Key Stats

- Current price: ~$46 (May 12, 2026)

- Q1 2026 revenue: $5.2B (+67% YoY)

- Q1 2026 Adjusted EPS: $0.98 (+180% YoY)

- Q1 2026 attributable EBITDA: $3.9B (+115% YoY)

- Q1 2026 attributable free cash flow: $1.2B (+195% YoY)

- Q2 2026 gold production guidance: 730,000 to 770,000 oz

- Full-year production guidance: unchanged

- TIKR model price target: ~$66

Barrick Mining Stock Posts 67% Revenue Surge as Gold Price Leverage Kicks In

Barrick Mining stock (ABX) posted Q1 2026 revenue of $5.2B, up 67% year over year, as a 66% increase in realized gold prices combined with improved operations to produce one of the strongest quarters in the company’s recent history.

Adjusted EPS came in at $0.98, up 180% from $0.35 in Q1 2025.

Attributable EBITDA reached $3.9B, more than doubling from $1.8B a year ago, at a margin of 75%.

Gold production rose 4% year over year to 719,000 ounces, above guidance, according to Mark Hill, President and CEO, on the Q1 2026 earnings call.

North America was the clearest driver: the region accounted for 57% of attributable EBITDA at a margin of nearly 70%, with Nevada Gold Mines and Pueblo Viejo both posting year-over-year growth.

Loulo-Gounkoto, Barrick’s Mali asset, ramped ahead of schedule after returning from care and maintenance, already contributing meaningfully to quarterly attributable EBITDA at this early stage of the ramp, according to Hill.

Copper produced 49,000 tonnes in Q1, with copper production up 11% year over year.

Attributable free cash flow reached $1.2B, up 195% year over year, according to Helen Cai, Senior EVP and CFO, on the Q1 2026 earnings call.

Barrick ended the quarter with $2.4B in net cash.

The board approved a $3B share buyback authorization, with the existing quarterly base dividend of $0.175 per share maintained and a year-end top-up targeting 50% of attributable free cash flow.

Full-year production and cost guidance remain unchanged, according to Hill; Q2 gold production is guided to 730,000 to 770,000 ounces, above Q1, with further production increases expected in Q3 and Q4.

The Lumwana copper expansion in Zambia advanced slightly ahead of schedule, targeting first copper from the expanded mill by Q1 2028 within a $2B original budget, with throughput set to grow from 27 million tonnes to 52 million tonnes per year and copper output targeted to double from 117,000 to 240,000 tonnes annually.

The North American IPO remains on track for completion by year-end 2026, with filings expected to be public by late summer and market access available in the fall, according to an unnamed executive on the Q1 2026 earnings call.

Reko Diq is under a 12-month review following force majeure notices from contractors and security concerns, with holding costs running approximately $20M per month during the review period, according to Hill.

Barrick Mining Stock: What the Income Statement Shows

The income statement tells a margin expansion story of unusual speed and scale.

Gross margin in Q1 2026 reached 60%, up from 43% in Q1 2025 and 49% in Q2 2025, as elevated gold prices flowed directly through a relatively stable cost base.

Gross profit in Q1 2026 was $3.2B, up from $1.4B a year earlier.

Operating margin reached 56% in Q1 2026, the highest in the eight quarters shown on the income statement, up from 38% in Q1 2025 and 44% in Q3 2025.

Operating income was $2.9B in Q1 2026, compared to $1.2B in Q1 2025, a 147% year-over-year increase.

The Q4 2025 quarter showed even higher absolute revenue at $6.0B, but Q1 2026 operating margin of 56% surpassed Q4’s 53%, reflecting tighter cost discipline alongside strong gold pricing.

Cai attributed the results not solely to the gold price environment: she described the quarter as one of strong earnings quality, with operating performance, cost discipline, portfolio optimization, and capital efficiency all contributing, according to remarks on the Q1 2026 earnings call.

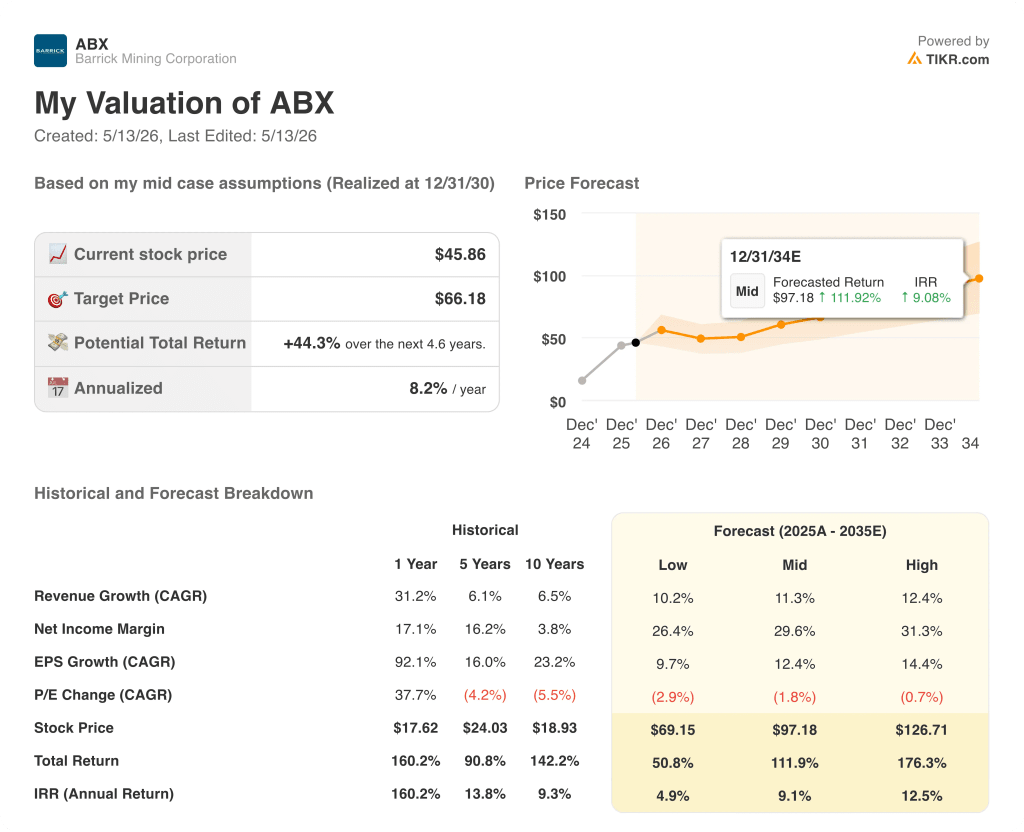

What Does the Valuation Model Say?

The TIKR model prices Barrick Mining stock at a mid-case target of ~$66, implying roughly 44% total upside from the current price of ~$46 over approximately 4.6 years, or 8.2% annualized.

The mid-case assumes an 11% revenue CAGR and a net income margin of ~30% through 2035, against a historical one-year net income margin of 17%.

The Q1 result provides direct support for that margin assumption: 75% EBITDA margin and 56% operating margin in a single quarter demonstrate that the portfolio can sustain significantly higher profitability than the historical average when gold prices cooperate.

The risk to the model is that the mid-case margin of ~30% is predicated on a gold price environment remaining broadly supportive through a multi-year forecast window; a reversion toward historical average pricing would pressure that assumption.

The model also embeds a P/E compression assumption of (1.8%) CAGR at mid-case, meaning the price target of ~$66 is reached despite a modest multiple contraction, not because of multiple expansion.

Barrick Mining stock enters the post-earnings period with a Q1 that validates the margin and cash flow trajectory the model requires, strengthening the investment case at current prices.

The Q1 result was strong, but Barrick Mining stock’s path to the TIKR model target depends on sustained execution across a complex multi-jurisdiction portfolio at a time when two major growth initiatives and a first-ever North American IPO are running simultaneously.

What Has to Go Right

- Gold prices must remain broadly supportive: the 67% revenue growth in Q1 2026 was driven in part by a 66% realized gold price increase, according to Cai on the Q1 2026 earnings call, and the mid-case model margin of ~30% requires an environment where that pricing leverage persists

- Loulo-Gounkoto’s ramp must reach full steady-state production of 600,000-plus ounces, having already started ahead of schedule in Q1

- Lumwana’s $2B copper expansion must deliver first copper by Q1 2028 on schedule and within budget, more than doubling copper output from 117,000 to 240,000 tonnes

- The North American IPO must close by year-end 2026 without disrupting NGM or Pueblo Viejo operations, unlocking what Hill described as significant shareholder value

What Could Still Go Wrong

- Reko Diq represents a live capital and execution risk: force majeure notices from contractors, unresolved security concerns in Pakistan, and a ~$20M monthly holding cost during the 12-month review create an open-ended drag on capital allocation

- North American IPO complexity is non-trivial: regulatory filings with the SEC and TSX, Fourmile inclusion negotiations with Newmont still unresolved, and a year-end deadline leave little room for delay

- Barrick’s Q1 gold production of 719,000 ounces was partially boosted by NGM inventory that was not drawn down in Q4 2025, according to Hill, meaning the Q1 baseline carries some pull-forward that will not repeat in Q2

- Mali country risk remains active: although Loulo-Gounkoto operations were unaffected in Q1, management flagged active contractor transition work in open-pit mining through year-end, and five months of key supply inventory was cited as the primary buffer

Should You Invest in Barrick Mining Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Barrick Mining stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Barrick Mining stock alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ABX stock on TIKR for Free →