntarily to protect underwriting quality.

Excluding that intentional pullback, total North America commercial premiums rose 7.7%, a figure that reframes the headline growth rate and signals where the real momentum sits.

On the investment side, adjusted net investment income reached $1.84 billion, up more than 10%, supported by a $170 billion invested asset base growing from $152 billion a year ago and a fixed income portfolio yielding 5.1%.

The Gulf shipping program adds a longer-dated optionality layer: Chubb is lead insurer on the U.S. International Development Finance Corporation’s $20 billion maritime reinsurance plan covering ships transiting the Strait of Hormuz, a program with the potential to generate material premium revenue if geopolitical conditions permit convoys to proceed.

The P&C combined ratio of 84% compares with 95.7% a year earlier, and on a current accident year ex-cat basis, the combined ratio was 82.1%, reflecting underwriting discipline that Greenberg said should continue to generate double-digit tangible book value growth.

Tangible book value per share already grew 21.5% in the quarter.

Wall Street’s Take on CB Stock

The Q1 beat resets the forward earnings trajectory at a higher base, and the ex-cat growth rate of 13.5% EPS makes the year-over-year comparison noise irrelevant to the underlying thesis.

Chubb’s EPS Normalized came in at $6.82 for Q1, up 85.3% year over year from the wildfire-impacted prior period, beating the Street estimate of $6.61 by 3.2%; on a full-year basis, consensus now sees EPS growing around 9% in the next twelve months as the ex-cat run rate compounds on top of Q1’s strong start.

Coverage tilts constructive: 8 Buy ratings and 2 Outperforms against 12 Holds and 3 Underperforms, with a mean price target of $345 implying 9.3% upside from the current price, and no analyst covering the name has a Sell on record.

The gap between the $291 low target and the $385 high target is wide enough to reflect a genuine debate, anchored on one side by investors who expect the property pricing cycle to create meaningful reserve stress and on the other by those who believe Chubb’s disciplined non-renewal strategy already inoculates the book.

Greenberg’s double-digit EPS and tangible book value growth guidance signals that management sees the current operating environment as sustainable despite property market softening, a conviction reinforced by the 20.6% annualized core operating return on tangible equity posted in Q1.

The key risk is a severe catastrophe event in Q2 or Q3 that reverses the favorable cat loss comparison and resets the combined ratio back above 90%.

Q2 2026 earnings, expected in late July, will be the first clean test of whether the ex-cat growth rate of 10%-plus can hold without the tailwind of a weak year-ago comparison.

What Does the Valuation Model Say?

The TIKR model targets Chubb stock at $430 in the mid case, built on a revenue CAGR of around 4% through 2030, a net income margin expanding to around 21%, and EPS growing at a CAGR of around 5%, implying a total return of around 36% over the next 4.6 years at an annualized rate of around 7%.

At $316, CB stock is priced at a discount to a mid-case intrinsic value that assumes no reacceleration in premium growth and only modest margin expansion from current levels, leaving Chubb stock undervalued for investors willing to hold through a property pricing cycle that Greenberg himself expects to correct within a relatively short timeframe given the pace of inadequate pricing currently entering the market.

The investment thesis hinges on a single question: does the property market softening stay contained to the large-account shared and layered segment Chubb is already exiting, or does competitive pressure bleed into the casualty and specialty lines where the company has pricing power?

Bull Case

- Ex-cat core operating EPS grew 13.5% in Q1 2026, demonstrating that the underlying earnings engine is intact independent of the catastrophe comparison

- Chubb’s North America commercial premiums grew 7.7% excluding purposely non-renewed large-account property, indicating that the voluntary book shrinkage is not a symptom of competitive pressure elsewhere

- The $170 billion invested asset base, up from $152 billion a year ago, earns at a 5.1% fixed income portfolio yield with a new money rate of 5.5%, creating an investment income tailwind that is structurally independent of underwriting cycles

- Casualty pricing remained up 9.6% in North America in Q1 2026, with rates up 8.4% and exposure growth of 1.1%, providing continued underwriting margin support in Chubb’s largest premium category

- The Gulf maritime reinsurance program represents a high-margin optionality premium stream that carries no additional capital commitment beyond the existing balance sheet

Bear Case

- Property pricing in shared and layered North America declined 25% in Q1 2026 and is accelerating toward 30%, creating reserve adequacy risk for competitors who continued writing at those levels and potentially seeding an industry-wide adverse development cycle

- The London wholesale market is also softening rapidly, with Chubb having already shrunk its open market property book there, limiting the company’s ability to redeploy the capital freed from the North America non-renewals into an equally attractive market

- Consensus EPS estimates project roughly flat sequential EPS through the middle of 2026, with Q2 and Q3 2026 NTM EPS estimates running around $6.28 to $6.68, implying no near-term acceleration and leaving the stock dependent on a clean catastrophe quarter to sustain the multiple

- Tangible book value growth of 21.5% in Q1 2026 was partially driven by reduced catastrophe losses from the prior year, a non-recurring dynamic that may not sustain if the 2026 Atlantic hurricane season proves active

- The 12x forward P/E entry point assumes the current softening cycle remains contained, but Greenberg’s own commentary noted that terms and conditions are already softening “on the margin,” a phrase that historically precedes more significant deterioration

Should You Invest in Chubb Limited?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Chubb Limited stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Chubb Limited alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CB stock on TIKR for Free →