Key Stats

- Current Price: $7 (May 8, 2026)

- Q1 2026 Revenue: $541M, +3.3% YoY

- Q1 2026 Adjusted EPS: $0.12, down from $0.20 in Q1 2025

- Q1 2026 Adjusted EBITDA: $111M, down from $125M in Q1 2025

- Full-Year 2026 Adjusted EBITDA Guidance: $460M to $480M (reaffirmed)

- Full-Year 2026 Adjusted EPS Guidance: $0.56 to $0.60 (reaffirmed)

- TIKR Model Price Target: $11

- Implied Upside: ~55% over near 5-years (~10% annualized)

Wendy’s Stock Q1 2026 Earnings Breakdown

Wendy’s stock (WEN) posted Q1 2026 revenue of $541M, up 3.3% year over year from $523M, while adjusted EPS came in at $0.12, down from $0.20 in the same quarter last year.

Global system-wide sales declined 5.5% on a constant-currency basis, driven by a 7.8% drop in U.S. same-restaurant sales that reflected traffic declines, severe weather in January and February, and intentional hour reductions tied to the company’s Project Fresh footprint optimization.

International was the offsetting bright spot, delivering 6% system-wide sales growth on the back of new unit development in the Philippines and Mexico.

According to Ken Cook, Interim CEO and CFO, on the Q1 2026 earnings call, company-operated restaurants that have fully implemented Project Fresh operational initiatives outperformed the broader U.S. system by 310 basis points in same-restaurant sales, providing early proof that the turnaround playbook is working where adopted.

Adjusted EBITDA was $111M, down $13M versus the prior year, driven by lower U.S. company-operated restaurant margins, reduced franchise royalty revenue, and higher G&A spending on brand revitalization and international expansion resources.

Global company-operated restaurant margin came in at 10.8% for Q1, with U.S. company-operated restaurant margin at 11.4%, pressured by an ~8% commodity cost increase (led by beef inflation), ~4% labor rate inflation, and the short-term impact of footprint optimization.

Management reaffirmed the full-year 2026 outlook in its entirety, including adjusted EBITDA of $460M to $480M, adjusted EPS of $0.56 to $0.60, and full-year free cash flow of $190M to $205M.

The company also disclosed that system-wide sales are expected to decline by a mid-single-digit percentage in Q2 before returning to growth in the back half of the year, with the step-up driven by compounding Project Fresh initiatives and a significantly stronger year-over-year media spend comparison in H2.

The single largest strategic development this quarter was the signing of a franchise agreement to build up to 1,000 Wendy’s restaurants across China over the next 10 years, which Cook described on the call as the largest development agreement in company history.

U.S. digital sales grew 8.4% in Q1, with digital mix reaching 22.7% of U.S. sales, supported by the integration of an AI recommendation engine into the mobile app.

The company declared a regular quarterly dividend of $0.14 per share and confirmed it has approximately $35M remaining on its existing share repurchase authorization, though management stated no buybacks are planned for 2026.

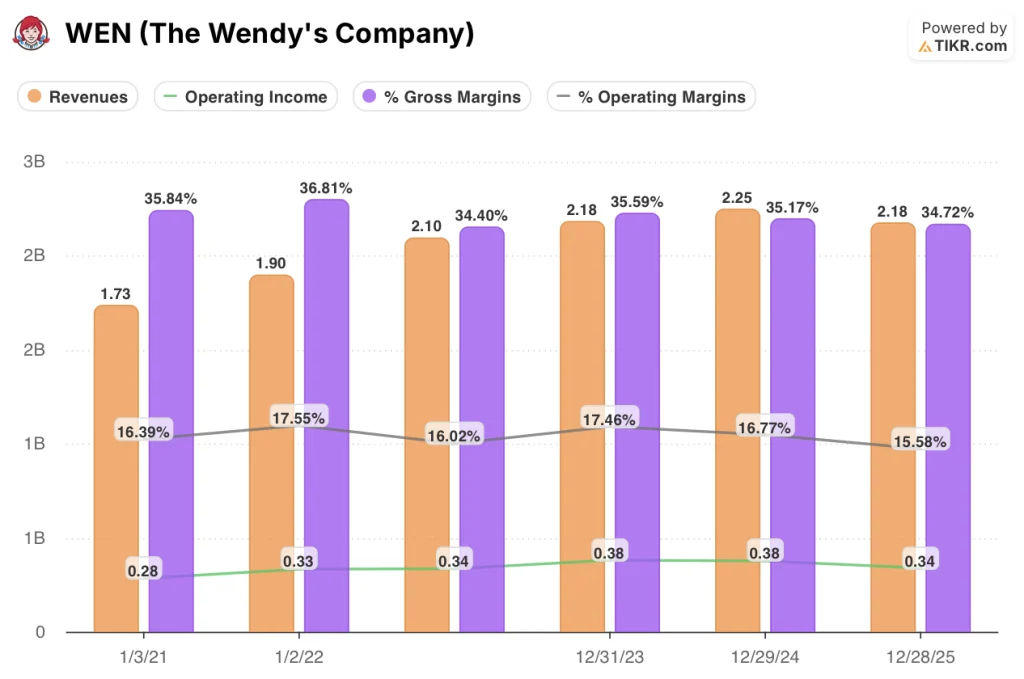

WEN Stock Financials

The Q1 2026 income statement reflects a business under deliberate margin pressure: gross margins have compressed materially since mid-2025, and operating income is running at its weakest levels in the eight-quarter window.

WEN stock’s revenue held at $540M in Q1 2026, roughly flat with Q4 2025 ($540M) but below the $560M peak reached in Q2 2025, and the YoY trend has been negative since Q2 2025 when the first decline of 1.7% appeared.

Gross margin came in at 33% in Q1 2026, a meaningful step down from the 36% peak reached in Q2 2025, and marks the third consecutive quarter of year-over-year gross profit contraction.

Operating income was $70M in Q1 2026, down from $110M in Q2 2025 and only modestly above the $70M trough posted in Q4 2025.

Operating margin was 12% in Q1 2026, compared to 19% in Q2 2025 at peak, reflecting commodity inflation, labor cost increases, and intentional G&A investment in brand revitalization and field resources.

Also, according to Suzanne Thuerk, Chief Accounting Officer and Global Head of FP&A, on the Q1 2026 earnings call, commodity inflation will be front-half heavy, with overall commodity costs running in the high single digits in H1 on the back of double-digit beef inflation, before easing to low single digits in H2 as the company begins to lap last year’s elevated beef costs.

What Does the Valuation Model Say?

TIKR’s model puts a price target of $11.34 on Wendy’s stock, implying ~55% total return from the current price of $7.30 over 4.6 years, or roughly 10% annualized.

The mid-case model assumes a revenue CAGR of 1.5% through 2035 and a net income margin of 5.6%, reflecting a modest recovery in profitability rather than a significant reacceleration.

Q1’s results are broadly consistent with those assumptions: the revenue beat was modest, the margin pressure is sequenced to ease as beef costs normalize in H2, and management’s decision to reaffirm full-year guidance keeps the base case intact.

The investment case for Wendy’s stock is neither stronger nor weaker after Q1; it is on track, with execution risk front and center as the key variable between here and the back-half inflection.

The debate for Wendy’s stock comes down to one question: whether the Project Fresh-driven H2 recovery is real enough and fast enough to justify buying at a 55% discount to model value.

What Has to Go Right

- U.S. same-restaurant sales must improve from negative 7.8% in Q1 toward the flat-to-positive range management is guiding for in H2, requiring the Minions collaboration, Pretzel Bacon Pub Cheeseburger relaunch, and new media agency to collectively close a gap that company-operated restaurants have only partially demonstrated is closeable

- Commodity inflation must ease on schedule, with beef costs expected to move from double-digit inflation in H1 to low-single-digit in H2, enabling U.S. company-operated restaurant margin to recover toward the guided 13% target

- The China development agreement for up to 1,000 restaurants over 10 years must begin to generate visible pipeline momentum, validating the international growth thesis at scale

- Digital sales, which grew 8.4% in Q1 with a 22.7% mix rate, must sustain their trajectory as the AI recommendation engine and expanded mobile checkout options mature

What Could Still Go Wrong

- Adjusted EBITDA was already down $13M year over year in Q1, with the full-year guided range of $460M to $480M implying substantial H2 recovery; any delay in foot traffic improvement extends the period of margin compression and strains the path to the midpoint

- U.S. franchisee average EBITDA margin fell to 9.3% in 2025, down 270 basis points, primarily on beef cost inflation; continued franchisee economic stress could slow operational initiative adoption beyond the 25% of the system that has fully implemented Project Fresh

- The system optimization program, which management expects to impact 5% to 6% of the system and is projected to create a $15M to $20M revenue headwind for 2026, remains on schedule but introduces ongoing revenue drag that offsets any early same-restaurant sales recovery

- Net leverage of 4.9x adjusted EBITDA at quarter-end is near the top of management’s 3.5x to 5x target range, and with no buybacks planned and dividend obligations continuing, the balance sheet provides limited flexibility if the turnaround takes longer than expected

Should You Invest in The Wendy’s Company?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up The Wendy’s Company stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track The Wendy’s Company alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze WEN stock on TIKR for Free →