Key Stats

- Current Price: $102 (May 8, 2026)

- Q1 2026 Revenue: $1.86B, up 9.2% YoY

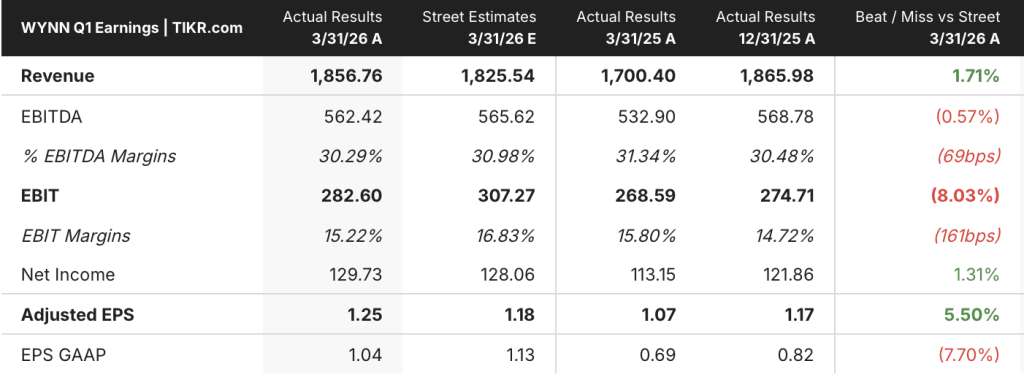

- Q1 2026 Adjusted EPS: $1.25, up from $1.07 in Q1 2025

- Las Vegas EBITDAR: $232.5M, margin 35.1%

- Macau EBITDAR: $279.4M, margin 28.2%

- Boston EBITDAR: $50.5M, margin 24.6%

- LTM Adjusted EBITDAR: ~$2.3B

- TIKR Model Price Target: ~$151 (mid case)

- Implied Upside: ~48%

Wynn Resorts Q1 2026 Earnings Breakdown

Wynn Resorts stock (WYNN) posted Q1 2026 revenue of $1.86B, up 9.2% year over year, with adjusted EPS of $1.25 against $1.07 in the prior-year period.

Macau was the volume engine of the quarter, with Wynn’s combined Macau operations generating $989.2M in operating revenue and $279.4M in adjusted property EBITDAR at a 28.2% margin, according to CFO Craig Fullalove on the Q1 2026 earnings call.

Mass drop in Macau surged 19% and handle rose 32% year over year, with CEO Craig Billings noting on the Q1 earnings call that Wynn Palace regularly operates near 100% occupancy.

Lower-than-expected VIP hold reduced Macau EBITDAR by $17M in the quarter, per Fullalove; on a hold-adjusted basis, EBITDAR would have been approximately $296M.

Las Vegas delivered $232.5M in adjusted property EBITDAR on $661.9M of operating revenue, with a 35.1% EBITDAR margin and hold impact of just over $2M to the negative, according to Fullalove.

Casino revenues in Las Vegas were up over 9%, hotel RevPAR rose nearly 10% on a 12% increase in rate, and Billings noted on the Q1 call that momentum has carried into Q2 with drop, handle, and ADR all tracking ahead of the prior year.

Encore Boston Harbor contributed $50.5M in EBITDAR on revenue of $205.7M, representing a 24.6% margin, with OpEx per day of $1.22M rising 3.9% year over year amid continued labor pressures, per Fullalove.

The most consequential forward announcement was the Enclave at Wynn Palace, a $900M to $950M addition of 432 all-suite rooms that will increase existing room count by 25% and suite count by 50%, with Billings noting on the Q1 call that at 99% occupancy the underwrite is straightforward and that projected GGR of approximately $400M could translate to $150M to $175M in incremental EBITDA.

On the UAE, Billings said construction at Wynn Al Marjan continues with over 22,000 workers on site but that a modest delay to the opening timeline is expected due to regional logistical challenges; the project remains on course to open in 2027, and total equity contributed to date stands at $1.01B with a drawn construction loan balance of $962.3M.

The Wynn Resorts board declared a cash dividend of $0.25 per share payable May 29, 2026, the company repurchased 528,000 shares for approximately $53.8M during Q1, and an additional $30.6M in buybacks occurred in the first weeks of Q2.

Global liquidity stands at $4.4B, comprising $2.8B in Macau and $1.6B in the U.S., with consolidated net leverage at just over 4.4x LTM adjusted EBITDAR, per Fullalove.

Wynn Resorts Stock: What the Income Statement Shows

The income statement tells a story of revenue growth with margin holding firm: Wynn Resorts stock has delivered a sequential revenue recovery since the Q1 2025 trough, with modest operating leverage that kept the bottom line constructive through a period of rising costs.

Total revenue troughed at $1.70B in Q1 2025 and has since climbed through $1.74B, $1.83B, and $1.87B in the three subsequent quarters before landing at $1.86B in Q1 2026.

Gross margin held at 68% in Q1 2026, in line with Q1 2025’s 68% and consistent with the property’s normalized range, excluding the Q3 2024 anomaly when a high cost-of-goods quarter compressed margins to 42%.

Operating margin reached 15% in Q1 2026, up from 16% in Q1 2025 on a rounded basis; the more meaningful comparison is the directional trend, where operating margin has ranged between 16% and 21% over the trailing six quarters while revenue recovered.

Operating income came in at $280M in Q1 2026, essentially flat versus $280M in Q1 2025 and recovering from a $130M trough in Q3 2024, reflecting the stabilization of costs following the reopening investment cycle.

What Does the Valuation Model Say?

TIKR’s mid-case model prices Wynn Resorts stock at approximately $151, implying roughly 48% upside from the May 8 close of $102.

The model assumes a revenue CAGR of 3.6% through 2035 and a net income margin of 7.9%, reflecting a business generating steady cash flow across its three operating markets with the UAE contribution entering the picture from 2027 onward.

The Q1 report strengthens the investment case incrementally: the 9.2% revenue growth, Macau mass momentum, and Las Vegas EBITDAR margin above 35% are consistent with or ahead of the trajectory the model requires.

The Enclave announcement introduces an incremental return vector, but the $900M to $950M capex commitment and 2027-plus construction timeline mean it is a long-dated input, not a near-term catalyst.

At current prices, Wynn Resorts stock offers material upside if the mid-case revenue assumptions hold, but the 4.4x net leverage ratio and Al Marjan execution risk are the primary constraints on multiple expansion.

Wynn’s investment thesis now hinges on two large-scale projects delivering on schedule: the UAE opening in 2027 and the Enclave at Wynn Palace proceeding without meaningful disruption to Macau operations.

What Has to Go Right

- Wynn Al Marjan opens in 2027 as the only gaming facility of its scale in the region, with Billings noting on the Q1 call that the UAE’s tourism infrastructure and policy framework remain intact despite the conflict-related delay

- Macau mass momentum sustains: mass drop was up 19% in Q1 2026, and Wynn Palace running at 99% occupancy provides the demand foundation for the $900M to $950M Enclave tower to generate the $150M to $175M in incremental EBITDA management underwrote

- Las Vegas holds its premium positioning through the Encore Tower remodel, with Billings noting group room nights and rate pacing ahead of 2025 and ADR up year over year in April

- LTM adjusted EBITDAR of approximately $2.3B at 4.4x net leverage gives Wynn financial flexibility to fund both the UAE equity contributions ($350M to $450M remaining) and the Macau expansion without impairing the dividend or buyback program

What Could Still Go Wrong

- The UAE delay, described as “modest” but not yet quantified, carries tail risk: if regional instability persists into mid-2027, the ramp is pushed further out and the incremental EBITDA contribution that partially underpins the model is deferred

- Macau VIP hold was below normal in Q1 2026, reducing EBITDAR by $17M; a sustained hold compression or a slowdown in mass drop from the 19% pace would pressure the Macau EBITDAR that funds the Enclave build

- Las Vegas OpEx per day rose 6.8% year over year, with wage pressure and food cost inflation both cited by Fullalove; if those inputs remain elevated through the Encore Tower remodel period, EBITDAR margin at the 35% level may be harder to sustain

- Expansionary capex of $400M to $450M in Macau in 2026, combined with ongoing UAE equity contributions, concentrates capital outflow at a moment when Al Marjan’s revenue contribution remains uncertain

Should You Invest in Wynn Resorts, Limited?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Wynn Resorts, Limited stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Wynn Resorts, Limited alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze WYNN stock on TIKR for Free →