Key Stats

- Current price: $29 (May 11, 2026)

- Q1 2026 revenue: $608M (+4% YoY)

- Q1 2026 adjusted EBITDA: $44M (7% margin)

- Q1 2026 subscribers: ~2.6M (+9% YoY)

- Q2 2026 revenue guidance: $680M–$700M (+25%–28% YoY)

- FY2026 revenue guidance (raised): $2.8B–$3.0B (+19%–28% YoY)

- FY2026 adjusted EBITDA guidance: $275M–$350M (~11% margin at midpoint)

- TIKR model price target: $55

- Implied upside: +89%

Hims & Hers Stock Posts Muted Q1 as GLP-1 Pivot Hits Revenue, But Demand Signals Point Higher

Hims & Hers stock (HIMS) delivered Q1 2026 revenue of $608M, up just 4% year over year, as a deliberate strategic pivot away from compounded GLP-1 products created short-term financial friction.

The company discontinued advertising compounded weight loss products in March and shifted toward branded GLP-1 offerings, including Wegovy from Novo Nordisk, which disrupted revenue recognition patterns and created a tougher comparable against Q1 2025’s record weight loss subscriber additions.

Within six weeks of introducing Wegovy to its platform, Hims & Hers fulfilled more than 125,000 Wegovy shipments and is on track to add more than 100,000 new weight loss subscribers per month, according to CFO Yemi Okupe on the Q1 earnings call.

Adjusted EBITDA came in at $44M, representing a 7% margin, weighed down by approximately $33M in restructuring charges tied to the pivot, with $28M of that amount reducing GAAP gross margin by roughly 5 percentage points.

GAAP gross margin was 65% in Q1; adjusted for the one-time charges, it was 70%.

GAAP net income swung to a loss of $92M in Q1, reflecting the restructuring costs, M&A transaction expenses, and legal costs; management guided for a return to net income profitability in 2027.

International revenue reached $78M, up nearly tenfold year over year, driven by the ZAVA and Livewell acquisitions.

Marketing efficiency improved, with marketing as a percentage of revenue declining 3 percentage points year over year and sequentially to 36% in Q1.

The company completed the acquisition of YourBio in Q1, a provider of at-home blood collection technology, and expects its planned acquisition of Eucalyptus to close in H2 2026 for approximately $240M at closing, extending its footprint across Australia, the U.K., Germany, Japan, and Canada.

FY2026 revenue guidance was raised to $2.8B–$3.0B, representing 19%–28% growth year over year, with adjusted EBITDA guided to $275M–$350M at approximately an 11% midpoint margin.

For Q2 2026, management guided revenue of $680M–$700M, reflecting 25%–28% growth year over year, and adjusted EBITDA of $35M–$55M.

CEO Andrew Dudum reiterated long-term 2030 targets of at least $6.5B in revenue and $1.3B in adjusted EBITDA, stating confidence has only increased.

Hims & Hers Stock Financials: Margins Under Pressure as Pivot Resets the Base

The income statement through Q4 2025 shows Hims & Hers stock in a pattern of expanding revenue alongside volatile and gradually compressing margins as the company absorbs the cost of rapid category expansion.

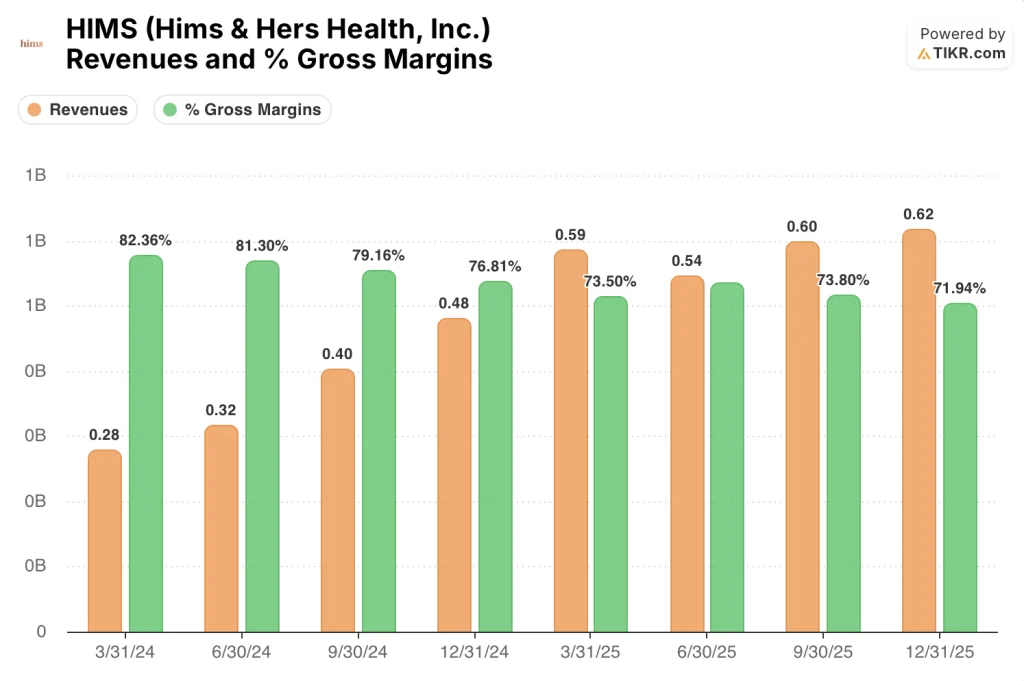

Quarterly revenue climbed from $280M in Q1 2024 to $620M in Q4 2025, a more than doubling of the top line in eight quarters.

Gross margin peaked at 82% in Q1 2024 and has since compressed to 72% by Q4 2025, as lower-margin specialties including weight loss, labs, and international markets scaled as a larger share of the mix.

Operating income peaked at $60M in Q1 2025 at a 10% margin, then pulled back to $30M in Q2, $10M in Q3, and $20M in Q4 as operating expense growth outpaced revenue.

Okupe confirmed on the Q1 2026 call that gross margins are expected to compress by a further couple of points in coming quarters as weight loss, labs, and international remain the primary growth vectors, all carrying lower margin profiles than the company’s longer-tenured specialties.

The company generated $89M in operating cash flow and $53M in free cash flow in Q1 2026, according to Okupe, despite the GAAP loss, underscoring that the restructuring hit was non-cash-intensive.

What Does the Valuation Model Say?

TIKR’s model sets a price target of $55 for Hims & Hers stock, implying 89% upside from the May 11 close of $29, or roughly 15% annualized over ~5 years.

The mid-case assumptions require a revenue CAGR of 12% from 2025 through 2035 and a net income margin of near 9%, a meaningful step up from the negative net margins the company posted over the past three and five years.

The Q1 print does not invalidate those assumptions, but it pushes the timeline: the near-term margin compression guidance and the 2027 net income profitability target mean the model’s margin assumptions are back-weighted.

The 89% implied upside is real, but it is contingent on execution through what management described as a transition period with GAAP volatility, not a near-term re-rating catalyst.

The Q1 pivot created short-term financial noise, but Wegovy adoption signals and a raised full-year revenue guide force the question: does the margin compression matter if subscriber growth accelerates at scale?

Near-Term Pressures

- Q1 revenue grew just 4% year over year to $608M, the slowest quarterly growth rate visible across the income statement period, with GAAP gross margin falling to 65% after $28M in restructuring charges

- Q2 2026 adjusted EBITDA is guided at just $35M–$55M at midpoint, implying a second consecutive quarter of below-10% margins before the back-half ramp

- Gross margin is expected to compress by a further couple of points in coming quarters as weight loss, labs, and international scale at lower margins than legacy specialties, per Okupe

- The Eucalyptus acquisition, expected to close in H2 2026 for approximately $240M at closing, will add integration complexity and cash deployment at a moment when domestic margins are already under pressure

Long-Term Platform Thesis

- Within six weeks of introducing Wegovy, the platform fulfilled more than 125,000 shipments and is on track to add more than 100,000 new weight loss subscribers per month, a pace management says exceeds demand seen during peak New Year and Super Bowl campaigns

- FY2026 revenue guidance was raised to $2.8B–$3.0B, implying 19%–28% growth, with a significant step-up in adjusted EBITDA dollars expected in Q3 and Q4 as monthly subscriber cohorts compound

- The 2030 targets of at least $6.5B in revenue and $1.3B in adjusted EBITDA imply a platform that has expanded internationally, verticalized new specialties including peptides, and leveraged AI infrastructure to reduce cost-to-serve

- Free cash flow of $53M in Q1 despite the GAAP loss and $751M in cash and short-term investments provide financial runway to absorb the transition period without balance sheet stress

Should You Invest in Hims & Hers Health, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Hims & Hers Health, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Hims & Hers Health, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze HIMS stock on TIKR for Free →