Key Stats for Spotify Stock

- 52-Week Range: $340.11 to $648.25

- Current Price: $427.43

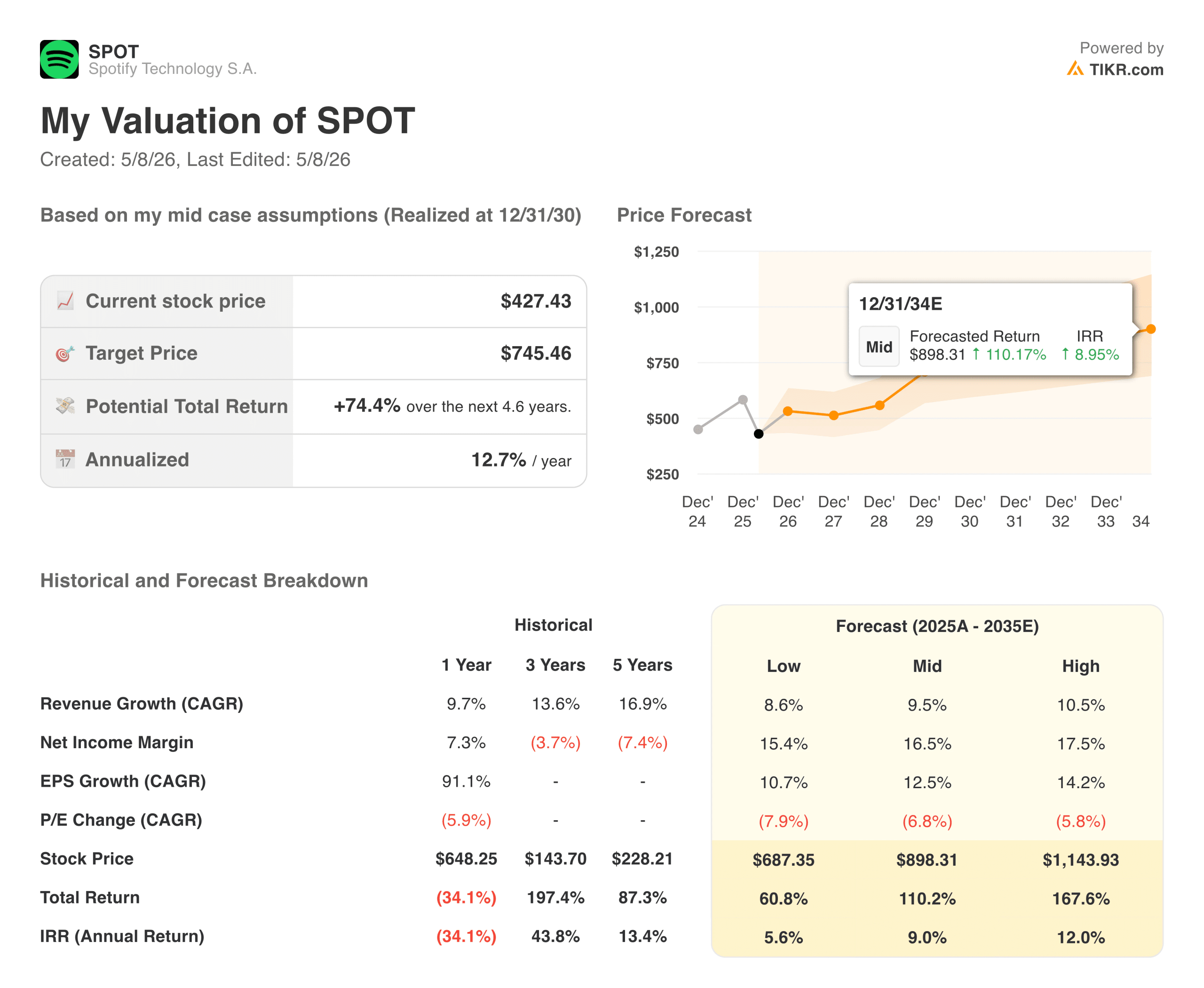

- TIKR Target Price (Mid): ~$745

- TIKR Annualized IRR (Mid): ~13% per year

- Q1 2026 MAUs: 761 million

- Q1 2026 Premium Subscribers: 293 million

Value your favorite stocks like SPOT with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

The Business Nobody Expected Spotify to Build

For most of its existence as a public company, Spotify (SPOT) was a growth story with a profitability problem. Revenue was compounding reliably, but the cost structure kept absorbing it before it could turn into earnings. Operating margins bounced between deeply negative and barely positive for years, and the bears made a straightforward argument: this is a business structurally incapable of generating real returns because the labels will always take too much.

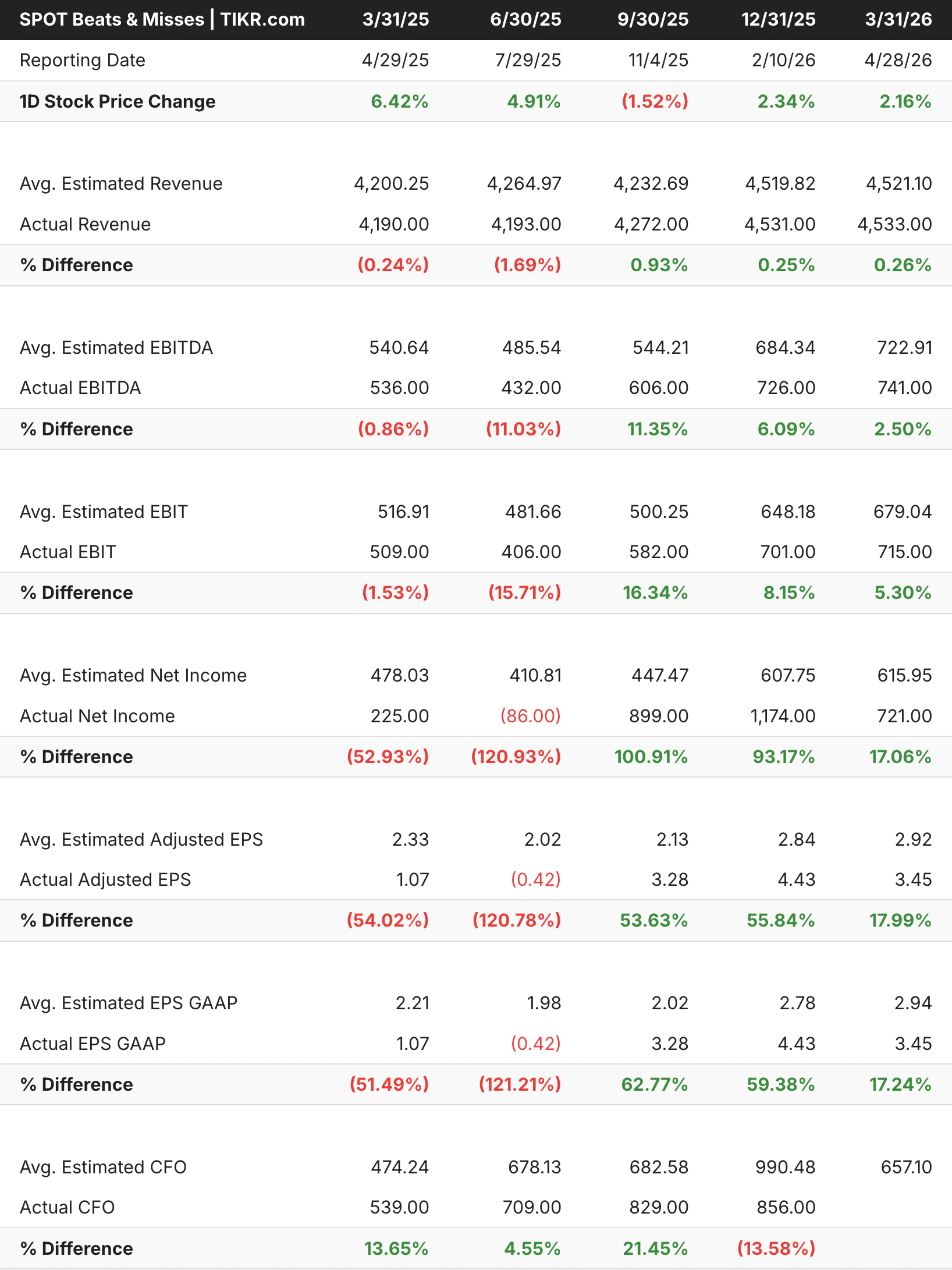

That argument is looking worse by the quarter. Spotify has now delivered meaningful operating income for six consecutive quarters, and the trajectory is not flattening out. Q1 2026 operating income came in at €715 million against guidance of €660 million, representing a 15.8% operating margin and growth of 40% year over year. Free cash flow for the trailing twelve months reached €3.2 billion.

The beats-and-misses table tells a useful story about the volatility in this business, but the direction is what matters. The last three quarters have seen consistent beats on EBIT and EBITDA, with operating income coming in above expectations by meaningful amounts as cost discipline has begun to compound on top of gross margin expansion.

See analysts’ growth forecasts and price targets for SPOT stock (It’s free!) >>>

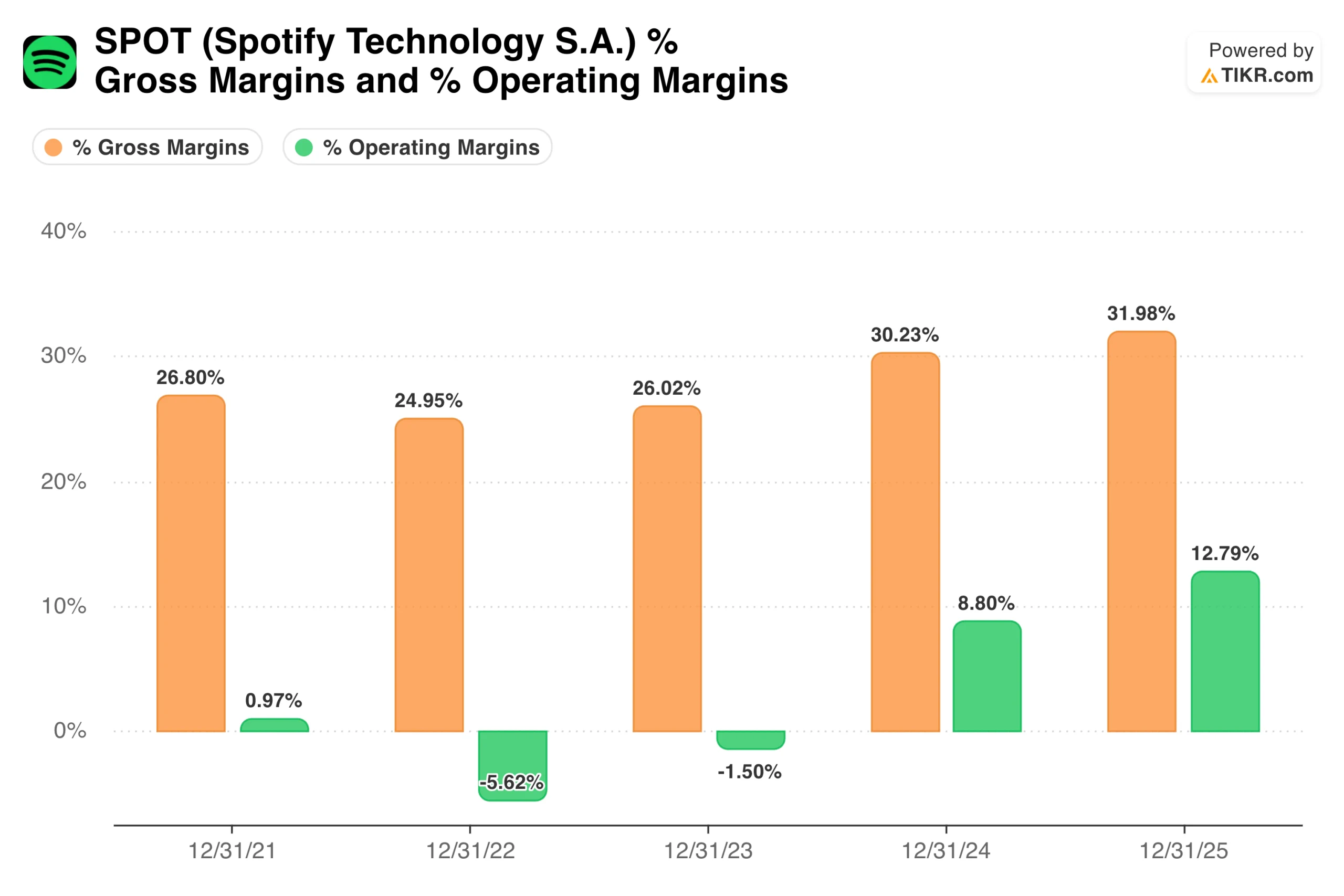

From Negative Margins to Best-in-Class in Three Years

The margin chart is worth sitting with for a moment. Operating margins went from -5.6% in 2022 to essentially breakeven in 2023, then jumped to 8.8% in 2024, and reached nearly 13% for the full year 2025. Gross margins have followed a similar path, climbing from around 25% in 2022 to nearly 32% in 2025, with Q1 2026 hitting a record 33%.

What drove this is not a single factor but a combination of pricing power, podcast profitability, and operating leverage on a largely fixed-cost base.

Spotify raised Premium prices in the US for the third time in four years in January 2026, yet subscribers kept growing, reaching 293 million at the end of Q1. That is the clearest possible signal that the product has real pricing power, which is the foundation of any durable margin story.

The ad-supported segment is the one genuine soft spot. Ad revenue declined 5% year over year in Q1, with music advertising facing pricing softness even as impressions grew. Podcast advertising held up better, but the overall ad business is not yet firing on all cylinders.

That matters because advertising carries higher margins than premium subscriptions at scale, and it represents the biggest source of upside surprise if it inflects.

With 35 analysts covering Spotify stock and the ad recovery call split wide open, the data window matters. Catch analyst upgrades, earnings beats, and estimate revisions on SPOT the moment they drop with TIKR for free →

74% Upside in the Mid Case, and the Inputs Are Not Aggressive

TIKR’s model targets around $745 in the mid-case, implying a total return of around 74% over roughly 4.6 years, or about 13% annualized. The model assumes revenue growth of around 9% to 10% annually and net income margins expanding toward the mid-to-high teens. Given that Q1 2026 operating margins are already sitting at 15.8%, the model is not asking for a heroic leap from where the business is today.

What the Bulls Are Counting On

- The margin path is already in motion. Operating margins of nearly 16% in Q1 2026 are already within the model’s mid-case target range, and management has guided to continued improvement in both gross and operating margins for the full year. The model does not require multiple expansions or accelerating revenue growth to generate a strong return from current levels.

- 761 million MAUs is a genuine moat. Spotify has more monthly active users than any other audio platform on earth, and the churn data suggests those users are not leaving. That installed base creates a compounding flywheel as the company monetizes it more deeply over time through higher ARPU, advertising, and ancillary products like audiobooks.

- Pricing power has been demonstrated, not assumed. Three price increases in four years in the US market, and subscribers kept growing. That is the kind of evidence that changes how you should think about the long-term earnings trajectory.

- Free cash flow is already substantial. With €3.2 billion in trailing twelve-month free cash flow and a cash position of €9.5 billion, Spotify has the balance sheet to invest aggressively, buy back stock, or weather a prolonged downturn in advertising without altering its core strategy.

What the Bears Are Watching

- The ad business is a real problem for now. Ad revenue declining 5% year over year, even as overall digital advertising has been recovering, is not a good look. If the ad segment does not recover, it caps the model’s upside and raises questions about whether podcast monetization will ever reach its potential.

- The multiple still requires belief in the margin story continuing. At around $427, Spotify is not cheap in absolute terms. The stock is pricing in sustained margin expansion, and any quarter that shows gross margin slipping back toward the low 30s will create meaningful downside. The 2022 data point in the margin chart is a reminder of how quickly the story can reverse if cost discipline slips.

- North American subscriber growth is slowing. Premium growth in the US was notably softer in Q1, with management attributing it partly to the January price increase. Three price hikes in four years has likely pulled forward some of the addressable base, and the next leg of subscriber growth will have to come increasingly from international markets where ARPU is structurally lower.

Should You Invest in Spotify

The core debate around Spotify has shifted from whether the business can be profitable to how profitable it can ultimately become. That is a much better position to evaluate a stock from than the one where things stood two years ago.

The margin chart tells the most important part of the story. A business that was operationally unprofitable in 2022 is now generating nearly 16% operating margins and over $3 billion in annual free cash flow, with management guiding for further improvement.

The TIKR model’s mid-case target of around $745 does not require anything dramatic from here, just continued execution on a path the business is already on. The ad weakness and North American subscriber deceleration are real things to monitor, but neither changes the fundamental direction of the story.

See analysts’ growth forecasts and price targets for SPOT stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!