Key Stats for Boston Scientific Stock

- 52-Week Range: $53 to $110

- Current Price: $53

- Street Mean Target: $53

- Street High Target: $110

- Analyst Consensus: 31 Buys/Outperforms, 2 Holds, 0 Sells

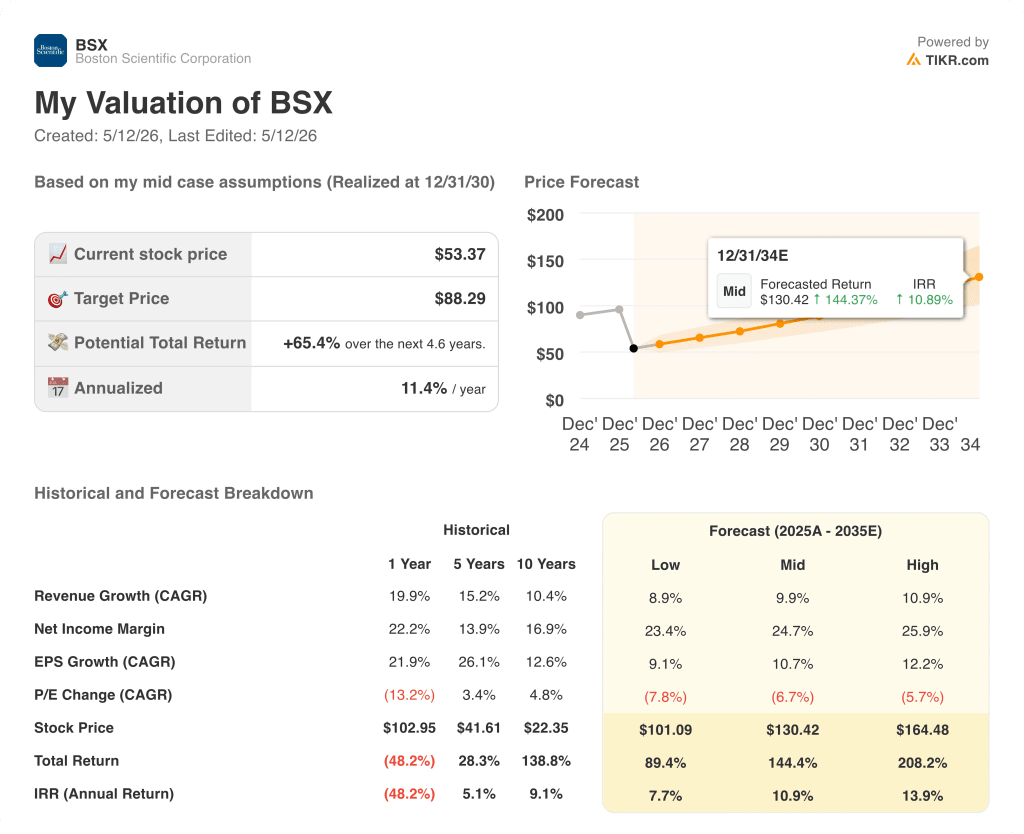

- TIKR Model Target (Dec. 2030): $88

What Happened?

Boston Scientific Corporation (BSX) designs and sells medical devices across interventional cardiology, electrophysiology, neuromodulation, endoscopy, and urology, and Boston Scientific stock has fallen roughly 47% from its 52-week high as a sequence of headwinds forced management to reset expectations.

The reset arrived formally on April 22, when the company reported first-quarter revenue of $5.20 billion, up 11.6% year over year, and adjusted EPS of $0.80, both landing slightly above Street estimates.

The headline beat was immediately overshadowed by a guidance cut that shook investor confidence.

Boston Scientific now expects full-year 2026 organic revenue growth of 6.5% to 8%, down sharply from the prior range of 10% to 11%, with adjusted EPS of $3.34 to $3.41 representing 9% to 11% growth.

CEO Mike Mahoney identified three sources of the downward revision: competitive erosion in the electrophysiology business, a deceleration in stand-alone WATCHMAN left atrial appendage closure procedures, and underperformance in the urology segment.

On EP, the company now guides to approximately 10% global growth for 2026, with U.S. growth in the mid-single-digit range, as Medtronic, Johnson and Johnson, and Abbott have accelerated their pulsed-field ablation entries into the U.S. market.

The WATCHMAN story is more nuanced: global mid-teens growth is still expected for 2026, but the strong stand-alone procedure volumes of recent years are giving way to concomitant procedures, performed alongside an ablation in the same session, which carry a different revenue cadence and require hospital workflow adjustments that are taking longer to resolve than management initially expected.

J.P. Morgan analyst Robbie Marcus called the revision “the reset investors wanted” and said that should management now deliver upside to this guide, “BSX shares could potentially be the best performing stock from here over the coming 12 months.”

The guidance cut was not the only development shaping the investment case. On March 28, Boston Scientific presented the CHAMPION-AF trial at the American College of Cardiology meeting, showing that WATCHMAN FLX outperformed blood thinners on bleeding outcomes while matching drug therapy on stroke prevention across a 3,000-patient randomized study.

The company believes CHAMPION supports a label expansion that could quadruple the eligible patient population from roughly 5 million today to 20 million by 2030, though label changes, guideline updates, and a revised CMS national coverage decision will each take time.

HI-PEITHO trial data, also presented at ACC, showed that the EKOS endovascular system cut the composite endpoint event rate in intermediate-risk pulmonary embolism to 4.0% versus 10.3% with anticoagulation alone, with zero intracranial bleeding events across 544 patients.

Additionally, last January , Boston Scientific announced its agreement to acquire Penumbra for approximately $14.5 billion, a re-entry into neurovascular and thrombectomy, two segments where BSX currently generates no revenue.

The Penumbra shareholder vote passed on May 6, and the deal is expected to close in the second half of 2026, funded by roughly $11 billion in cash and newly issued debt.

On May 8, the FDA classified a software recall affecting six pacemaker models, including Accolade and Essentio devices, as its most serious category, requiring a software update during an in-person clinic visit rather than device removal.

Wall Street’s Take on BSX Stock

The guidance reset has done something unusual: it compressed Boston Scientific stock to near its 52-week floor at the same moment the clinical pipeline is arguably the richest in the company’s history, creating a setup where the price reflects today’s headwinds while ignoring 2027’s tailwinds.

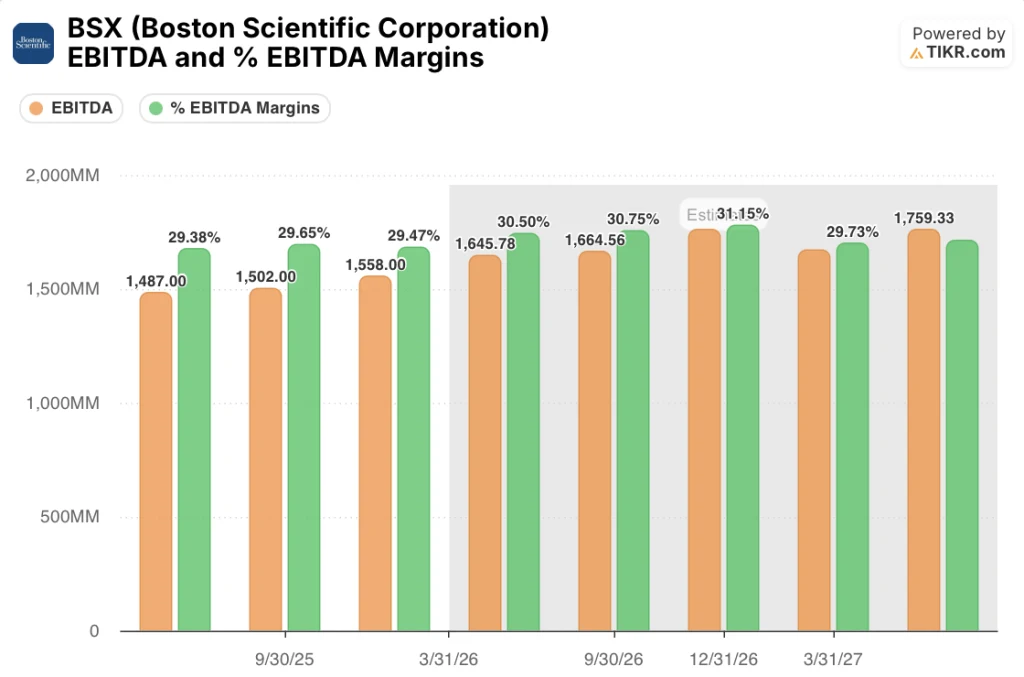

BSX’s EBITDA is expected to reach approximately $1.65 billion in the second quarter of 2026 and grow to approximately $1.76 billion by year-end, with consensus margins expanding from 29.5% in the fourth quarter of 2025 to 31% by the end of 2026, as the Penumbra transaction closes and EP comparables normalize.

Thirty-one of 33 analysts rate BSX a buy or outperform, with 2 holds and zero sells, a level of conviction that has held even through the guidance cut and Boston Scientific stock’s descent to multi-year lows.

The spread between the Street high target of $110 and the Street low of $60 captures the genuine debate: the high-end bulls are pricing in a clean 2027 recovery while the lower-conviction targets reflect a scenario where all three headwinds linger simultaneously.

CFO Jonathan Monson stated the company has “much more restrictive spend controls across the business” alongside AI automation initiatives and a concentrated R&D review, steps designed to protect margin even as revenue growth moderates.

If stand-alone WATCHMAN procedure volume does not stabilize in the second half as management projects, the 50 to 75 basis point adjusted operating margin expansion target becomes difficult to defend.

The Q3 2026 earnings call is the first real checkpoint: investors should watch whether concomitant growth offsets stand-alone WATCHMAN declines at a ratio that keeps total WATCHMAN growth within the low-to-mid-teens range guided for the year.

What Does the Valuation Model Say?

TIKR’s mid-case model assigns a target price of $88 to BSX stock, implying a 65% total return over the next ~5 years at an annualized rate of around 11%, underpinned by a revenue CAGR forecast of around 10% and net income margins expanding from 23% today toward approximately 25%.

The central tension is whether three simultaneous headwinds, EP share erosion, WATCHMAN stand-alone deceleration, and urology underperformance, reset fast enough for FARAWAVE Ultra, Penumbra, and the CHAMPION label expansion to compound together in 2027 and 2028.

Bull Case

- Q1 adjusted EPS of $0.80 beat the $0.79 estimate at the high end of guidance despite three active headwinds, demonstrating operating leverage even in a down-guide quarter

- Cardiovascular delivered $3.5 billion in Q1 revenue, up 13.5% year over year, led by FARAPULSE, WATCHMAN, and AGENT DCB, confirming the core growth engine is intact despite segment-level noise

- CHAMPION-AF hit all primary safety and efficacy endpoints across 3,000 patients, and management has committed to a label expansion submission that could expand the eligible WATCHMAN population from 5 million to 20 million

- FARAWAVE Ultra launches in the first half of 2027 alongside a differentiated ICE platform and FARAFLEX, three product cycles that arrive on materially easier comparables

- The company guided to approximately $4 billion in free cash flow for 2026, providing the capital to absorb Penumbra’s debt load and fund the $2 billion share repurchase authorized for Q2

Bear Case

- U.S. EP growth is guided to the mid-single-digit range for all of 2026, meaning the segment that drove Boston Scientific stock from the low $40s to $110 over two years is running at flat to low single digits domestically for three consecutive quarters

- Stand-alone WATCHMAN procedures are decelerating due to reimbursement pressure on interventional cardiologists and hospital capacity constraints that management does not expect to fully resolve until 2027

- The $14.5 billion Penumbra acquisition adds approximately $11 billion in new debt, raising the gross leverage ratio well above the current 1.8x and constraining capital allocation at a moment when the core business needs commercial reinvestment

- A securities class action filed in March alleging misleading statements about 2025 U.S. EP growth sustainability remains unresolved and creates ongoing headline risk

- The May 8 FDA Class I pacemaker software recall, linked to four reported deaths and 2,557 serious injuries as of March 18, adds regulatory and reputational exposure on top of an already complex operational backdrop

Should You Invest in Boston Scientific Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Boston Scientific Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Boston Scientific Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze BSX stock on TIKR for Free →