Key Stats

- Current Price: ~$86 (May 8, 2026)

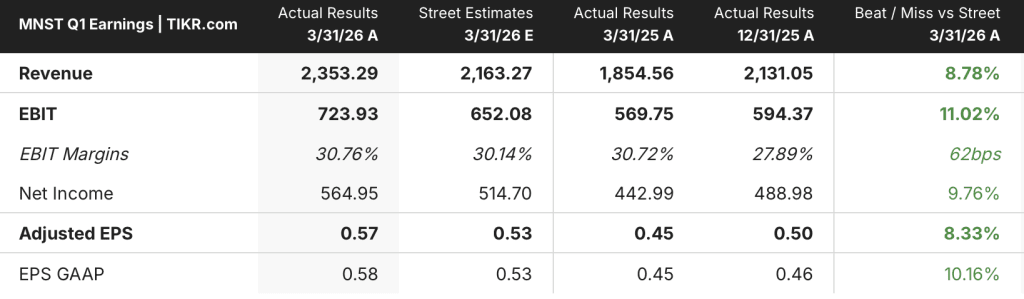

- Q1 2026 Revenue: $2.35B, +27% YoY

- Q1 2026 GAAP EPS: $0.58, +29% YoY

- Q1 2026 Adjusted EPS: $0.58, +24% YoY

- Monster Energy Drinks Segment Revenue: $2.19B, +28% YoY

- International Net Sales: $1.06B, +45% YoY; +33% FX-neutral

- April 2026 Sales Growth: ~24% YoY (non-FX adjusted); ~22% FX-neutral

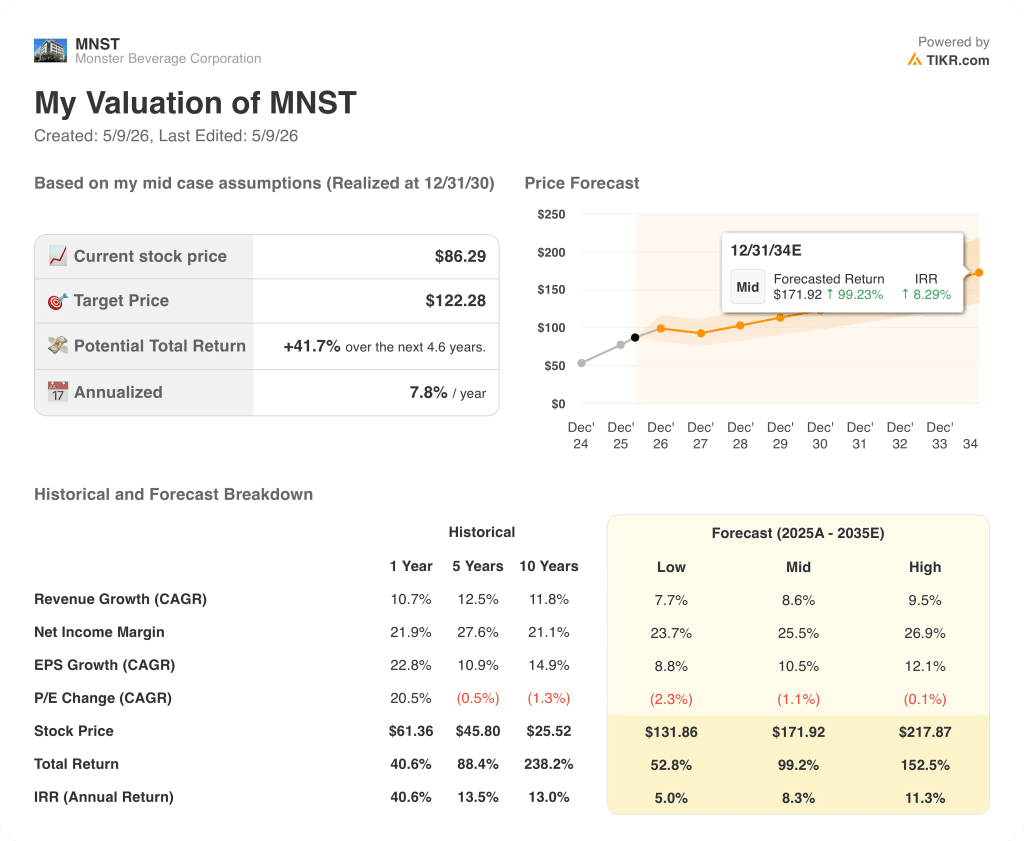

- TIKR Model Price Target: $122 (mid case, realized 12/31/30)

- Implied Upside: ~42% total; ~8% annualized

Monster Stock Q1 2026 Earnings Breakdown

Monster Beverage Corporation (MNST) crossed $2 billion in quarterly revenue for the first time in company history, posting Q1 2026 net sales of $2.35B, up 27% from $1.85B in Q1 2025.

GAAP EPS came in at $0.58 for the quarter, up 29% from $0.45 in Q1 2025.

International was the headline driver, with net sales outside the United States surging 45% to $1.06B, representing approximately 45% of total net sales versus roughly 40% a year ago.

EMEA led international growth, with net sales rising 53% in dollars and 37% on a currency-neutral basis, according to CEO Hilton Schlosberg on the Q1 2026 earnings call.

Asia Pacific net sales grew 40% in dollars and 37% currency-neutral, with standout performance in China (+95% in dollars) and India (+95% in dollars), according to Schlosberg on the Q1 call.

Latin America net sales increased 36% in dollars and 22% currency-neutral, with Brazil up 61% in dollars.

The Monster Energy Drinks segment, the company’s core business, grew net sales 28% to $2.19B.

The Strategic Brands segment increased net sales 29% to $127M.

The Alcohol Brands segment declined 6% to $33M.

In the United States, net sales grew 16% in Q1 2026, supported by pricing actions taken in late 2025 and strong performance across the Ultra and Juice Monster brand families.

Ultra White grew 34% in the U.S. quarter-over-year, and the Juice Monster family grew 26%, according to Schlosberg on the Q1 call.

Gross margin contracted to 55% in Q1 2026 from 57% in Q1 2025, driven by geographic sales mix (120 basis points of adverse impact from heavier international weighting), higher aluminum can costs, and increased freight-in costs from out-of-orbit production.

Operating income grew 28% to $730M from $570M in Q1 2025, and the company confirmed it has returned to in-orbit production as of the current period.

Monster repurchased 1.4 million shares at an average price of ~$74 during Q1 2026 for approximately $100M, with ~$400M remaining under the existing authorization as of May 6, 2026.

April 2026 net sales were approximately 24% higher than April 2025 on a non-FX adjusted basis and approximately 22% higher on a currency-neutral basis, according to Schlosberg on the Q1 call.

Financials

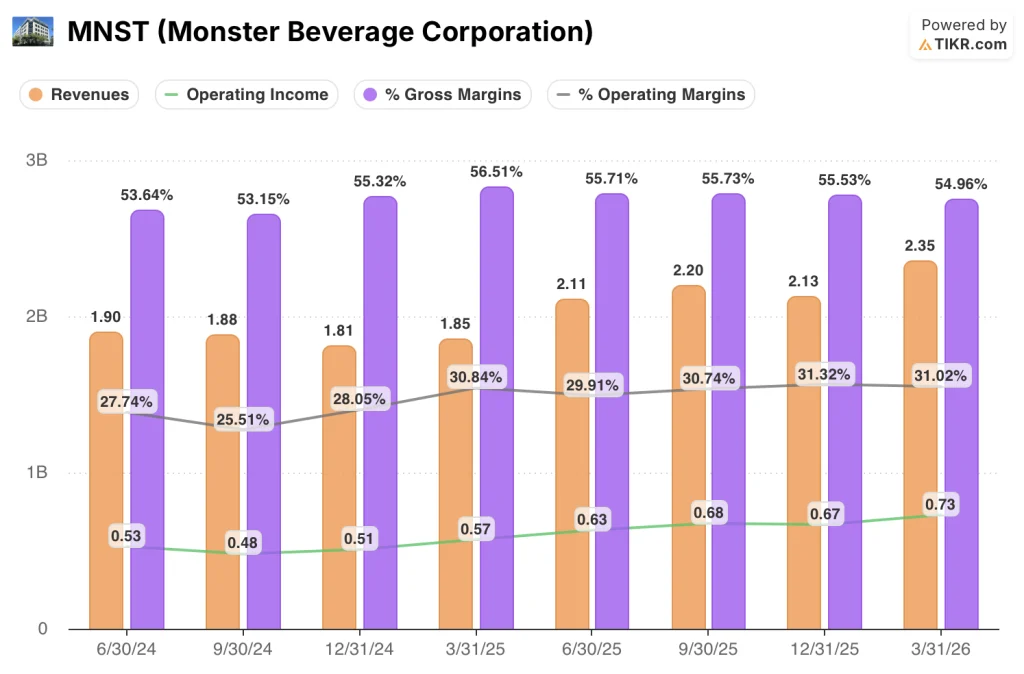

Revenue growth has re-accelerated sharply over the past four quarters, with margin pressure emerging as the cost of that expansion.

Revenue troughed at $1.81B in Q4 2024, then climbed steadily: $1.85B in Q1 2025, $2.11B in Q2 2025, $2.20B in Q3 2025, $2.13B in Q4 2025, and $2.35B in Q1 2026.

Gross margin peaked at 56.5% in Q1 2025, then compressed progressively: 55.7% in Q2 2025, 55.7% in Q3 2025, 55.5% in Q4 2025, and 55% in Q1 2026.

Operating income expanded from $570M in Q1 2025 to $630M in Q2 2025, $680M in Q3 2025, $670M in Q4 2025, and $730M in Q1 2026.

Operating margin held in a tight range across the past four quarters — 30.8% in Q1 2025, 29.9% in Q2, 30.7% in Q3, 31.3% in Q4 — before settling at 31.0% in Q1 2026.

The gross margin compression in Q1 2026 was attributable to three factors identified by Schlosberg on the Q1 call: geographic mix (international growth carries structurally lower margins), higher aluminum can costs from tariff-driven Midwest premium increases, and out-of-orbit freight costs from demand exceeding forecast.

Management stated on the Q1 call that the company expects a modest sequential increase in aluminum-related costs through at least the end of 2026 relative to Q1 2026 levels.

Selling expenses improved as a percentage of net sales to 8.3% in Q1 2026 from 9.3% in Q1 2025, and G&A improved from 12.3% to 11.3% over the same period, reflecting operating leverage on the higher revenue base.

What Does the Valuation Model Say?

The TIKR model prices Monster Beverage Corporation stock at $122 in the mid case, implying roughly 42% total upside from ~$86 over the next 4.6 years, or approximately 8% annualized.

The mid case assumes a revenue CAGR of 8.6% and a net income margin of 25.5% — both look achievable given Q1’s 27% revenue growth and pricing actions already in place.

The gross margin trajectory is the one variable that could undermine the model — if international mix continues to expand while EMEA and APAC unit economics remain structurally below consolidated averages, 25.5% net income margin may prove optimistic.

At roughly 8% annualized in the mid case, Monster Beverage Corporation stock offers a reasonable return — but the stock’s 14% move on earnings day has already closed a portion of that gap.

Monster Beverage just proved it can grow revenue at 27% — the open question is whether the international markets driving that growth will ever carry margins that justify the valuation.

Growth Case: International Becomes a Margin Tailwind

EMEA gross margin improved to 35.9% in Q1 2026 from 35.1% a year ago — a small move, but in the right direction. If EMEA and APAC margins continue to inch upward as those markets scale, the 120 basis point geographic mix headwind that pressured consolidated gross margin in Q1 begins to reverse.

The 8.6% revenue CAGR assumption in the TIKR mid case already looks conservative against a quarter where the U.S. grew 16% and international grew 45%, and pricing actions implemented in late 2025 are performing as expected according to management on the Q1 call.

Margin Case: The Mix Problem Compounds

International is now ~45% of revenue, up from ~40% a year ago, and EMEA gross margins of 35.9% sit well below the consolidated 55.0%. Every point of share that shifts from domestic to international pressures the blended margin.

Aluminum costs added just under 1% of margin headwind in Q1 2026, according to Schlosberg on the Q1 call, with management guiding for a continued modest sequential increase through at least the end of 2026.

Should You Invest in Monster Beverage Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up MNST stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Monster Beverage Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze MNST stock on TIKR for Free →