Key Stats for Applied Materials Stock

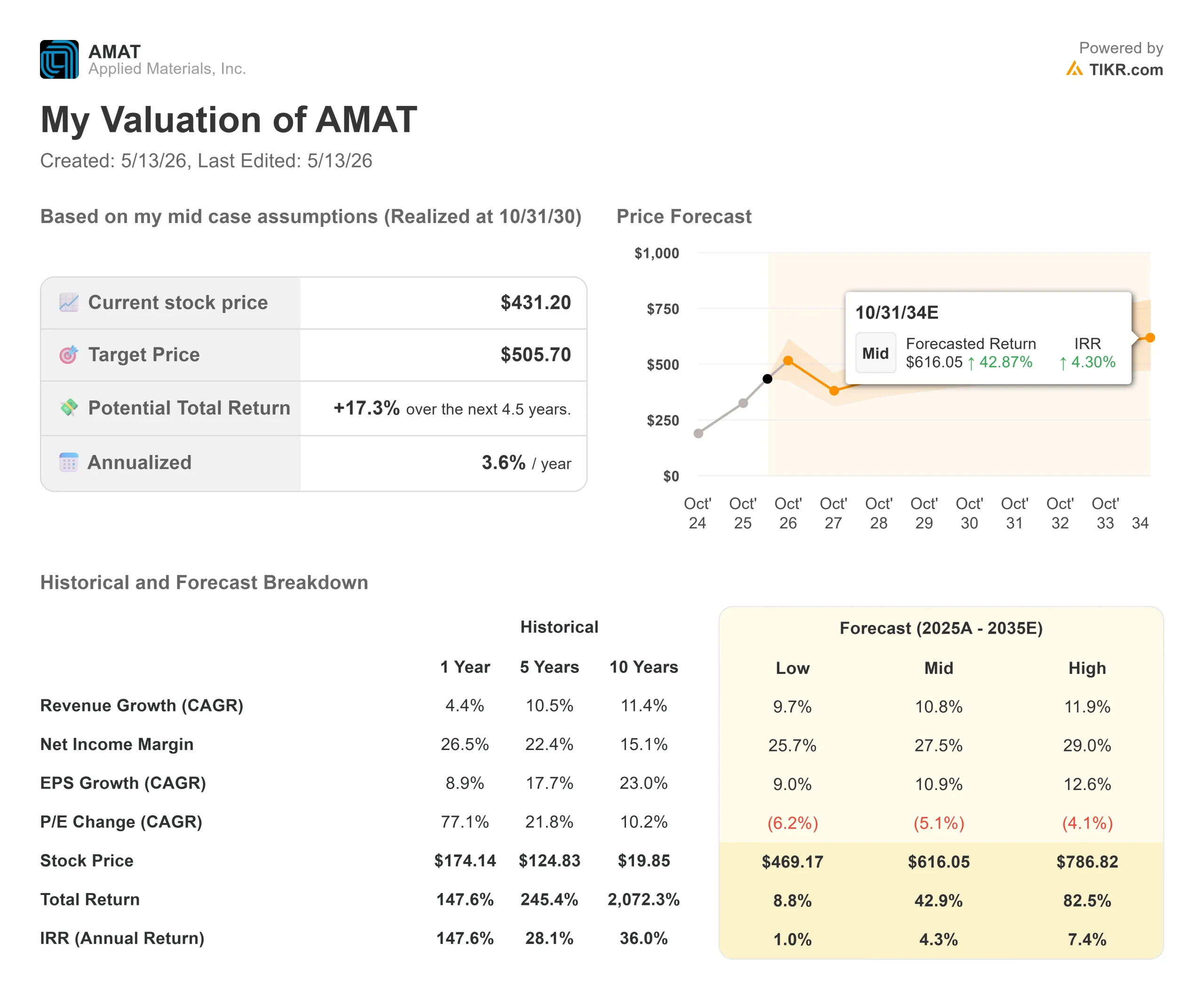

- Current Price: $423.86

- Target Price (Mid): ~$506

- Street Target: ~$444

- Potential Total Return (High Case): ~83%

- Annualized IRR (High Case): ~7% / year

- Most Recent Earnings Reaction: +8.08% (February 12, 2026)

- Max Drawdown: -21.60% (September 3, 2025)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Applied Materials (AMAT) moved 6% in a single session on May 11 on an R&D announcement, not an earnings beat. The catalyst was a new co-innovation partnership with TSMC, which brought the world’s most important chipmaker into Applied’s $5 billion Equipment and Process Innovation and Commercialization (EPIC) Center as a founding partner. That reaction was roughly 20 times the average single-day move that prior AI announcements had generated for Applied, according to StockTitan data. The market was saying something clear. The question is whether the fundamentals back it up.

Fiscal Q2 2026 results land on May 14, the first hard test of whether Applied’s leadership in high-bandwidth memory, advanced packaging, and leading-edge logic is delivering the revenue growth the stock now prices in.

Why the TSMC Partnership Is Different

Applied Materials has assembled a strong EPIC Center roster: Samsung joined first, then Micron and SK Hynix in March 2026, then Advantest in April. TSMC is categorically different. With roughly 70% of the advanced chip foundry market, according to Market Chameleon, TSMC’s roadmap decisions effectively determine what equipment the entire semiconductor industry needs, years before production begins.

As Gary Dickerson, President and CEO of Applied Materials, said at the partnership announcement: “By bringing our teams together at the EPIC Center, we are strengthening that partnership and accelerating the development of technologies to address the unprecedented complexity driving the chipmaking roadmap.”

This matters beyond the headline. Having TSMC co-located inside the same lab compresses the feedback loop between foundry requirements and Applied’s equipment development from quarters to weeks. CFO Brice Hill explained the value of this kind of visibility at the Cantor Global Technology and Industrial Growth Conference in March: Applied now works with two-year customer roadmaps across its top accounts, signaling that demand directly to more than 2,000 suppliers. TSMC, as a resident partner, takes that model to another level.

The EPIC Center, opening in phases this year, is described by Applied as the largest U.S. investment in advanced semiconductor equipment R&D ever made, with capital spending expected to scale to approximately $5 billion.

What Three Simultaneous Upcycles Mean for Revenue

The TSMC news arrives against a specific financial setup. Applied guided fiscal Q2 at approximately $7.65 billion in revenue and approximately $2.64 in adjusted EPS. The company has beaten adjusted EPS estimates in each of its past four quarters by an average of around 5%. Morgan Stanley, which raised its price target to $454 ahead of the print, expects Applied to lift its calendar 2026 semiconductor equipment growth guidance from 20% to 25% or above, noting that peers Lam Research and Tokyo Electron have already set a high bar this earnings season.

The underlying reason is that three markets are accelerating simultaneously. At the Cantor conference, Hill called this historically unusual in 26 years of industry experience: leading-edge logic, DRAM, and advanced packaging all pulling at the same time.

The clearest opportunity is in DRAM. High-bandwidth memory, the stacked chip architecture that feeds AI accelerators, requires roughly three times the wafer area of standard DRAM and adds approximately 19 extra manufacturing steps, 15 of which are equipment steps. Applied captures more than 50% of the value of tools used in those additional steps, per Hill’s conference remarks. As AI clusters scale and HBM generations advance, that wallet share compounds.

On leading-edge logic, data center AI now accounts for 30% of leading-edge wafer consumption, having eclipsed PC demand and pacing to overtake smartphones by 2029, according to Hill. Cloud provider capital expenditures are tracking above $600 billion this year and projected to be above $700 billion in 2027.

Those dynamics translate directly into the forward estimates. TIKR consensus models Applied’s revenue growing from $28.4 billion in fiscal 2025 to around $31.6 billion in fiscal 2026 and around $38.5 billion in fiscal 2027, a roughly 22% acceleration in a single year. Applied Global Services, the recurring business covering spares and service contracts, grew 15% year over year to a record $1.6 billion in fiscal Q1 2026. About two-thirds of that segment operates under multi-year contracts with renewal rates above 90%, per Hill, giving the revenue base unusual stability for a capital equipment company.

See historical and forward estimates for Applied Materials stock (It’s free!) >>>

Margins and Where Valuation Stands

Applied’s Equipment segment reported a gross margin of 54.5% in fiscal Q1 2026, per Hill’s remarks at Cantor. The company’s overall LTM gross margin stands at 48.7%, per TIKR. Two things are driving expansion: higher-complexity tools such as HBM packaging systems and gate-all-around transistor equipment command better pricing, and Applied has built a more disciplined internal pricing process over the past two years, with defined target prices per product. Hill said this has lifted margins and expects it to continue.

TIKR consensus models net income margin expanding from 26.8% in fiscal 2025 to around 28% in fiscal 2026 and roughly 30% by fiscal 2027. Over the past 12 months, Applied returned approximately $4 billion to shareholders, representing around 86% of free cash flow, consistent with its stated 80% to 100% target.

On valuation, Applied trades at roughly 30x NTM EV/EBITDA per TIKR. For context, Lam Research sits at around 33x and KLA Corporation at around 32x on the same metric, while ASML trades at approximately 37x. Given Applied’s broader exposure across deposition, etch, thermal, inspection, and packaging, including more than 50% wallet share in HBM packaging steps, the discount to ASML is defensible. The narrower gap to Lam and KLA becomes the re-rating question if Q2 confirms the guidance raise.

26 analysts rate AMAT a Buy, 5 an Outperform, and 7 a Hold, with no Underperform or Sell ratings, per TIKR’s Street Targets. The mean price target is $444.24. Cantor Fitzgerald raised its target to $550 and maintained Overweight. HSBC initiated coverage on May 8 with a Buy and a $517 target, citing accelerating growth in fiscal 2026 and 2027.

See how Applied Materials performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $423.86

- Target Price (Mid): ~$506

- Potential Total Return (High Case): ~83%

- Annualized IRR (High Case): ~7% / year

See analysts’ growth forecasts and price targets for Applied Materials stock (It’s free!) >>>

The high case is the more relevant frame given where the cycle stands, though it requires the demand environment to hold. It assumes a revenue CAGR of around 12% through fiscal 2030, driven by HBM equipment wallet share and sustained advanced logic demand as gate-all-around architectures deepen Applied’s equipment intensity per wafer. Net income margin expands toward around 29% as HBM Packaging and Applied Global Services grow as a share of revenue. That path yields around 83% total return and roughly 7% annualized through 10/31/30.

The mid case at around $506, roughly 17% total return and around 4% annualized, is not a compelling risk-reward at current prices on its own. The primary risk to both scenarios is a demand air pocket in 2027 if current fab build-outs complete before the next round of capacity decisions, compressing the cycle’s duration. Hill addressed this directly at Cantor: the constraint is not demand but clean room space availability. As long as that bottleneck holds, the cycle extends.

Conclusion

Watch May 14 for two things: whether management raises its full-year semiconductor equipment growth target above 20%, and whether Q3 revenue guidance clears approximately $7.9 billion. A raised full-year outlook alongside a strong Q3 guide confirms that the TSMC partnership timing was strategically driven and that the demand cycle is building, not peaking. A guide that simply tracks the current run rate with no explicit outlook upgrade gives the bears an opening. Management has two years of customer visibility baked into its planning. May 14 shows whether it is showing up in the numbers.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Applied Materials?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Applied Materials, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Applied Materials alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Applied Materials on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!