Key Stats for Applied Digital Stock

- Current Price: $41.25

- Street Consensus Target: ~$53

- TIKR Model Target Price (Low Case): ~$146

- Potential Total Return (Low Case): ~253%

- Annualized IRR (Low Case): ~17% / year

- Earnings Reaction: –7.99% (April 8, 2026)

- Max Drawdown: –50.31% (March 30, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

AI infrastructure stocks spent much of 2026 being asked one question: Where are the new leases? For Applied Digital (APLD), the answer came on April 23, and it was larger than most investors expected.

The company announced a 15-year lease with a new U.S.-based, investment-grade hyperscaler at its Delta Forge 1 campus, a 430-megawatt (MW) AI factory under construction in the southern United States. The deal covers 300 MW of critical IT load and carries approximately $7.5 billion in total contracted value. Shares jumped more than 14% on the news.

Then on May 5, Applied Digital completed the separation of its cloud business, contributing it to EKSO Bionics Holdings, which renamed itself ChronoScale Corporation (CHRN). Applied Digital retained approximately 97% of ChronoScale’s shares and invested $15.75 million at closing. The stock surged another ~12% that day.

Together, the two events answered the questions most weighing on the stock: can management sign new hyperscaler leases, and will the cloud drag end? Both answered within two weeks. APLD is up ~45% in the past month, against a max drawdown of 50.31% as recently as March 30.

Bears still point to $2.7 billion in debt, ongoing GAAP losses, and a construction timeline that stretches into 2027. The unresolved question is whether the remaining pipeline, roughly one gigawatt across four campuses, gets contracted on the schedule management is signaling.

What the Q3 Earnings Call Actually Revealed

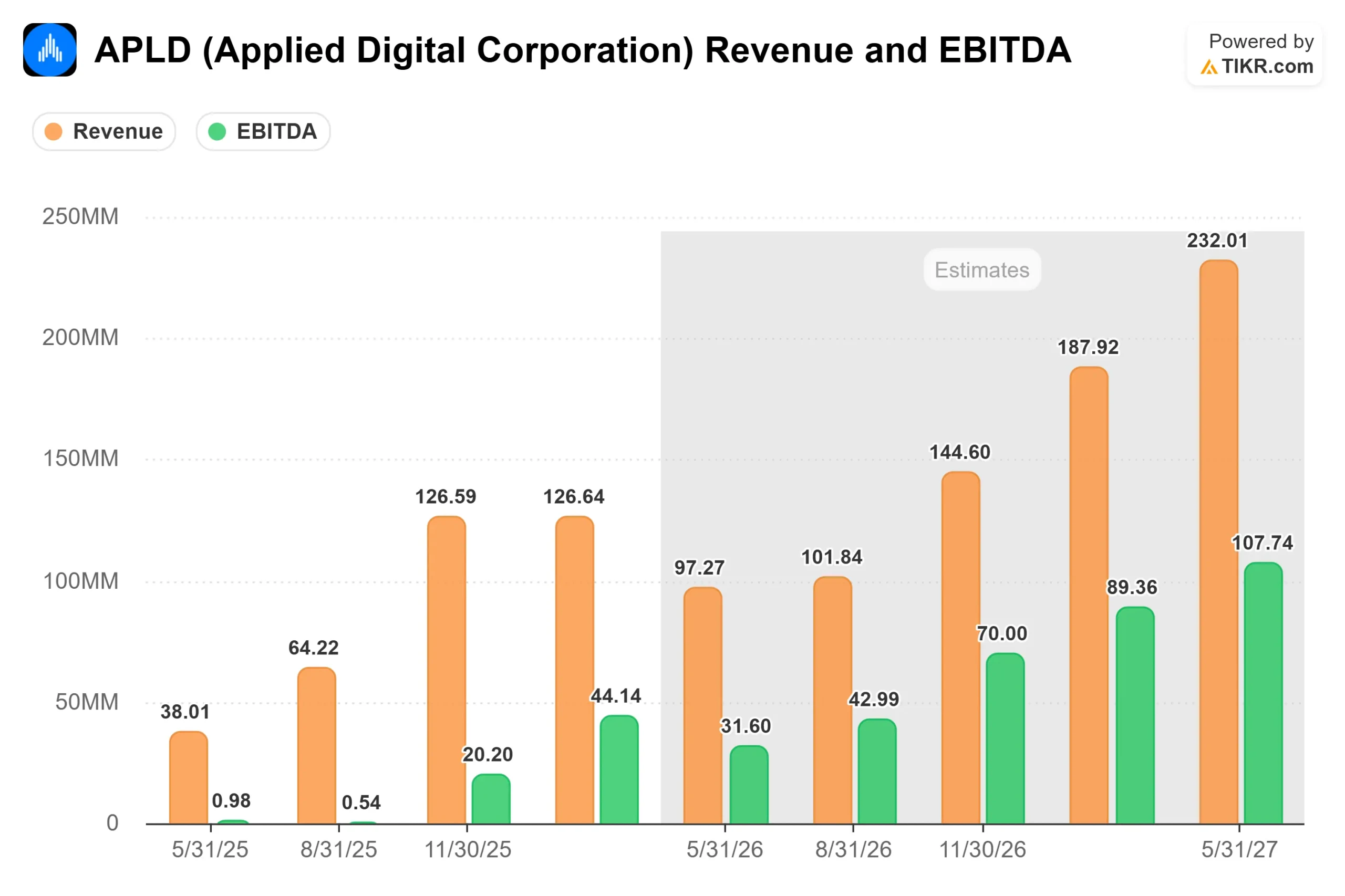

Fiscal Q3 2026, the quarter ended February 28, was strong on an adjusted basis and noisy on a GAAP one. Revenue came in at $126.6 million, up 139% year-over-year, beating the ~$78.5 million analyst estimate by over 61%. Adjusted EBITDA of $44.1 million crushed the $16.19 million consensus. Adjusted EPS of $0.09 beat the –$0.21 estimate by nearly 143%.

The GAAP net loss of $100.9 million was driven by two non-cash items: a $59.7 million write-down of the cloud business following its reclassification from held-for-sale, and $39.3 million in stock-based compensation. Neither reflects the core HPC hosting trajectory. The stock still fell 7.99% on earnings day before recovering as the adjusted picture became clear.

The financing story from that call matters more than the headline numbers. CFO Saidal Mohmand confirmed Applied Digital ended the quarter with $2.1 billion in cash against $2.7 billion in debt, with no significant maturities due in the next two years. He outlined the Macquarie Asset Management structure: up to $4.1 billion in preferred equity available following a signed lease with an investment-grade hyperscaler, a condition Delta Forge 1 now satisfies. Under this model, Applied Digital shareholders retain over 85% common equity ownership of future sites while reducing reliance on public equity markets.

The CoreWeave lease restructuring, announced March 30, also matters for the cost of capital. Applied Digital executed amendments, including a $50 million letter of credit and an unconditional springing parent guarantee from CoreWeave. The CoreWeave SPV received an A3 investment-grade credit rating, up from its previous BB rating. As Mohmand explained, investment-grade debt prices have a mid-200 basis points of spread; BB debt runs 350 to 450 basis points. On a multi-billion-dollar debt stack, that difference is the mechanism through which long-term shareholder returns get unlocked.

CEO Wes Cummins framed the demand environment plainly: “Just 3 months ago, we referenced approximately $400 billion in annual capital expenditures from the largest U.S. hyperscalers. That figure has now been reported to have increased to nearly $700 billion.” For a company with grid-connected sites and proven direct-to-chip liquid-cooling execution, that backdrop is the fundamental tailwind.

See historical and forward estimates for Applied Digital stock (It’s free!) >>>

The Pipeline: A Gigawatt Still to Convert

The Delta Forge 1 lease covers 300 of the campus’s 430 MW, leaving 130 MW available for expansion. Management is actively marketing three additional sites beyond Delta Forge 1 one more in North Dakota, and two in undisclosed states representing approximately one gigawatt of combined grid power capacity, with some in what Cummins called “advanced stages of negotiation.”

The South Dakota site was paused after the state legislature declined the tax exemptions sought. Two new sites replaced it in the active pipeline. On lease discipline, Cummins was clear: “we don’t put these deadlines on ourselves. We just make sure that we end up with the right customer and the right contract.”

On the power side, Applied Digital is providing limited credit support to Base Electron, an independent power producer working with Babcock & Wilcox to build approximately 1.2 gigawatts of natural gas-fired generation capacity in the Dakotas. In exchange, Applied Digital shareholders will own approximately 10% of Base Electron upside exposure with no direct construction risk on the generation assets.

Applied Digital now carries over $23 billion in total contracted revenue backed by three hyperscalers, with over half tied to investment-grade counterparties. Management has set internal leadership targets at both the $1 billion and $2 billion NOI (net operating income) levels, reinforcing the five-year goal.

How APLD Stacks Up Against Peers

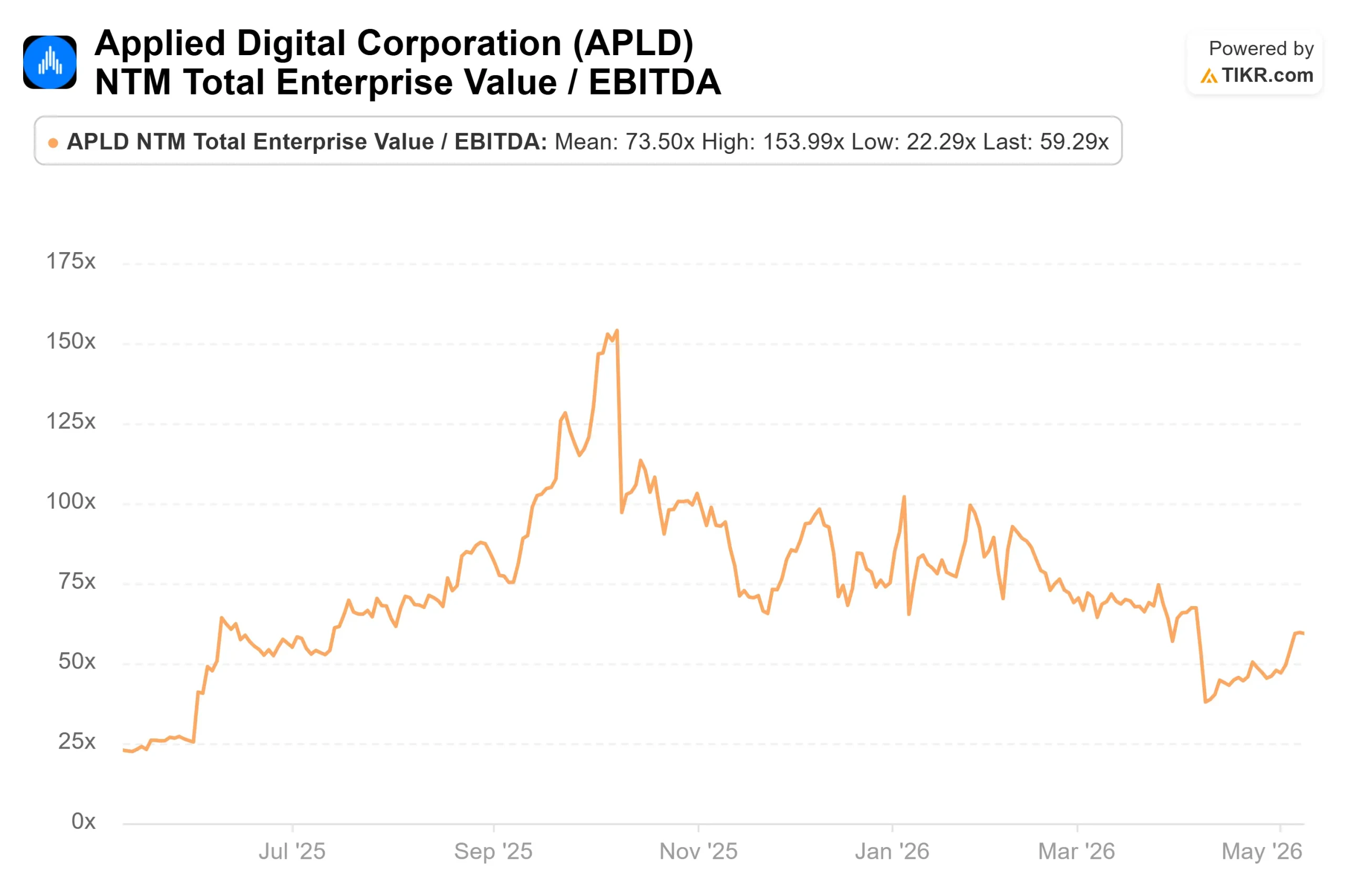

Applied Digital trades at 26.09x NTM EV/Revenue and 59.29x NTM EV/EBITDA. CoreWeave (CRWV), its largest tenant, trades at 10.35x NTM EV/Revenue and 10.35x NTM EV/EBITDA. DigitalOcean (DOCN), a cloud infrastructure peer, trades at 14.40x NTM EV/Revenue and 37.42x NTM EV/EBITDA.

APLD screens are expensive on those numbers. But CoreWeave and DigitalOcean are largely operational businesses; their multiples anchor to today’s revenue. Applied Digital’s NTM EBITDA consensus sits at approximately $234 million, a figure set to ramp sharply as new buildings come online through fiscal 2027 and 2028. The premium is a bet on execution velocity, not a mispricing of mature cash flows.

See how Applied Digital performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

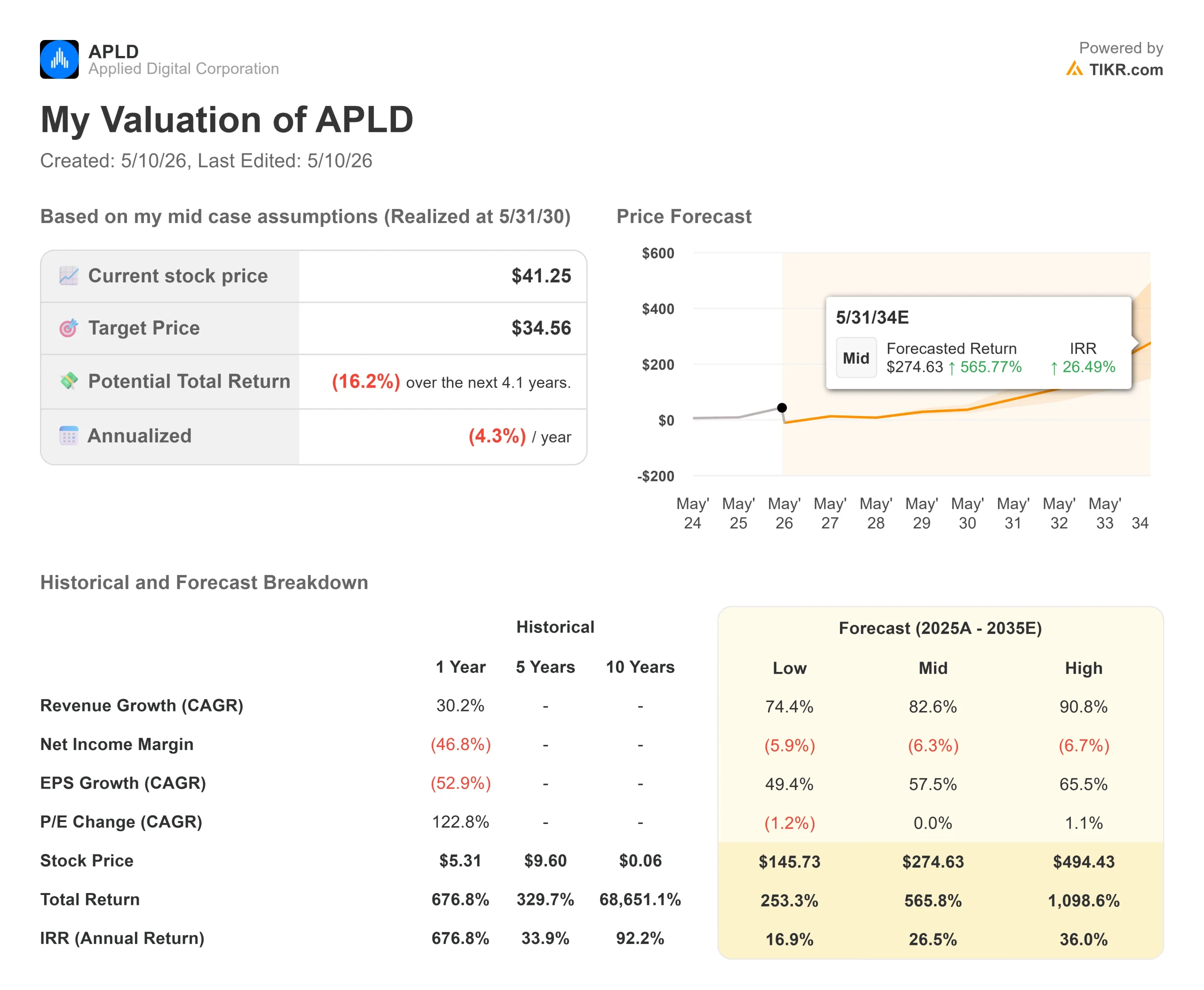

- Current Price: $41.25

- TIKR Model Target Price (Low Case): ~$146

- Potential Total Return (Low Case): ~253%

- Annualized IRR (Low Case): ~17% / year

See analysts’ growth forecasts and price targets for Applied Digital stock (It’s free!) >>>

One important context note: the TIKR model’s mid-case target of $34.56 realized at 5/31/30 sits below the current stock price of $41.25. That means the market is already pricing in above-mid-case execution on a four-year horizon. The longer-range mid-case, realized at 5/31/34, reaches ~$275, representing ~566% total return and a ~26% annualized IRR, but that is an eight-year horizon. This article uses the lowercase as the conservative anchor.

The low case assumes roughly 74% revenue CAGR, a net income margin of around (5.9%), and flat multiple change arriving at approximately $146 by May 2034 and a ~17% annualized IRR. The mid case (around 83% revenue CAGR) reaches ~$275. The high case (around 91% revenue growth) reaches ~$494.

Two drivers underpin even the low case: the sequential activation of new 150 MW buildings at Polaris Forge 1 and Polaris Forge 2 through late fiscal 2026, and the Delta Forge 1 ramp beginning mid-2027. The margin driver is operating leverage as the construction-phase overhead gets distributed across a growing revenue base. The primary risk is that delay slippage on construction or leasing pushes the ramp rightward and shrinks returns. Free cash flow remains deeply negative as capital expenditures peak, so this is a long-duration investment case.

Conclusion

Watch the Q4 fiscal 2026 report, expected around July 29, 2026. The key metric is whether the first 150 MW building at Polaris Forge 1 begins energizing its data halls on the July schedule, as Cummins confirmed. Revenue recognition from that building flows through August and September, and a near-full quarter contribution is expected in the November report. That ramp is the first real proof of the earnings power on which the entire thesis rests.

Applied Digital has crossed from a construction story to one backed by $23 billion in contracted revenue. Whether $41.25 is cheap or fully priced comes down to whether the pipeline campuses close and whether the buildings already under construction deliver on time.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Applied Digital?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Applied Digital, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Applied Digital alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Applied Digital on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!