Key Takeaways:

- Booking Holdings (BKNG) beat Q1 2026 earnings with adjusted EPS of $1.14 versus the $1.08 consensus, but cut its annual revenue growth forecast due to Middle East conflict impacts on bookings.

- The company completed a 25:1 stock split on April 6, 2026, and subsequently priced around $2.65 billion in new senior notes to strengthen its balance sheet.

- BKNG stock could reasonably reach around $312 per share by December 2030, based on our valuation assumptions.

- This implies a total return of around 101% from today’s price of $155, with an annualized return of 16.2% over the next 4.6 years.

What Happened?

Booking Holdings Inc. (BKNG) is the world’s leading online travel marketplace, operating Booking.com, Priceline, Kayak, Agoda, and OpenTable. The stock fell 27% year-to-date through mid-May 2026, as the ongoing Middle East conflict weighed on a high-value booking region. All share prices reflect post-split figures following the company’s 25:1 stock split on April 6, 2026.

In Q1 2026, the company delivered adjusted EPS of $1.14, beating the analyst consensus of $1.08. But management warned that the Middle East conflict would impact bookings through at least June 2026, and it cut its full-year revenue growth outlook as a result. So investors sold the stock despite the earnings beat, pushing it toward its 52-week low of $151.

The capital structure developments added important context. Booking priced EUR 1.9 billion in senior notes in May 2026 and separately priced $750 million in 5.375% senior notes due 2036. These moves extend the company’s debt maturity profile and reflect confidence in its long-term cash generation.

CEO Glenn Fogel spoke at the J.P. Morgan Technology, Media and Telecom conference in May 2026, reaffirming management’s confidence in the resilience of global travel demand. The current street consensus price target of $224 remains well above the current price of $155, suggesting analysts still see meaningful upside.

Competitor Expedia tumbled in May 2026 after flagging Middle East and Mexico travel demand headwinds. Airbnb also flagged second-quarter growth impacts from geopolitical disruptions. But Marriott raised its annual room revenue growth forecast during the same period, reflecting the bifurcated nature of travel demand.

Here’s why Booking Holdings stock could deliver attractive returns once geopolitical headwinds ease, and its dominant platform scale reasserts itself.

What the Model Says for BKNG Stock

We analyzed the upside potential for Booking Holdings stock based on its dominant platform scale across Booking.com and Priceline, resilient long-term global travel demand, and its highly profitable asset-light business model.

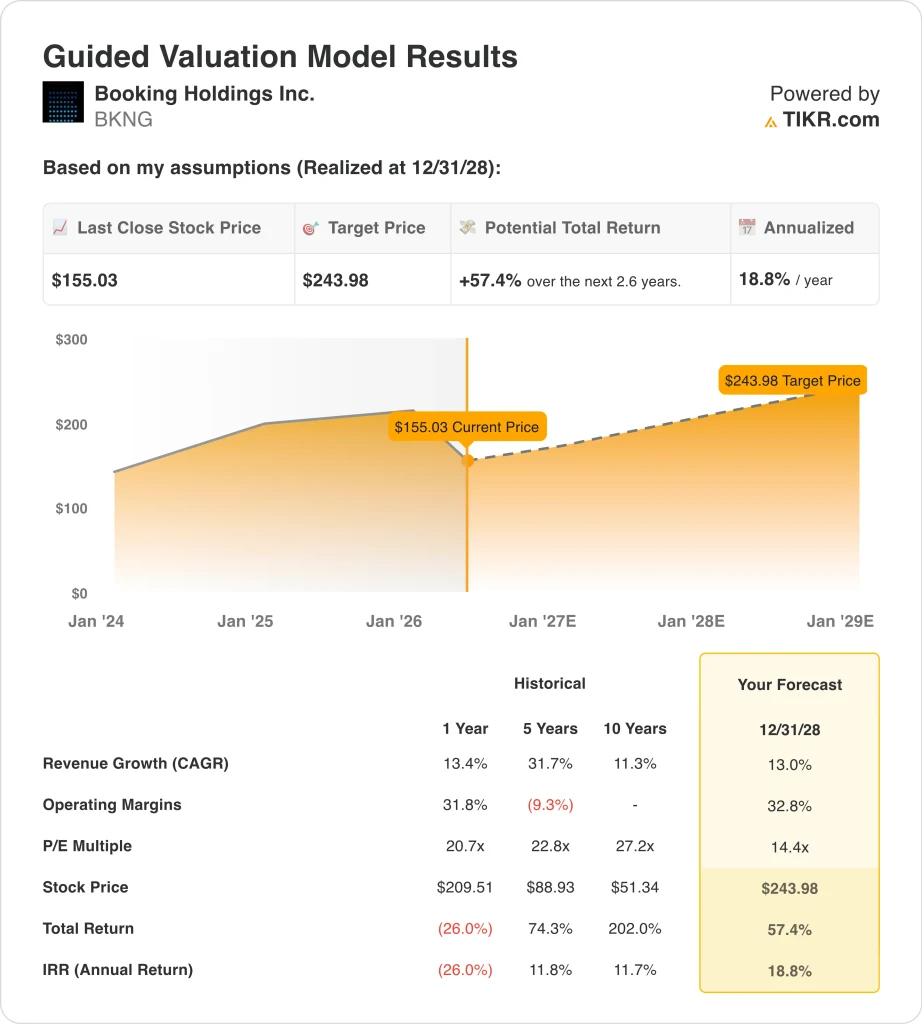

Based on estimates of 13.0% annual revenue growth, 32.8% operating margins, and a normalized P/E multiple of 14.4x, the model projects Booking Holdings stock could rise from $155 to around $244 per share.

That would be a 57.4% total return, or an 18.8% annualized return over the next 2.6 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for BKNG stock:

1. Revenue Growth: 13%

Booking Holdings grew revenue at a 13.4% CAGR over the past year, so a 13.0% growth assumption aligns closely with recent performance. The platform continues expanding its alternative accommodations inventory, attraction offerings, and AI-driven search and booking capabilities. But the Middle East conflict creates near-term revenue pressure that may persist through at least mid-2026.

Based on analysts’ consensus estimates, we used a 13.0% revenue growth forecast, reflecting Booking’s proven ability to grow through challenging macro periods while acknowledging current geopolitical headwinds in key booking regions.

The one-year revenue CAGR of 13.4% and the forward two-year CAGR of 9.2% together suggest a path of moderating but healthy growth as the initial post-pandemic travel surge normalizes.

2. Operating Margins: 32.8%

Booking Holdings delivered a 31.8% operating margin in the past year, and its asset-light model makes margins highly scalable. The company does not own the properties on its platform, so growth in bookings volume carries minimal incremental cost. But continued investment in AI personalization and new verticals like ground transportation and activities adds near-term spending.

Based on analysts’ consensus estimates, we used a 32.8% operating margin target, reflecting gradual improvement as the company scales its fixed cost base and benefits from AI-driven platform efficiency gains.

This target is also consistent with Booking’s historical operating margin range, suggesting it is achievable without requiring exceptional performance beyond what the business has already demonstrated.

3. Exit P/E Multiple: 14.4x

Booking Holdings currently trades at a forward NTM P/E of around 14.5x, which is historically low for a business with 87% gross margins and a globally recognized brand portfolio. The current multiple reflects near-term investor concern about geopolitical demand disruption and the company’s reduced growth guidance.

Based on analysts’ consensus estimates, we maintained a 14.4x exit multiple, acknowledging that this is a conservatively set P/E relative to Booking’s historical multiples that could expand if travel demand normalizes faster than currently expected.

So the valuation model benefits from both earnings growth and potential multiple expansion, which explains the 18.8% projected annual return from current prices.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for BKNG stock through 2034 show varied outcomes based on global travel demand recovery, platform monetization, and margin execution (these are estimates, not guaranteed returns):

- Low Case: Prolonged Middle East disruption and slower international travel recovery limit revenue growth → 11.2% annual returns

- Mid Case: Global travel normalizes, and platform scale drives steady revenue growth and margin improvement → 14.8% annual returns

- High Case: Strong global travel demand and AI-powered efficiencies drive above-consensus revenue and earnings growth → 18.2% annual returns

Going forward, Booking Holdings stock will likely track the resolution or escalation of the Middle East conflict and the pace of global travel recovery. The 27% year-to-date decline has pushed the stock toward its 52-week low and created what the model suggests is a compelling return opportunity under most scenarios. But near-term investors should remain aware that geopolitical headwinds could persist longer than currently anticipated.

See what analysts think about BKNG stock right now (Free with TIKR) >>>

Should You Invest in Booking Holdings?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up BKNG, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track BKNG alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze the stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!