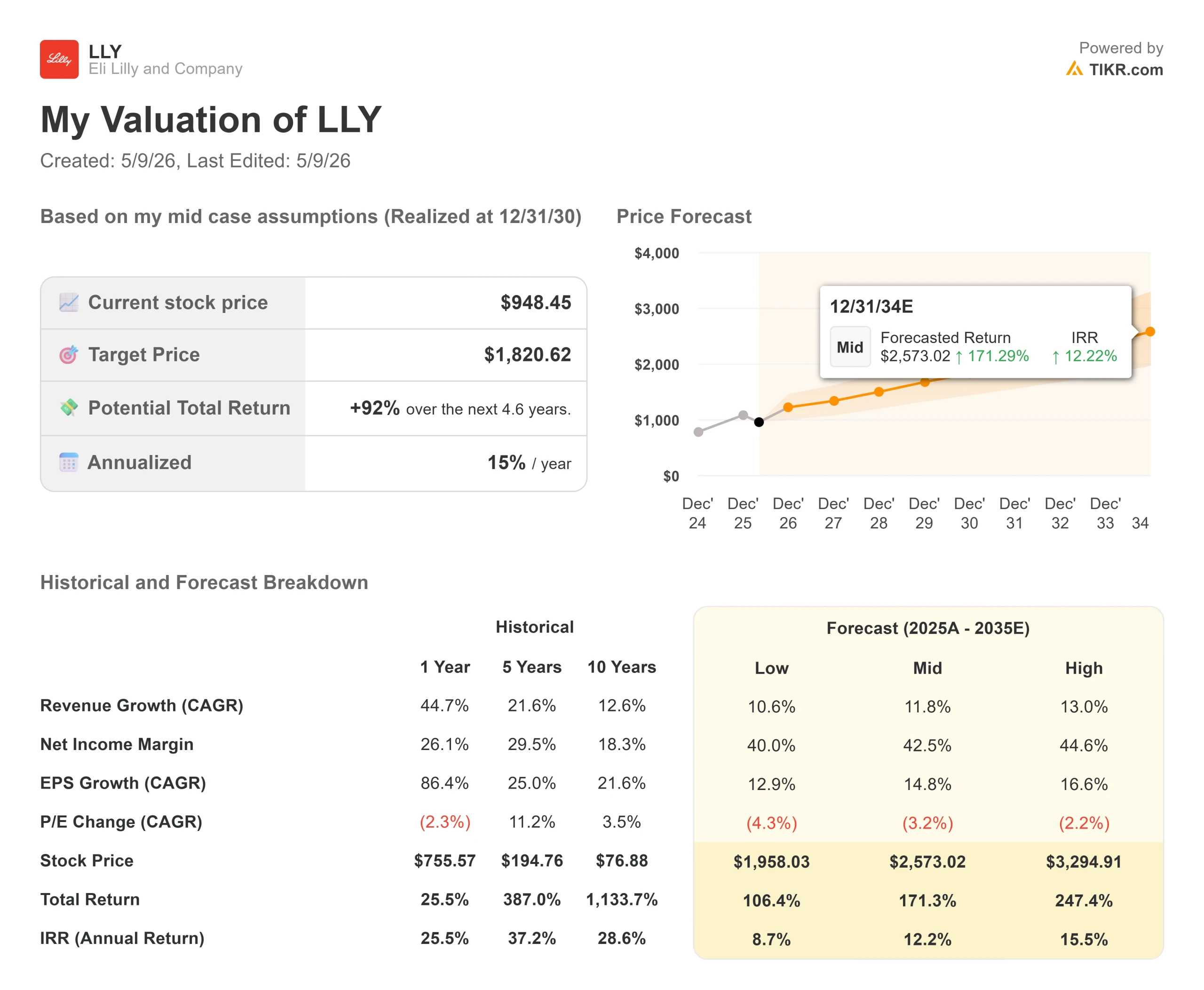

Key Stats for Eli Lilly Stock

- Current Price: $948.45

- Target Price (Mid-Case) ~$1,821

- Street Target: ~$1,209

- Potential Total Return: ~92%

- Annualized Return: ~15% / year

- Earnings Reaction: +3.07% (April 30, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Eli Lilly (LLY) is trading 16% below its 52-week high of $1,133.95, even after delivering one of the strongest quarterly beats in large-cap pharma history. The stock rose 3.07% on April 30 after Q1 2026 revenue came in at $19.8 billion, beating the average analyst estimate of $17.8 billion by nearly $2 billion, per TIKR data. Non-GAAP EPS of $8.55 topped the $6.79 consensus by nearly 26%.

Bulls point to accelerating free cash flow and a pipeline with no near-term generic threat. Bears point to pricing pressure from pharmacy benefit managers and Foundayo’s early prescription ramp running below Novo Nordisk’s oral Wegovy. The central question is whether Lilly’s volume engine can keep absorbing that pricing drag.

On May 6, the company gave a structural answer: an additional $4.5 billion investment in Indiana manufacturing, bringing its total U.S. capital commitments to more than $27 billion, per Lilly’s press release. CEO David Ricks framed it directly: “We are not just discovering the medicines of the future. We are building the world’s most advanced plants to make them.”

See historical and forward estimates for Eli Lilly stock (It’s free!) >>>

Why Volume Is Outrunning the Pricing Headwind

The most revealing moment of the Q1 2026 earnings call was not a revenue line. During Q&A, CEO Dave Ricks explained why the standard pharma pricing framework does not apply to the obesity category: “Pretty much every time we reduce pricing, we see a pretty large expansion.” Out-of-pocket sensitivity in this market drives volume responses that do not behave linearly, he argued, making it unlike almost any other drug category.

The numbers support him. Lilly’s non-GAAP performance margin reached 50% in Q1, up approximately 7 percentage points from a year earlier, per CFO Lucas Montarce on the earnings call, even as gross margins contracted about 1 point to 82.6% due to lower list prices. The company also raised its full-year 2026 revenue guidance to $82 billion to $85 billion, up $2 billion from its prior range, consistent with the TIKR consensus estimate of $85.1 billion for fiscal 2026.

That is the operating leverage story: volume scaling against largely fixed manufacturing infrastructure expands margins even as prices drift lower. The $27 billion domestic manufacturing buildout is the infrastructure designed to sustain that dynamic.

Three Platforms. One Thesis.

The injectable franchise, Mounjaro and Zepbound, generated $12.8 billion in combined global Q1 revenue, contributing $6.7 billion of growth versus Q1 2025, per the earnings transcript. That is the foundation. Internationally, Lilly holds an estimated market share above 53% across more than 55 launched countries, per Patrik Jonsson, President of Lilly International, on the earnings call. The growth lever now is patient activation, not market entry.

Foundayo (or forglipron), Lilly’s once-daily oral GLP-1 pill that requires no food or water restrictions, is the access layer. Ilya Yuffa, President of Lilly U.S.A., confirmed on the call that more than 20,000 patients had started Foundayo by late April, with 80% of those prescriptions coming from patients new to the GLP-1 class. Commercial access at two of the three largest U.S. pharmacy benefit managers goes live in mid-May. Medicare access through the CMS Bridge program starts no later than July 1, capping senior out-of-pocket costs at $50 per month, per the transcript. Full-scale direct-to-consumer TV advertising begins in Q3.

Retatrutide, a GIP, GLP-1, and glucagon triple agonist, is the pipeline’s most closely watched asset. The first Phase 3 trial, TRIUMPH-4, reported 28.7% mean body weight loss at 12mg over 68 weeks, per Lilly’s published trial data, the highest figure reported for any obesity drug in a Phase 3 setting. The pivotal TRIUMPH-1 general obesity readout is expected this quarter, per Dr. Dan Skovronsky on the earnings call. The new Indiana facility will also produce retatrutide commercially if development proceeds as planned, per Lilly’s May 6 press release. Detailed results from TRIUMPH-4 and the TRANSCEND-T2D-1 diabetes trial will be presented at the American Diabetes Association Scientific Sessions in June.

Ken Custer, President of Lilly Cardiometabolic Health, captured the portfolio logic clearly on the call: patients will want different medicines for different needs. Injectables for maximum efficacy, oral GLP-1s for those who prefer no needles, retatrutide for patients seeking the highest weight loss, and eloralintide, a selective amylin receptor agonist in Phase 3, for patients who need a non-GLP-1 option. That is a platform, not a single product.

On valuation multiples, Lilly trades at 20.20x NTM EV/EBITDA, a clear premium to Novo Nordisk at 9.95x, Merck at 14.55x, and Roche at 10.58x, per TIKR’s Competitors page. That premium reflects 42 active Phase 3 programs, per CFO Montarce on the call, an LTM ROIC of 45.8%, and a GLP-1 franchise with no credible near-term generic competition, per TIKR. Whether that premium holds depends on retatrutide’s TRIUMPH-1 readout and whether Foundayo’s prescription trajectory accelerates through Q3.

See how Eli Lilly performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $948.45

- Target Price (Mid-Case): ~$1,821

- Potential Total Return: ~92%

- Annualized Return: ~15% / year

See analysts’ growth forecasts and price targets for Eli Lilly stock (It’s free!) >>>

The TIKR mid-case model targets approximately $1,821 by 12/31/30, implying around 92% total return and approximately 15% annualized return from $948.45. The two primary revenue CAGR drivers are the continued global scaling of the incretin injectable franchise, and the multi-platform build through Foundayo and retatrutide. The model assumes around 12% revenue CAGR, conservative relative to the 44.7% one-year and 21.6% five-year historical rates per TIKR, reflecting market maturation and a growing mix of internationally negotiated prices. Profit margins are modeled to expand from 33.4% in 2025 to around 43% by 2030 per TIKR, driven by operating leverage from the manufacturing buildout.

The upside scenario requires retatrutide to reach commercial scale and Foundayo to capture meaningful Medicare volume after the July unlock. The downside scenario prices in slower international penetration and pricing pressure that limits margin expansion. At $948.45, the stock trades near the bottom of its recent range despite its strongest quarterly execution in years.

The Street mean target of $1,209.14 from 29 analysts (18 Buys, 6 Outperforms, 6 Holds, 2 No Opinions, 1 Sell per TIKR) implies around 27% upside on a 12-month basis. The TIKR mid-case at ~$1,821 reflects the longer horizon through 12/31/30 and pipeline contributions, particularly retatrutide, not yet in consensus models. The primary risk is further valuation multiple compression. LLY’s NTM P/E has already contracted from 35.55x in March 2025 to 25.57x today per TIKR, and a Foundayo ramp that disappoints in Q3 could compress it further.

Conclusion

Watch Foundayo’s weekly prescription run rate at the August 6, 2026, earnings call. If prescriptions are tracking above 20,000 per week, with the majority still coming from new-to-class patients, the access ramp is on track, and the multiple contraction story should ease. Lilly is executing as well as any company in the S&P 500. At $948.45, the stock is priced at less than the business appears to be delivering.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Eli Lilly?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Eli Lilly, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Eli Lilly alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Eli Lilly on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!